The globe’s growing demand for energy and concerns over climate change are driving the need for renewables and related low-emission technologies. At Baillie Gifford, we’re on the lookout for companies that can gain a competitive edge and generate strong returns by leading the way.

Existing holdings across our clients’ portfolios include makers of wind turbines, solar panels, electric vehicle batteries and hydrogen electrolysers, such as Vestas, LONGi, Northvolt and Nel. They also comprise suppliers of aluminium, nickel, lithium and other raw materials, including Rio Tinto, PT Vale Indonesia and Albemarle. And while we believe renewables have superior long-term growth prospects to fossil fuels, hydrocarbon companies can still play a critical role. For example, Reliance is reinvesting its oil refining profits into developing cutting-edge hydrogen fuel cells and solar panels.

As long-term growth investors, we’re excited about these companies’ potential and intend to explore further opportunities for years to come.

We believe many of the factors that led ‘cleantech’ innovators to underperform financially in the early 2000s are now behind us. But we’re aware that three concerns need to be addressed:

- Renewable electricity sources need to demonstrate that they can scale to meet different types of energy demand.

- Companies need to spend significant sums on physical infrastructure, requiring investors to support firms that are capital intensive.

- Governments and companies need to have confidence in the advantages of a fast energy transition to overcome caution and inertia.

We can’t yet know exactly how the energy and climate transition will unfold over the next five, 10, let alone 50 years. But we should expect the unexpected. We should be open to scenario analysis that challenges incremental thinking and explores the complexities of the deep systems changes that likely lie ahead.

A recent study from Oxford University’s Institute for New Economic Thinking (INET Oxford) provides one such opportunity. It challenges consensus forecasts, suggesting they don’t properly account for the implications of long-term exponential growth.

The work is well-founded and calls to mind how progress in computing and the internet caught many by surprise. Moreover, the researchers involved are highly credible, including Prof J Doyne Farmer, a complex systems scientist whose work we sponsor and who recently joined us to discuss the findings.

The academics ask why other studies repeatedly underestimated the deployment of renewable energy technologies and overestimated their costs. They conclude that models relied on by the International Energy Agency (IEA) and the Intergovernmental Panel on Climate Change, among others, are unduly pessimistic about future trends in renewables and carbon emissions. Moreover, the researchers propose that a rapid shift to renewable technologies could save society trillions of dollars.

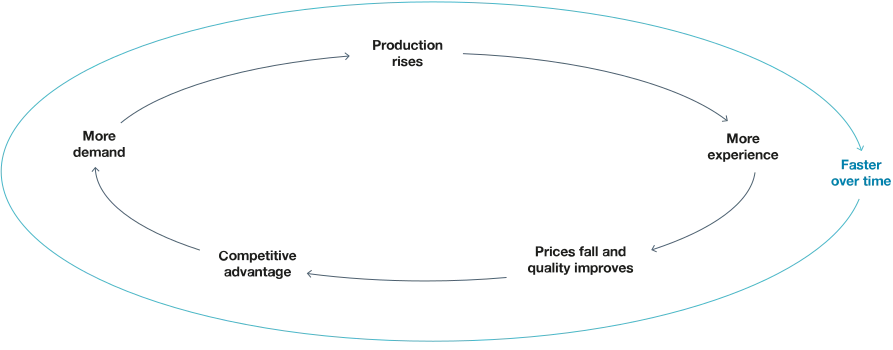

The feedback flywheel

The authors base their approach on Wright’s Law. You can read more about it below. But the key insight is that a ‘learning curve’ applies to wind turbines, solar panels and other renewable technologies: for each cumulative doubling in production, the cost of manufacturing each unit falls by a constant percentage.

That gives rise to a virtuous feedback cycle: resulting price drops stimulate demand, leading to efficiency gains, allowing manufacturers to cut prices further, and so on. And because the price cuts are exponential, the loop speeds up as it goes.

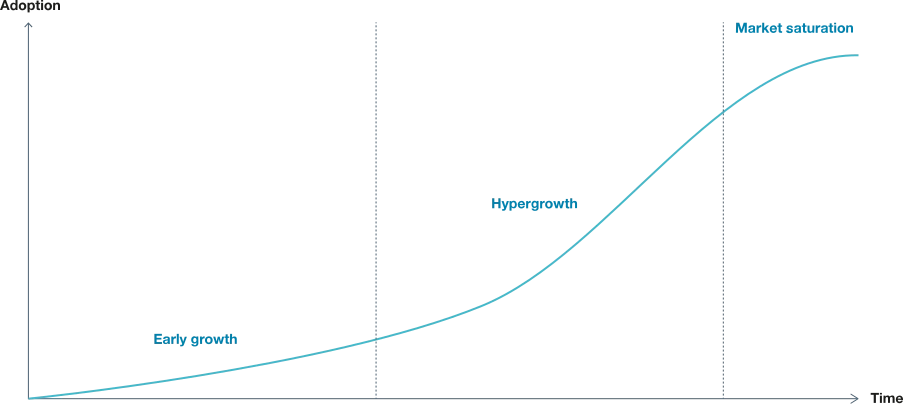

One consequence is that deployments of successful technologies tend to follow an S-curve. Early growth seems slow as the exponential effect takes time to build. Then a period of ‘hypergrowth’ takes hold.

The bigger the market size, the longer hypergrowth endures before demand eventually tapers off as the market gets saturated.

The S-curve model of technological deployment

However, fossil fuels don’t benefit from the same effect. While engineers have continually improved extraction processes, the need to work in ever-more extreme environments as resources become harder to find cancels out the savings. In addition, for 50 years the actions of the OPEC cartel have added social and political complexities to the market prices of these energy commodities. As a result, oil, gas and coal prices are roughly the same as they were 140 years ago, once you adjust for inflation.

The key message here is that renewable energy is a technology, while fossil energy is a commodity. Technologies can access learning curves and persistent cost deflation. Commodities, it seems, cannot.

Wright’s Law

Theodore Wright was involved in the design of military, civilian and racing aircraft when he developed his formula.

He was determined to tease out the relationship between the cost of manufacturing a plane and the number of units produced. In 1936, after 14 years of study, he published his findings. They detailed a ‘curve relationship’: for every doubling of the quantity of aircraft made, production costs (ie labour, materials, factory overheads) fell by a constant percentage. In effect, the more planes workers made, the more they learned.

Wright deduced the ‘learning rate’ for the aircraft he studied resulted in a 10–17 per cent cost drop each time the number built doubled. The rate varied as the cost of raw and purchased materials took on greater importance as production increased. Follow-up studies by others observed the relationship applied to other technologies, from semiconductors to electric car batteries, albeit with different learning rates.

Wright went on to head the US’s efforts to increase plane production during World War Two. But his ‘law’ may be his most enduring legacy. About four decades after his death, researchers at MIT and the Santa Fe Institute found it to be more accurate than five rival progress-predicting formulas.

Improved model

INET Oxford’s paper suggests the IEA and others underestimate renewables’ falling costs because their ‘deterministic methods’ struggle to incorporate how technologies sometimes advance in a slightly volatile manner. By contrast, INET Oxford’s work takes a ‘probabilistic’ approach. When back-tested, it seems to better deal with the ‘bumpiness’ encountered.

Just as importantly, Farmer and his colleagues claim that these earlier studies applied excessive ‘ad hoc’ constraints. Their forecasts imposed floors on the amount that renewable prices could drop and limited expected deployment rates, despite this running contrary to an increasing catalogue of lived experience. This effectively puts the brakes on the two key driving forces of the feedback loop described earlier.

The study argues that artificially blocking off plausible future pathways led the other predictions astray. Take solar panel systems, for example. The paper analysed more than 2,900 investment cost projections for the technology between 2010 and 2020:

- The mean annual expected cost saving was 2.6 per cent

- None of the projections was more than 6 per cent

- But the actual yearly saving turned out to be 15 per cent

Over 10 years of compounding, that’s the difference between about a 20 per cent cost saving and an 80 per cent cost collapse. The discrepancy helps explain why it’s been a surprise that new solar and onshore wind projects are now estimated to be at least 40 per cent below the equivalent cost of new-build coal and gas-fired power facilities.

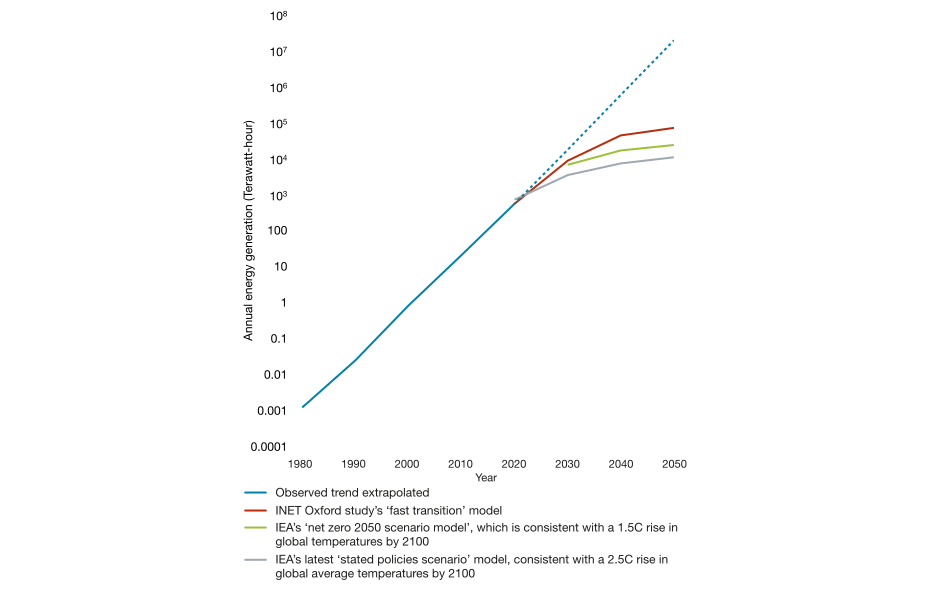

The new methodology retrospectively models past saving more accurately. And it gives more optimistic projections of renewables’ use in the future.

A more optimistic model of solar power use

The INET Oxford study’s cost-led fast transition model anticipates that solar power use could outpace the International Energy Agency’s most optimistic, policy-led predictions. Farmer and his colleagues took steps to temper its outlook to help it stand up to scrutiny. But extrapolating onwards from the observable trend points to the possibility of even greater use of solar.

The rapid uptake envisaged has the dual benefit of creating potentially significant returns for investors and large savings for society in general. The sums involved are huge.

The paper suggests that a fast transition to renewables would save the world about $12tn by 2050 compared to maintaining the status quo. That’s even after allowing for the requirement of a more complex electricity grid, which it estimates would cost an additional $140bn a year to run. Given that fossil fuels are a limited resource, there’s a good chance that the longer we remain reliant on them at scale, the more likely their prices will rise. So even the $12tn figure may be an underestimate.

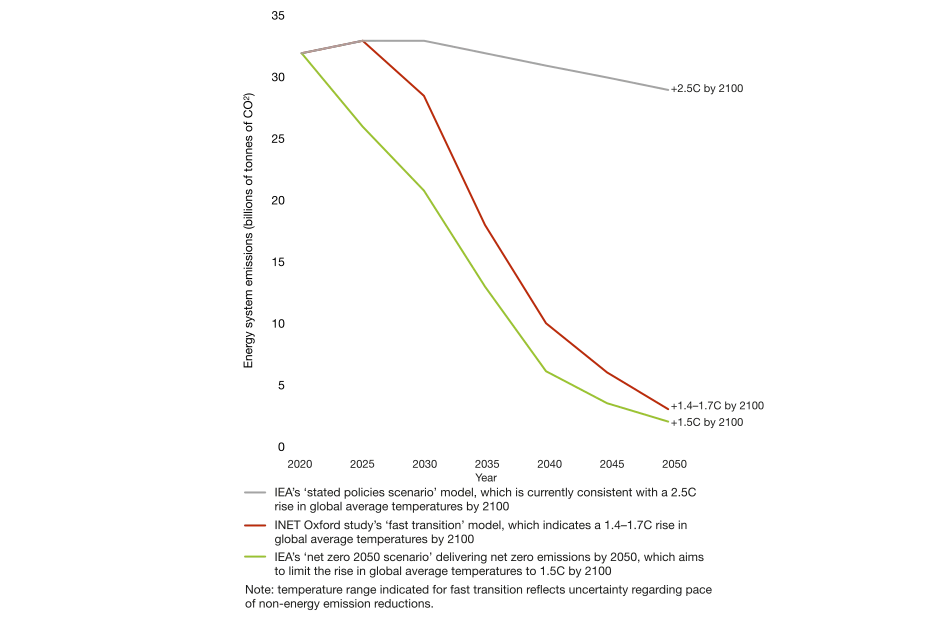

The study also indicates energy system emissions would fall off a cliff during the 2030s under its fast transition model after declining by only about 10 per cent during the 2020s. This reflects the slow-then-sudden nature of exponential change. And it highlights why we shouldn’t necessarily despair if emission reductions remain relatively subdued in the near term.

There isn’t a pre-determined successful emissions pathway to a fully decarbonised 2050. We have some very effective technologies ready for mass installation, and we should expect continual innovation. So while climate science suggests that we should all work towards the fastest reduction possible, a slow start doesn’t rule out rapid acceleration to come.

Comparing energy system emissions under different models

The INET Oxford study suggests emissions could remain pretty constant this decade before falling steeply in the 2030s. By 2050, it indicates they could nearly match the IEA’s deterministic and policy-led ‘net zero 2050 scenario model’, which is constructed on the basis of sequential reductions from today forward. Note the temperature range indicated for INET Oxford’s ‘fast transition’ reflects uncertainty regarding the pace of non-energy emission reductions.

Investment implications

As described above, the forces driving renewables may be stronger than generally recognised, creating the potential for us to produce substantial returns for our clients.

We believe that if we used a top-down method to construct portfolios based on a fixed view of technology and its pace of adoption, we’d blind ourselves to the potential of individual companies and regions. Instead, we favour a bottom-up approach that lets us focus on finding transformative businesses that can deliver long-term growth.

We’re mindful that Farmer’s paper provides us with scenarios, not forecasts. But they appear to have some interestingly robust foundations compared to ‘consensus models’. Some further ramifications follow:

- There are exceptional companies to invest in that we believe will accelerate the energy transition over the medium to long term. They may work in different niches and be at different stages of their lifecycle today, but all offer the potential for significant long-term returns. Examples include the electric car maker NIO and the iron ore miner FMG, which is investing in the switch from coal and natural gas to solar and hydrogen.

- Greater use of renewables could provide a world with abundant, low-cost energy. That should support developing countries and will make some business models profitable for the first time. Some could even aid efforts to ultimately reverse global warming. For example, Climeworks is pioneering a way to use low-cost electricity to remove carbon dioxide from the air and store it underground.

- Another consequence of a faster-than-expected transition is that electricity grids will have to deal with lots more complexity sooner than anticipated. That creates an opportunity for providers of the software and hardware to manage it. We have found such potential in companies as diverse as the electric cable manufacturer Nexans and the internet services provider Cloudflare.

- Just as exponential growth can bring about rapid changes in our use of renewables, so might it cause a tipping point in public policy. We’ve seen in the past how change often occurs via massive dislocations rather than small increments – the formation of the UK’s publicly funded National Health Service is one example. Likewise, the acceleration of extreme weather and climate damages could spur lawmakers to take sudden action against carbon-intensive activities via taxes and other regulations. Unprepared companies could experience significant value destruction.

There’s much to consider. Baillie Gifford’s advantage is that we aim to invest in companies for 5 to 10 years or longer. This period gives the exponential effects described above time to deliver meaningful change. By taking this patient approach, we can support transformative companies to drive forward the energy transition in the hope of delivering strong returns for our clients.

Lessons from the lily pond

To better understand the implications of exponential change for emissions, we can call on a famous analogy used in schools to convey the concept.

A patch of lily pads in a pond doubles in size every month. By the end of the year, they cover the entire stretch of water. How many months did it take to for them to cover the final half of the pond?

The answer is not six months, as many kids guess, but one. In fact, after half a year, the impact on the frog’s home would barely be noticeable: they would cover less than two per cent of the pond. But the trend’s future implications would be profound.

The same effect comes to play even if the expansion rate is slower. Suppose a slightly more complex scenario:

A 500m2 pond covered in 1m2 of lilies growing by 20 per cent each month.

The lesson: just because growth may seem to get off to a slow start doesn’t mean that exponential forces won’t eventually dominate.