Executive summary

We remain optimistic that 2022 will see a continuation of the overall positive economic momentum seen in 2021. Omicron represents a key risk, though the signs so far point to reduced severity, even if it’s much more transmissible. This may even be good news for the world. However, it remains too early for any major conclusions.

This important risk aside, consumption and employment are, in our view, in generally good shape and supply bottlenecks are improving. Indeed, the US is finding it hard to fill jobs, which is a tail wind for inflation. Inflation is broad and we support Jay Powell’s decision to remove reference to ‘transitory’, even if he was late to do so.

We view inflation as sticky, rather than us being outright inflation bulls. We believe more could and should be done, from a monetary perspective, to reflect the general good health of the world’s largest economy and normalise monetary policy so that there is something to cut in a downturn. We believe, when the market comes round to this, curves will steepen.

There is a good chance risk assets will not appreciate higher yields. However, given the generally positive economic backdrop, we believe this will be an opportunity to add to our already favourable exposure to high yield debt. It will perhaps also give us an opportunity to close our underweight to investment grade bonds.

Macroeconomics

Economic expectations have been somewhat seasonal in 2021. In Q1, growth expectations were boosted by the late 2020 vaccine efficacy results, but they were dampened in Q2 by the spread of the delta variant and the spectre of supply-side bottlenecks. As Q3 progressed, optimism returned, but was dealt a blow by the news of the Omicron variant in Q4. Despite the volatility in expectations, we have good visibility on global nominal growth being ~10.2% in 2021.

At the time of writing, Omicron has thus far brought with it some restrictions on mobility. We await more data on the rate of transmission, its severity and the extent to which it evades vaccines. Early indications are that it is much more transmissible (e.g. data from Japan suggesting >4x), whilst potentially less severe than previous strains. The nascent data also suggests reduced but still substantial vaccine efficacy, and Pfizer has promoted the effectiveness of its booster jab against this new strain. We are optimistic, but it is early days.

After an early Omicron shock, though nothing to the extent of March 2020, financial markets rebounded and look set to continue on the ever-resilient ‘lower for longer’ path.

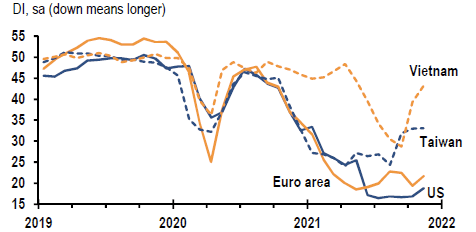

Supply-chain bottlenecks have been one of the main features of 2021, adding a headwind to what was a strong year for global GDP growth. Omicron aside, tentative signs of improvement have been evident, particularly in Asian manufacturing hubs, but also in the US and Europe.

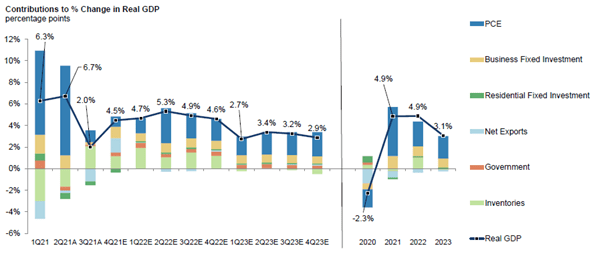

Meanwhile, inventories have been stretched to cope with issues in supply chains. We expect the rebuilding of inventories, at higher costs (e.g., labour), to be part of the growth (and inflation) dynamic in the coming months. For example, the cumulative inventory shortfall in the US grew to over one trillion dollars in Q321 relative to Q419. Expectations are for inventory re-build to have a meaningful contribution to growth in 2022.

China is certainly of interest as we move into 2022. It seems to be doing a good job in managing the default of Evergrande without too much of an over-spill into the general Chinese property and banking sector. Whilst consensus is growing that issues in the Chinese real estate sector will be a headwind, the People’s Bank of China has tilted policy towards dealing with the aftermath of the default, including a cut in the reserve requirement ratio. More generally, there is scope for catch-up in emerging markets, which have lagged in terms of bounce-back from Covid, to be a tailwind for global growth in 2022.

Consumption

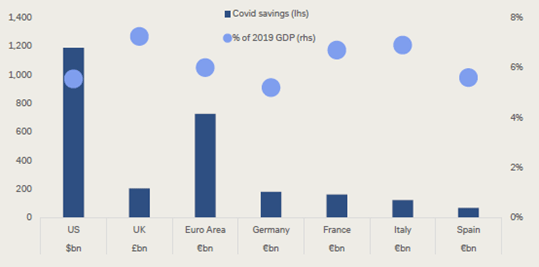

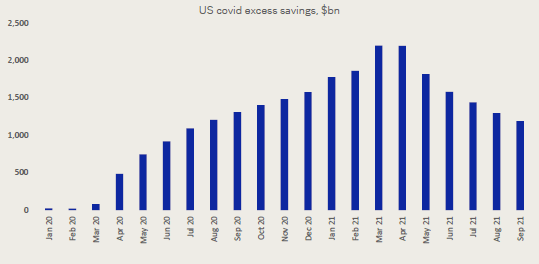

One of our favourite topics in 2021 has been the excess savings rate, particularly in the US, and the support to consumption that may come from this. Given the crucial role US consumption plays in not just domestic but global growth too, this is important. The evidence suggests a slow release of pent-up demand is ongoing.

Employment

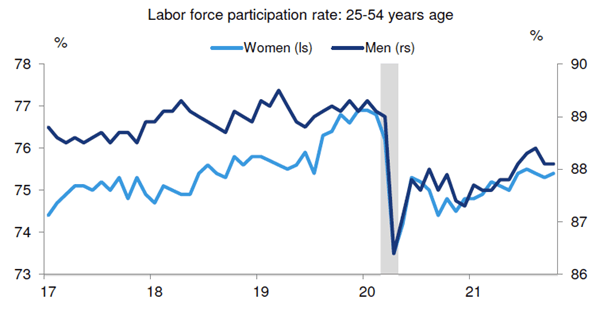

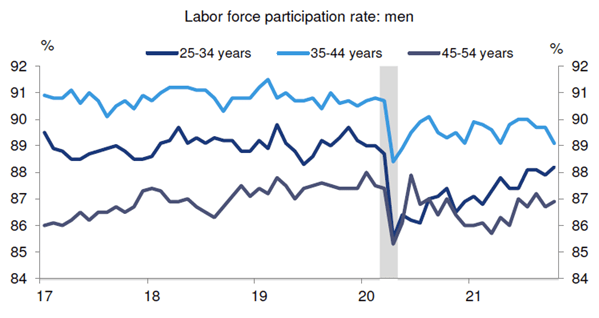

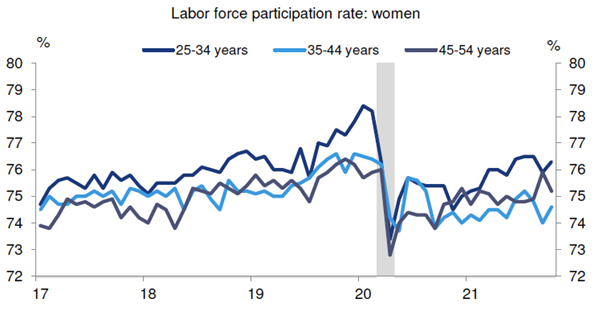

Savings are of course finite. With job openings in the US at 11m and labour participation rates below pre-pandemic levels, the US is not yet fully back to work; although the gap is closing, there remains a ~1.7% shortfall in labour participation. Digging into the data, it is notable that 55+ age workers make up roughly 60% of that participation shortfall. The other 40% appears to be dominated by ‘prime-age’ women, with, although feeling like a twentieth century explanation, childcare issues being at least partly attributed.

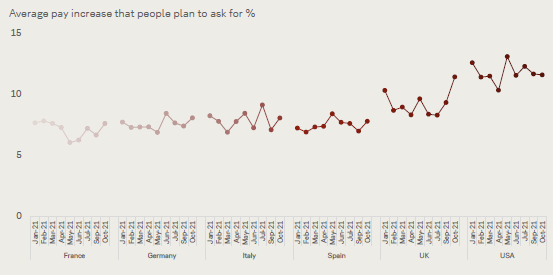

Whilst openings remain high alongside obstacles to getting back to work, hours worked are increasing. We also note the apparent confidence US workers have in asking for a pay rise. Of course, what people want and what people get can be two different things, but the dynamics in the labour force would suggest a reasonable amount of power in the hands of labour. This has implications for both consumption and inflation.

Inflation

US CPI for the month of November was 6.8%, a rate not seen since 1982. The debate all year has been whether inflation is transitory or something stickier, although in recent weeks Jay Powell has decided to remove the ‘t’ word from Fed communications.

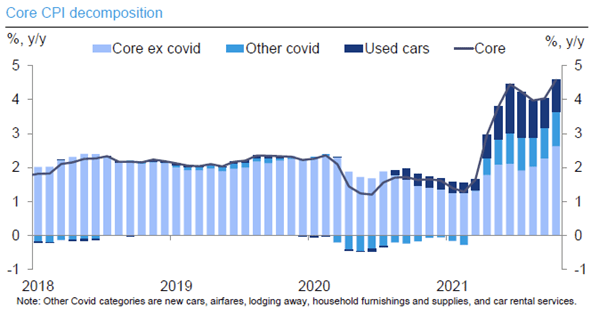

Above-trend goods inflation in the US remains broad-based across core goods, appliances and home furnishings. Given used cars and trucks alone have contributed ~1ppt to core consumer price inflation (CPI), it is understandable why such factors have been used in the transitory argument. However, if we look at core CPI excluding covid sensitive prices altogether, as per the chart below, inflation is still running above the 2% target.

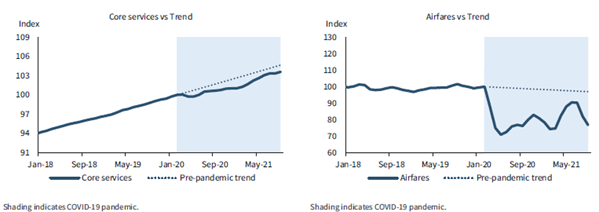

Meanwhile, owner-equivalent rents, or housing costs, are running above 3% and look sticky heading into 2022. Indeed, housing is not stuck in a shipping container or waiting for semi-conductor factories to adjust to higher levels of demand. In terms of granular services inflation data, it is only really airline tickets running at meaningfully below pre-pandemic levels.

Rates Positioning

It may seem a semantic point, but we would describe the tapering of QE and around 2 hikes expected in the U.S in 2022 as a reduction in phenomenal levels of monetary support, rather than a move to tight monetary policy. Even with these expectations baked into the market, there remains a huge support base for economic growth and risk assets.

We believe, going into 2022, data will support our optimistic view of the world and bond yields will be tested as a result. More specifically, the major curve flattening that we’ve seen in the second half of the year will likely reverse as the market accuses the Fed of being behind the curve. This may not necessarily be a January phenomenon, particularly with the arrival of Omicron, but we do expect this to be in the first half.

If we’re correct about perceptions of the Fed being behind the curve and the steepening of bond curves, will risk assets have a wobble? Will the periods of positive correlation between bonds and equities seen when the market thinks the Fed has its back, see the corollary of both equities and bonds selling off in tandem?

Time will tell, but we think the odds of this happening are reasonably short. That being said, such is the unpredictability that comes from extreme market manipulation, positioning fully for such events could be dangerous. We view some duration (2.75 years at end November) as justified even if we do think rates are very expensive and we also like high yield (more later), albeit the higher-quality end. The trick for our valuation-based process is to have plenty of dry-powder for when the market becomes cheaper.

We have positioned the Fund’s 2.75-3 years duration mainly in the US (~60%). We do believe US yields are going higher, but it is closer to peak, in our view, than other major, liquid markets. Within the US, we favour the middle-part of the curve. We have some long-end exposure, but much less than our index. We will begin to increase our bet on steepening curves if we see the US 5s30s flatten below 50bps spread (currently ~60).

The balance of the Fund’s duration (~30%) is in Europe. However, close to half of this has been switched into Swiss five-year bonds in a pair trade versus German five-year bonds, where we see an attractive pricing differential between the two markets. Within the European exposure, a long-held and profitable trade has been a German 5s10s flattener (long 10, short 5), which has been a useful counter to the general rising rates bias that exists within the portfolio. We have trimmed as the spread has moved in our favour, but this remains an important core position.

An important discussion we’ve had is at what level of yields would we be neutral duration per our process (4.5 in a range of 0-9). Previously, we’ve been guided by long-term asset returns and viewed a ten-year yield of ~3.5% as long-term fair value versus trend nominal growth. However, in this cycle, with a huge Fed balance sheet and mountain of government debt, it seems highly likely to us that ten-year yields will not (be allowed to) break out to that extent. We are thinking a level of rates for us to be neutral in this cycle is lower than 3.5%, possibly in the 2.5% – 3.0% range. Should rates break through 2% next year, this may help guide expectations as to how we increase duration in the portfolio in the months and quarters ahead.

Spread product

Corporate fundamentals continue to head in the right direction. Not forgetting the inventory chart from earlier in this note, cash may be currently flattered for many companies and will likely drop as inventories build. However, we would view this in the ‘good problem’ camp, rather than a credit deterioration story. In all likelihood, while debt is so affordable and refinancing cliffs pushed out, super-low default rates will continue in 2022.

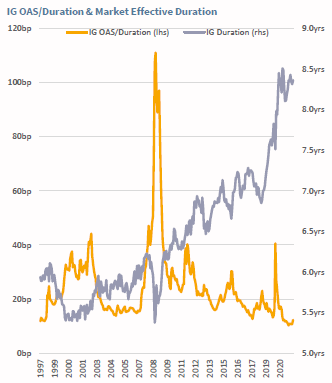

Reflecting the outlook for credit, investment grade spreads remain very low and only had a mild wobble in the short-lived Omicron sell-off. European investment grade spreads have been widening, largely due to technical factors, but the amount of widening would not be spotted on a long-term chart. Meanwhile, the interest rate risk, or duration, has never been higher. Given 2021 was a record year for low corporate spread volatility, we perhaps should have owned more, but, equally, the opportunity cost has been modest. In a similar vein to our thoughts on fair value of ten-year treasury yields in this cycle, our milestone for fair value of investment grade credit (150bps spread) could also be lower in this cycle. If we see volatility into new year, we will be more aggressive in our allocation to investment grade (currently 40% in a range of 0-100%), without being more aggressive on the types of instrument we buy (i.e. we will remain relatively discerning when it comes to bank capital securities until they offer genuinely compelling terms).

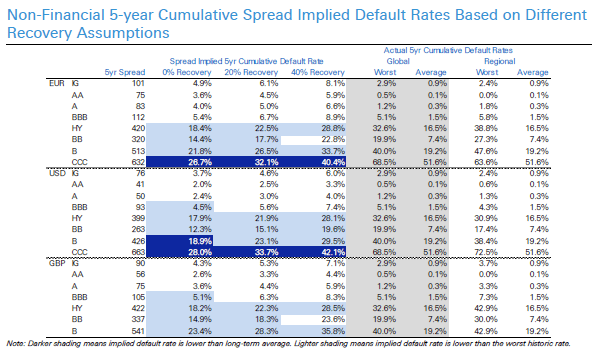

As previously mentioned, we like high yield debt on a relative basis and, as yields have risen (the yield on our high yield bond fund is now ~5%), increasingly on an absolute basis too. During the Omicron sell-off, we increased high yield exposure to 27.5% (range 0-40%). The data in the following chart, showing that default spread compensation is much better in high-quality high yield than lower quality (light blue versus dark blue), is a crucial point for all of our strategies. We may have a sanguine view on defaults. Indeed, lower quality bonds can be a good home in a rising rate environment (higher spread cushions the impact of rising interest rates). However, we must also guard portfolios against the unexpected, and you do not want to be the one holding CCCs when the party stops.

Key Risks

Past performance is not a guide to future performance. The value of an investment and the income generated from it can fall as well as rise and is not guaranteed. You may get back less than you originally invested. The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

Investment in Funds managed by the Global Fixed Income team involves foreign currencies and may be subject to fluctuations in value due to movements in exchange rates. The value of fixed income securities will fall if the issuer is unable to repay its debt or has its credit rating reduced. Generally, the higher the perceived credit risk of the issuer, the higher the rate of interest. Bond markets may be subject to reduced liquidity. The Funds may invest in emerging markets/soft currencies and in financial derivative instruments, both of which may have the effect of increasing volatility.

Disclaimer

This information should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. It contains information and analysis that is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content of this document, no representation or warranty, express or implied, is made by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified. It should not be copied, forwarded, reproduced, divulged or otherwise distributed in any form whether by way of fax, email, oral or otherwise, in whole or in part without the express and prior written consent of Liontrust. Always research your own investments and if you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.