January was a volatile month for the markets in general, and municipal bonds were not immune. But volatility can lead to opportunity.

In December 2021, as the market began to price in anticipated interest-rate hikes from the Federal Reserve in 2022, we saw an increase in Treasury yields—and an increase in volatility. In January 2022, volatility in the muni bond market picked up as yields saw their largest increase since the first quarter of 2021. Price discovery continues to plague the market, as it has over the past month, with bid-ask spreads ranging between 15 and 25 basis points (bps)1 across maturities on the first day of trading in February.

Much of the larger movement seen in munis this year has been essentially a catchup to what happened in the Treasury market at the end of last year, which munis did not participate in. Munis could continue to experience brief spurts of volatility as price discovery continues in the short term, but longer term, we expect volatility to quiet as valuations are becoming more in line with historic norms. As we look at overall market performance, it is worse farther out on the yield curve, but on the quality front, the returns are fairly in line across the credit spectrum, confirming that the recent drawdown in the market was almost entirely interest-rate driven.

Despite current uncertainty, we maintain an optimistic outlook for the rest of 2022, and remain rooted in our belief that periods of heightened price dislocation create more opportunities to capture relative value. Risk management is at the core of our portfolio construction process, allowing us to understand exactly how a trade can impact our funds from a duration and risk perspective. Over the past two months, our approach to risk management helped the team maintain a neutral duration profile within our portfolios.

We are able to tap into our deep and experienced research bench and leverage our extensive modeling capabilities to find those bonds that offer the best relative value. While this is true in all markets, we can often find the great opportunities when the markets are messy like we saw in January 2022.

The Value of Munis

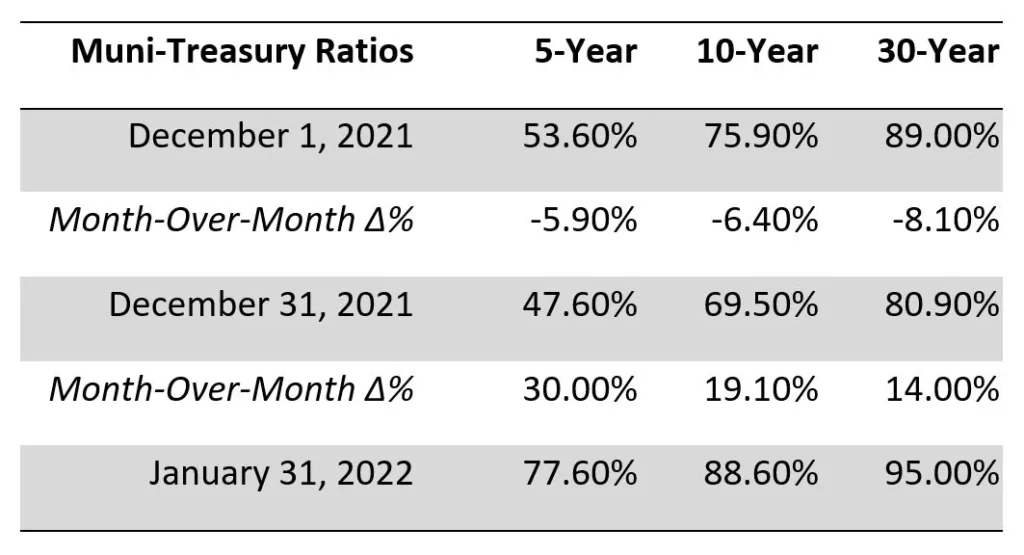

Municipal bonds traditionally serve to reduce volatility of an investor’s overall portfolio while providing tax-free income. Interest payments on Treasury bonds are subject to an investor’s regular income tax rate. If one wants to get a sense of which asset class is right for them at a particular point in time, they can compare the after-tax yields on bonds of equivalent credit quality and maturities from each asset class. The muni-to-Treasury ratio is a commonly used metric to perform this exercise; however, it should be noted that Treasury yields are often quoted before taxes. It is standard practice in munis to assume an income tax rate of 30% to estimate the after-tax Treasury yields so that an apples-to-apples comparison may be made. From this, one can deduce that munis are relatively cheap to Treasuries when the muni-to-Treasury ratio rises above 70%, or relatively expensive when they dip below that threshold—generally speaking.

Over the trailing 12 months ending January 31, 2022, the average yield on a AAA muni bond with a five, 10 and 30-year maturity averaged 54.1%, 68.1% and 78.5%, respectively, to the yields of Treasury bonds at corresponding maturities.2 As highlighted in the table below, AAA muni valuations were generally in line with those levels at the end of last month.

Navigating Market Conditions: The Importance of Risk Management

Fundamentals in the municipal bond market today remain sound, while technicals—although slightly weaker as of late—look healthy to us. We believe current valuations offer an attractive entry point for investors that have been sidelined by perceived low nominal yields. The same value exists for investors looking to add to their existing exposure now that munis have cheapened relative to Treasuries. As a result, we believe that active managers’ best chance to outperform will depend on credit selection for the remainder of 2022.

We think risk management practices will be especially critical going forward as we navigate impending short-term volatility, whether it stems from policy adjustments, pandemic developments or other economic uncertainties. The term “risk management” is commonly misinterpreted to mean risk-avoidance, or mitigation. Among Franklin Templeton’s Municipal Bond team, we hold a more positive belief that periods of heightened price dislocation create more opportunities to capture relative value. Or in other words, we believe risk should be optimized, rather than minimized. No single measure or methodology can reveal the “truth” about risk.

In our view, a mosaic of analytics, oversight protocols and consultation are required to obtain a holistic understanding of risk in today’s municipal bond market. We leverage proprietary credit models, and both macro and sector-specific models enable our entire team to assess the relative value of bonds offered in the secondary market, which frees up our research analysts to focus on assessing relative value opportunities that are available in the primary market. Ultimately, the team understands the subtle nuances of credit that are unique to each sector, which in turn enables us to gauge the impact of macro and sector-specific risks on our holdings down to the obligor-level.

Looking ahead, we are confident in our ability to navigate volatile market conditions and find the good credit stories at attractive valuations for our portfolios.

ENDNOTES

One basis point is equal to 0.01%.

Bloomberg, as of January 31, 2022

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Because municipal bonds are sensitive to interest rate movements, a municipal bond portfolio’s yield and value will fluctuate with market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the portfolio’s value may decline. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value.