Real Estate Investment Trusts (REITs) are a great way to diversify your portfolio. For starters, many are publicly traded companies that own and manage a portfolio of real estate assets. This means you don’t need millions of pounds to purchase physical property and get exposure to the sector – they provide access to a variety of real estate investments that would otherwise not easily be available to individual investors.

The assets they invest in include the likes of student accommodation, self-storage facilities, warehouses, and data centres, which means a wide range of investors can also easily diversify their real estate portfolios and reduce risk. What’s more, as REITs are liquid investments, you can easily adjust your allocation as required.

Long-term lower correlation

A further diversification benefit of REITs – their lower correlation with other assets – is less understood, predominantly because of the way REITs react in the short-term vs the long term.

As publicly traded companies, many REITs are susceptible to short-term market sentiment, as we have witnessed all too well over the past few months. When markets go risk-off, equity sell-offs take REITs down too. Over the very long term, however, REITs have a lower correlation to equities and are far more correlated to the underlying real estate assets.

This is borne out by research carried out by Routledge (Tayor & Francis Group)* and Nareit**.

Research for the buy and hold investor

Routledge looked at broad REIT return characteristics versus the broad direct real estate markets over a 20+ year period. It used data for six countries (Australia, France, Germany, Netherlands, the U.K., and the U.S.), accounting for over 70% of the free float of REIT market capitalisation in the developed world.

The results indicated that, as might be expected, REIT returns correlate strongly with stock returns in the short term. However, over the mid to long horizon, listed real estate returns tend to co-move with returns from the real estate market and the correlation with stock returns is weaker.

Routledge said that if listed and direct real estate returns are generated by a common ‘real estate factor’ over the long term, “then listed real estate securities are expected to provide similar returns and return volatilities and the same diversification benefits as direct real estate in a mixed-asset portfolio of a long-horizon buy-and-hold investor.”

They concluded that, as a result, “listed real estate investments would then constitute an appealing avenue for investing in the asset class given the flexibility, liquidity, and low transaction costs of such investments.”

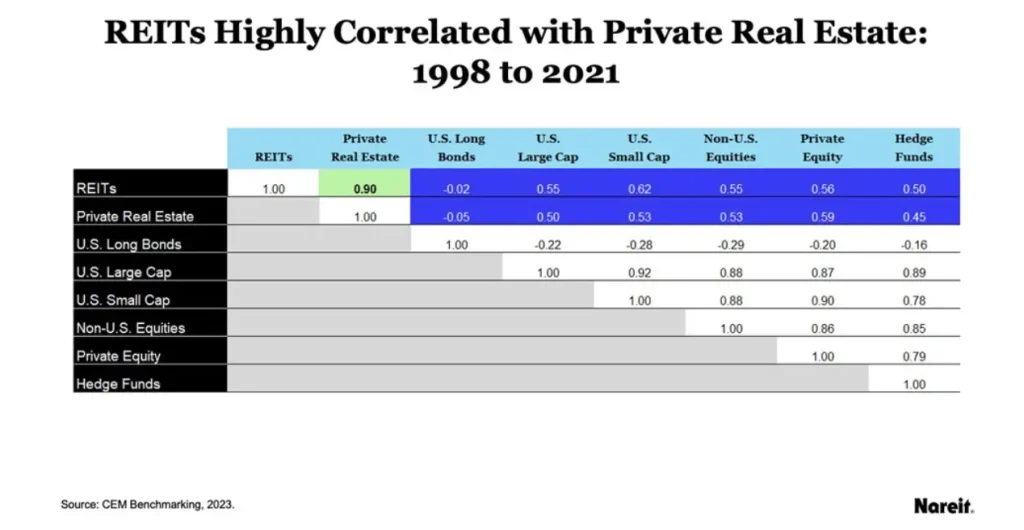

In the US, Nareit sponsored CEM Benchmarking’s 2023 study, which provided a comprehensive look at realised investment performance across asset classes over a 24-year period (1998–2021).

REITs outperform all other real estate styles in that period, and the study showed that while REIT and unlisted real estate returns were highly correlated when illiquid returns were adjusted for reporting lags (0.90), they had relatively low correlations with bonds (-0.02) and listed equity returns (0.55), implying good diversification benefits and strong risk-adjusted returns.

Investing in the next generation of real estate

Investing in property has formed a core element of portfolio construction for years, but times and the sector are changing. Investors need to make sure they are focusing on the next generation of real estate, not the last.

In our view, there are four powerful socio-economic mega trends in play: ageing population, digitalisation, generation rent, and urbanisation. Thankfully, there are plenty of specialist UK REITs investing in these areas.

Important information

This article has been prepared by Gravis Advisory Limited (“the Investment Adviser”) and is for information purposes only. It is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Any recipients outside the UK should inform themselves of and observe any applicable legal or regulatory requirements in their jurisdiction.

This article should not be considered as a recommendation, invitation, or inducement that any investor should subscribe for, dispose of, or purchase any securities or enter into any other transaction with the VT Gravis Real Assets ICVC, or any other Fund affiliated with the Investment Adviser. The merits and suitability of any investment action in relation to securities should be considered carefully and involve, among other things, an assessment of the legal, tax, accounting, regulatory, financial, credit and other related aspects of such securities.

Although high standards have been used in the preparation of the information, analysis, views, and projections presented, no responsibility or liability whatsoever can be accepted by the Investment Adviser for any errors, omissions, misstatements, loss, or damage resultant from any use of, reliance on, or reference to the contents. The views and opinions contained herein may not necessarily represent views expressed or reflected in other Gravis communications, strategies or funds and are subject to change.

The VT Gravis UK Listed Property (PAIF) Fund is a UK Non-UCITS Retail Scheme (NURS) Open Ended Investment Company (OEIC) with Property Authorised Investment Fund (PAIF) status.

Past performance is no guarantee of future performance.

Gravis Advisory Limited is authorised and regulated by the Financial Conduct Authority. Gravis Advisory Limited’s principal place of business is: 24 Savile Row, London, W1S 2ES.