We compare the redhead of 90s pop with today’s red-hot inflation expectations.

For those of a certain vintage, Sonia is an auburn-haired, diminutive Liverpudlian singer from the early 1990s. She had a number one single with ‘You’ll never stop me loving you’, represented the UK at Eurovision (coming second), and contributed to Band Aid II’s ‘Do they know it’s Christmas?’

For those with an interest in the fixed income markets, SONIA is the sterling overnight index average. It is the average interest rate paid by banks to borrow sterling overnight from other financial institutions. Since LIBOR’s fall from grace after the global financial crisis, derivative contracts tied to SONIA have formed the bedrock of market expectations for Bank of England (BoE) policy rates.

Pumping (down) the gas

SONIA, unlike Sonia, rarely sets pulses racing. However, that changed this month. Firstly, the BoE raised interest rates by 50 basis points at their policy meeting on 4 August. That was the biggest increase in nearly 30 years despite a set of deeply gloomy economic projections. Secondly, SONIA futures have collapsed in the subsequent three weeks. SONIA futures for December 2023 (i.e. a good proxy for the market’s expectation of where BoE policy rates will land at the end of next year) have moved an eye-watering 150 basis points. Expectations for December this year have jumped by nearly 75 basis points. A repricing of that magnitude in such a short period of time is exceptionally rare.

Why the drama, and what does it imply? The triggers for the repricing are partly data driven. We had stronger CPI and labour market data landing in the middle of the month. But the clearer explanation is yet another round of gas price hikes. As gas prices spiral, expectations for household bills over the winter have risen to eye-popping (and budget-busting) levels. A doubling or even tripling of the average household fuel bill now looks perfectly plausible. The impact on household finances will be massively dependent on the policy choices of the next government, but we know that somebody has to pay for the huge negative terms of trade shock being endured by the UK.

Unemployment or worse?

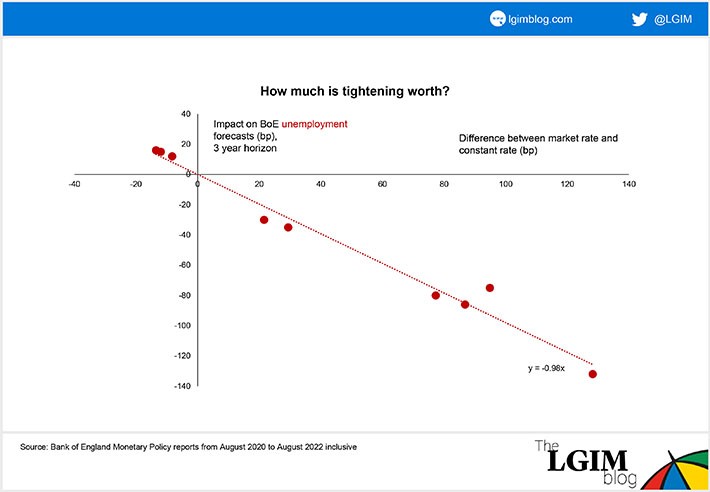

The repricing of SONIA is adding fuel to the fire of the recessionary outlook. Higher interest rates imply even more pain is set to be heaped upon households, particularly those with mortgages that are either floating rate or need imminent refinancing. On the BoE’s own estimates, the extra 150 basis points on short-term rates is likely to push unemployment up by around the same amount (see the chart below). Their early August forecast had unemployment rising to 6.3% in 2023 (from the current 3.8%). Marking those forecasts to market would push the peak to around 8%. That’s getting very close to the level of joblessness experienced in the wake of the global financial crisis.

At Eurovision (1993), Sonia told us that it’s often a case of ‘Better the devil you know’. For the BoE, the devil it knows is unemployment. No policymaker welcomes putting people out of work or causing distress in the mortgage market, but it is seen as a price worth paying to keep the ‘devil we don’t know’ (unhinged inflation expectations) at bay.

Maybe the new government can wave a policy wand and spread out the impact of the energy price shock over multiple years as proposed by various industry bodies? But, for now, the interest rate shock on its own is getting big enough to upend the labour market.