Heightened market volatility episodes have become more frequent in recent years with several fast and deep corrections. With a low volatility strategy, investors can stay invested while minimising the volatility in their portfolios. This way investors reduce the risk of exiting the market at the worst time and missing the market’s best days which can significantly lower their overall returns.

Quant strategies typically appeal for their structured, systematic and repeatable investing approach. By eliminating behavioural biases and relying instead on empirical evidence from huge chunks of data, quant-based investments are not clouded by human prejudices and personal preferences.

That said, non-quant practitioners point out that these strategies rely on past data which may not prepare a quant model to be sufficiently nimble to predict and adapt to future market events. COVID-19 is cited as one such example. Nevertheless, the evidence shows that a low volatility quant strategy (“low vol”) has delivered what it promises – delivering more stable returns than the market even during the severe COVID-induced drawdown and subsequent market rebound.

In 2021, when the delta COVID variant surged in Asia, the MSCI Asia ex Japan Minimum Volatility Index fell 5% between 18 March and 20 August, while the broader MSCI Asia ex Japan index fell 10.7%.1 This pattern was repeatedly visible throughout the year during the intermittent market drawdown episodes.

Rising volatility

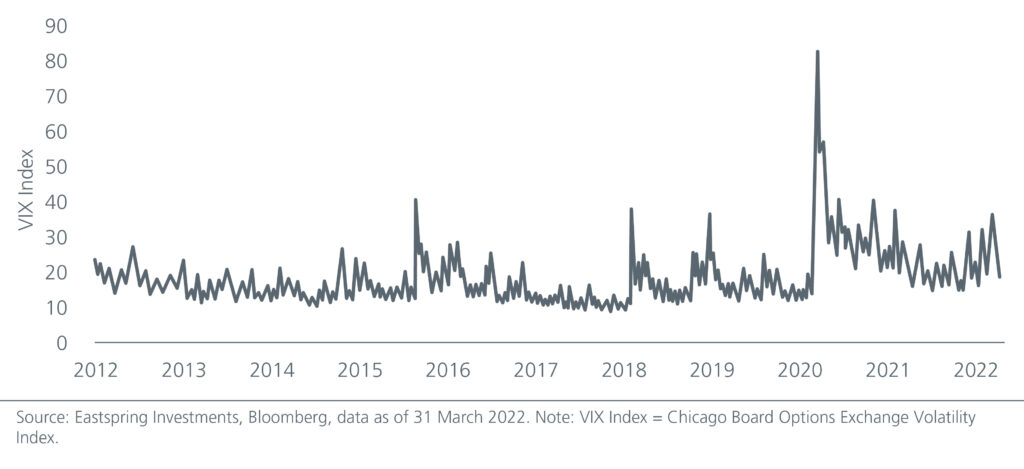

In recent years, bouts of heightened market volatility have become more frequent with several fast and deep corrections. These episodes can happen without much warning. Market expectations of volatility spiked in March 2020 and have remained at levels higher than we have seen for most of the last decade, initiated by the uncertainty over the COVID recovery. See Fig. 1.

Other factors that have caused recent market swings are global supply chain disruptions, China’s property market woes, the US Fed tightening, surging commodity, food, and energy prices and more recently the Russia-Ukraine crisis.

Fig. 1: Volatility has spiked since March 2020

In 2019, there were 42 days in which the MSCI Asia Pacific ex Japan index experienced swings of more than 1%. In 2020, this number more than doubled to 86. In the first quarter of 2022, there have already been 25 days of such swings.2

When such swings happen, investors who are unable to endure the pain of market corrections may decide to exit the market at precisely the worst time, thus potentially losing out on any sharp market reversal. Low vol strategies help to minimise the losses by falling less during turbulent times. Equally, such a strategy only needs to rise by a smaller magnitude to return to the same level. This effect compounds over time.

A strong case for low vol in Asia

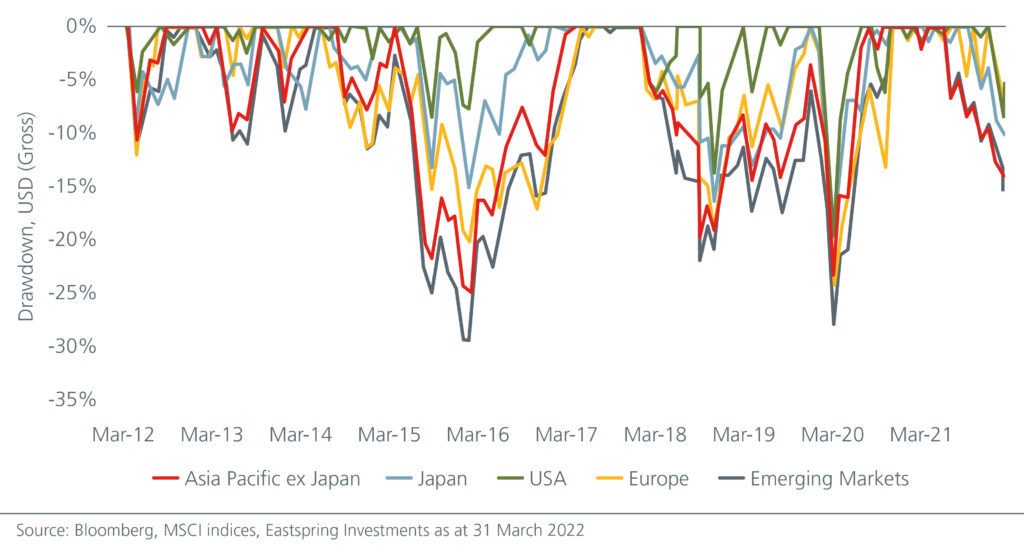

Emerging and Asian markets are typically more volatile than Developed markets. See Fig. 2. Over the past ten years, both EM and Asia experienced higher drawdowns than the US and Europe during periods of heightened volatility. The time taken to recover from these drawdowns is equally important. Over the same period, it took Asian markets 14 days, on average, to recover from the selloffs compared to 4 days for the US and 8 days for Europe.3 Given that Asia is vulnerable to a higher risk of drawdown and takes a longer time to recover, Asian low vol looks particularly compelling as an investment strategy to help investors better navigate market gyrations and stay invested over the long term.

Fig 2: Asian markets endure higher drawdowns

Separately, COVID has caused economic scarring in Asia. Although the region is still expected to grow by 5.2% in 2022 and 5.3% in 20234 on continued recovery in domestic demand and solid exports, the pace of recovery will not be even across the region given the varied nature of the economies. As Asian economies continue to develop and mature, there will be intermittent episodes of economic rebalancing which can trigger market volatility. China’s 2021 regulatory clampdown on property and other sectors is a case in point. Investors who desire a broader Asian equity exposure can consider complementing their portfolios with an Asian low vol strategy.

Rate hikes appear to be brushed aside

Concerns over rapid rises in US rates have rattled Asian stocks in recent months. To cool US inflation, the US Federal Reserve (“US Fed”) has indicated it might have to raise interest rates more aggressively than it had originally thought. Investors are understandably concerned about the downward pressure on economic growth from higher interest rates.

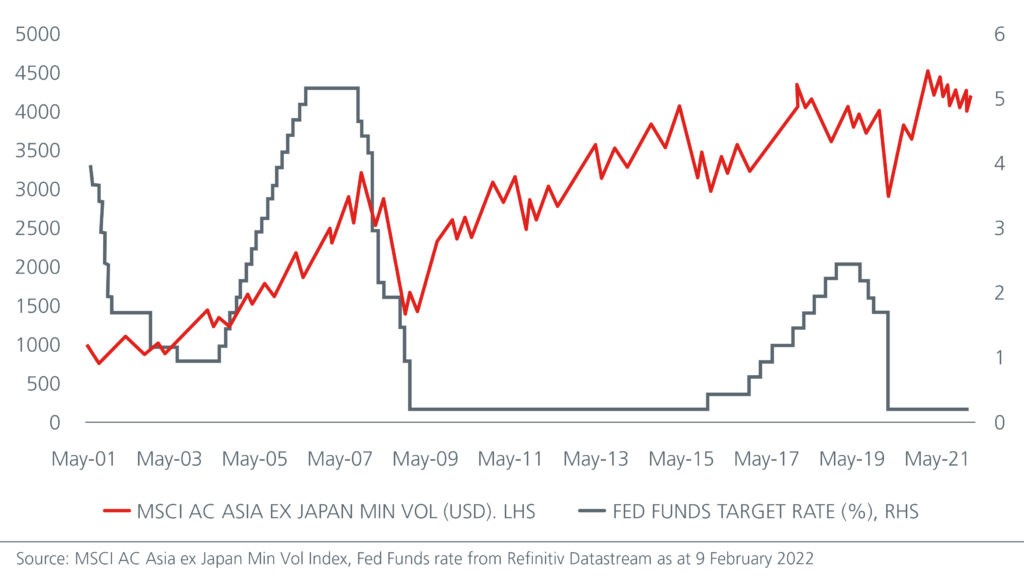

The last time the US Fed took on an aggressive stance was between 30 June 2004 and 29 June 2006, during which time rates were hiked by 425 basis points from 1% to 5.25%. During this period, the MSCI Asia ex Japan Minimum Vol Index still returned 26%. See Fig. 3.

Fig 3: Asian low vol held up well during past rate hikes

An inflation buffer

Low volatility stocks are usually found in defensive sectors and are typically mature companies with stable earnings, predictable cash flows and high dividends. Dividend paying companies are a buffer in an inflationary environment, providing more immediate return of capital and proof of a company’s cash-generating ability.

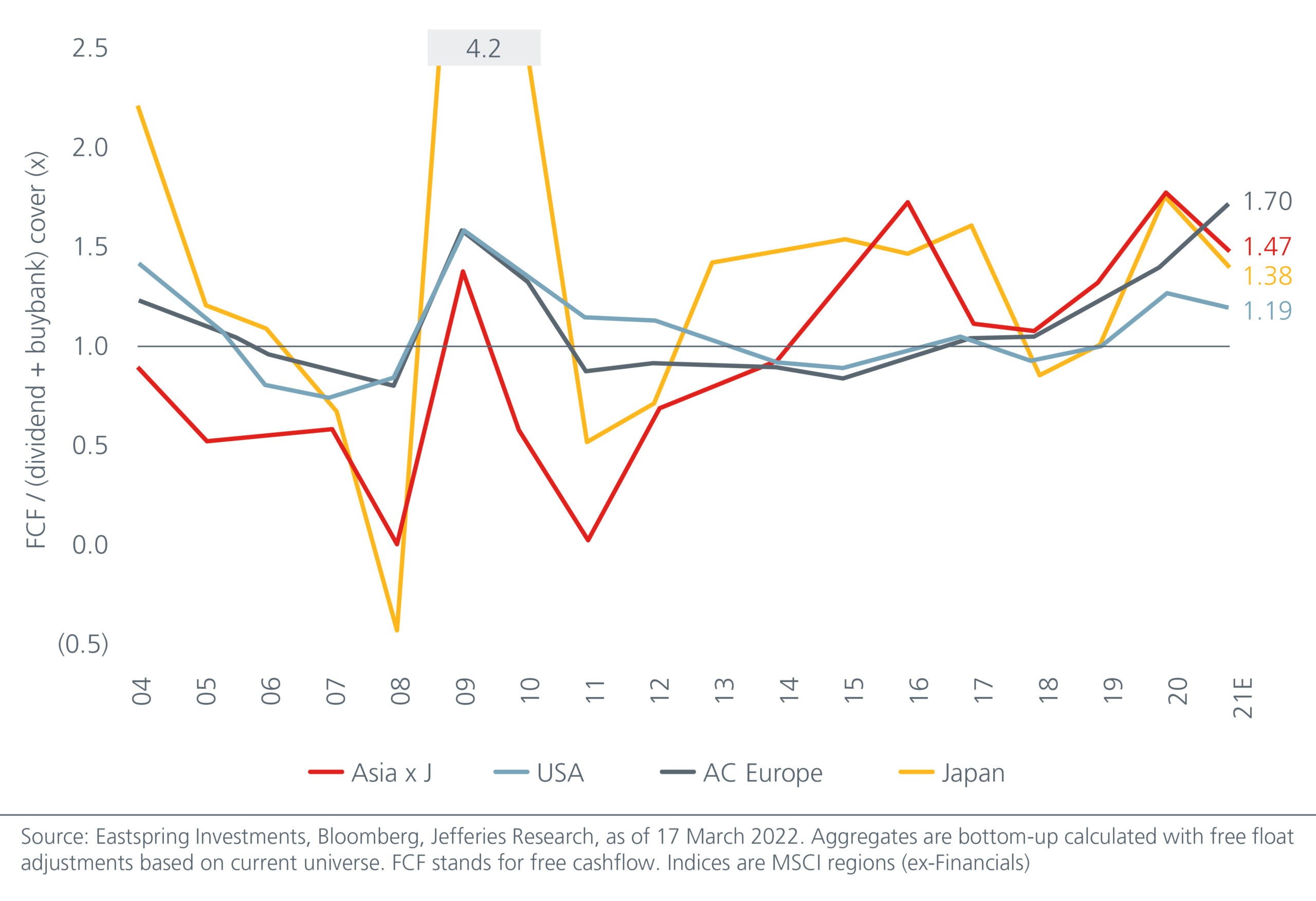

Dividend income is also a long-term driver of Asia’s equity returns. Furthermore, Asia ex Japan companies have the highest aggregate free cashflow cover ratio, suggesting that dividends are well supported by robust balance sheets. See Fig. 4.

Fig 4: Asia ex Japan’s free cashflow cover above 1x since 2013

The number of stocks in Asia Pacific ex Japan that have dividend yields above 3% is almost twice that of Europe and more than 3x that of the US5. A careful selection of good quality, dividend paying low volatility stocks can therefore cushion against rising inflation.

A low vol portfolio ≠ a portfolio of low vol stocks

While the benefits of low vol strategies are evident, a key drawback cited is that they tend to lag when the market rallies quickly. COVID, too, highlighted that relying on a single factor approach i.e., low vol, may not be always be effective in achieving the lower drawdowns yet broader market participation that many investors desire.

This is why an approach which considers a large universe of stocks rather than only focusing on stocks with low vol characteristics is preferable. Thus, the resulting portfolio benefits from greater opportunities to add alpha through stocks with attractive fundamental characteristics and then leverages an advanced portfolio construction approach to arrive at a low volatility portfolio.

This process ultimately yields well-diversified exposure across sectors, countries, industries, and stocks and culminates in a low vol portfolio, not a portfolio of low vol stocks. Long-term investors who wish to remain fully invested in Asia even during periods of elevated volatility can consider complementing their asset allocation with low volatility strategies to help manage the risk of drawdown in choppy market regimes.

This is the sixth of a series of eight articles which examines the different investment strategies investors can adopt to tap on the opportunities that are emerging in Asia

Footnotes

Sources:

1 Refinitiv Datastream, MSCI indices, Eastspring Investments as of 31 December 2021

2 Bloomberg, MSCI Asia Pacific ex Japan index, Eastspring Investments as of 31 March 2022

3 eVestment, Eastspring Investments as of 31 March 2022

4 Asian Development Bank, April 2022

5 MSCI indices and companies are constituents of MSCI World Index, as of March 2022

Disclimer

This document is produced by Eastspring Investments (Singapore) Limited and issued in:

Singapore and Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws.

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (531241-U).

This document is produced by Eastspring Investments (Singapore) Limited and issued in Thailand by TMB Asset Management Co., Ltd. Investment contains certain risks; investors are advised to carefully study the related information before investing. The past performance of any the fund is not indicative of future performance.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

United Kingdom (for professional clients only) by Eastspring Investments (Luxembourg) S.A. – UK Branch, 10 Lower Thames Street, London EC3R 6AF.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author on this page, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this posting is at the sole discretion of the reader. Please consult your own professional adviser before investing.

Investment involves risk. Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments (excluding JV companies) companies are ultimately wholly-owned/indirect subsidiaries/associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company, a subsidiary of M&G plc (a company incorporated in the United Kingdom).