The Swiss National Bank (SNB) cut the policy rate by 0.25%, partially disappointing market expectations. In this Macro Flash Note, Senior Economist GianLuigi Mandruzzato discusses the outlook for Swiss monetary policy in light of the latest SNB decision.

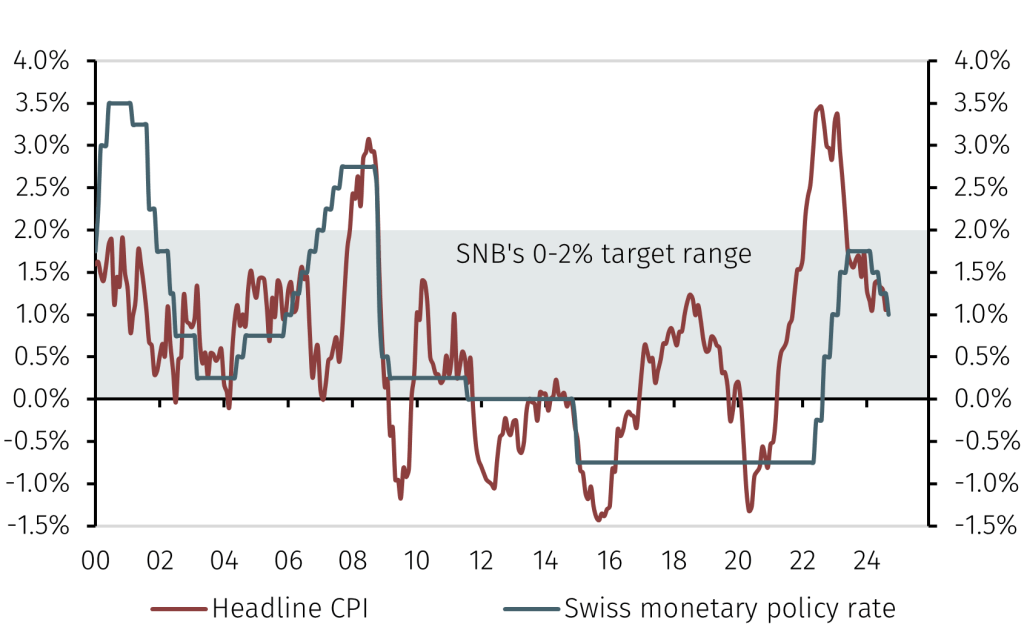

The SNB has reduced the policy rate by 0.25% to 1.00% (see Chart 1). Compared to market expectations, which discounted the possibility of a 0.50% cut at 50%, the decision is slightly less expansionary, which explains the moderate appreciation of the exchange rate following the SNB’s announcement.

Chart 1. Swiss inflation and interest rates

Source: SNB, LSEG Data & Analytics, and EFGAM calculations. Data as at 26 September 2024.

However, the decision to continue to gradually adjust monetary policy appears consistent with recent developments in the Swiss economy. Furthermore, the SNB began reducing interest rates in March, ahead of other major central banks, and now has more flexibility to recalibrate monetary policy.

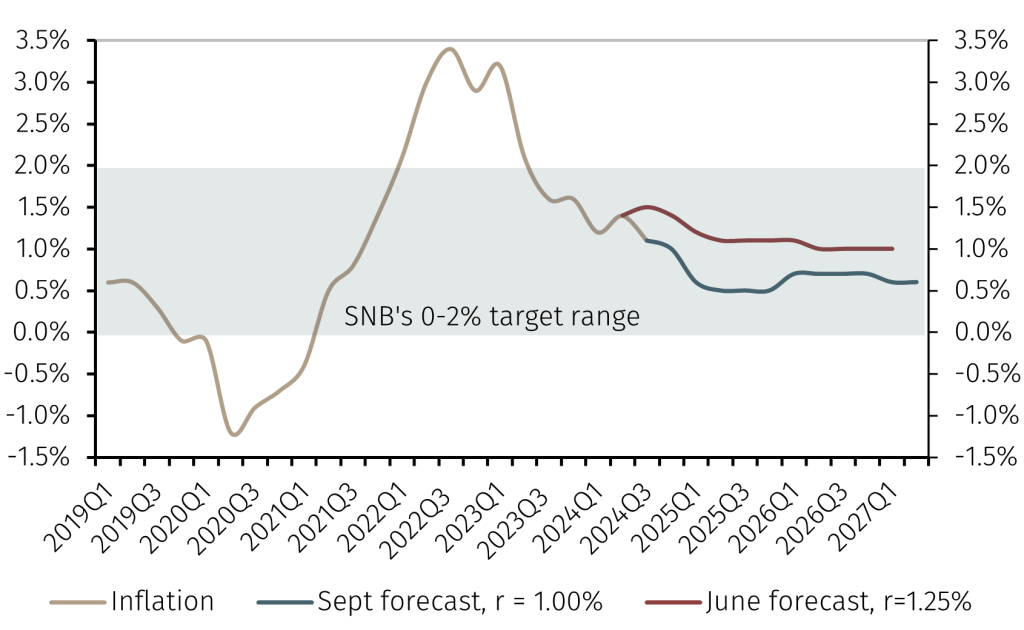

The SNB has significantly revised downwards its conditional inflation forecasts for 2025-26 to 0.6% and 0.7% respectively (see Chart 2)1. The drivers behind the lower inflation expectations are: the appreciation of the Swiss franc over the summer, the drop in oil prices and the reduction in Swiss electricity tariffs that will come into effect in January 2025. Furthermore, the prospect of gross domestic product growth in line with or slightly below potential, and still subject to mainly downside risks, will help to limit inflationary pressures in the coming quarters.2

Chart 2. SNB conditional inflation forecast (year-on-year)

Source: SNB, LSEG Data & Analytics, and EFGAM calculations. Data as at 26 September 2024.

The macroeconomic picture therefore supports the expectation of further rate cuts. We expect another 0.25% reduction in the policy rate to be announced after the next SNB meeting in December. In addition, a further downward adjustment of the policy rate to 0.50% cannot be ruled out in the first part of 2025. If the SNB’s conditional inflation forecasts proves right, such an interest rate path would keep the real interest rate, adjusted for headline consumer inflation, around the SNB’s estimate of the neutral rate around zero.

This scenario is also supported by the comments of the SNB which noted that “further cuts in the policy rate may become necessary in coming quarters”, an unusually explicit signal about future monetary policy moves. In addition to interest rate changes, the central bank reiterated its intention to intervene in the foreign exchange market in order to maintain price stability, likely focusing on preventing an overly rapid rise in the Swiss franc exchange rate.

1 See “Good news on Swiss electricity prices”, EFG Macro Flash Note, 19 July 2024.

2 See “Swiss summertime blues”, EFG Macro Flash Note, 13 August 2024.