South East (SE) Asia is one of the most exciting regions for investors in the emerging markets universe, with many companies offering attractive and compounding multi-year growth prospects. From Indonesia’s digital economy to Vietnam’s IT services hubs, SE Asia offers opportunities across a broad range of sectors, with hungry entrepreneurs and unique business models.

Revisiting the SE Asia case

With a combined population of over 4.8 billion people, Asia is by far the most populated region on the planet. Even after the 2.8 billion combined population of India and China, SE Asia is still home to a further 700 million people and the continuing demographic trends will continue to drive growth in the region for decades to come.

From a corporate perspective, SE Asia represents currently:

Beyond its size, SE Asia is also emerging as a dynamic economic powerhouse thanks to its robust macroeconomic fundamentals and growth potential. Investors who once saw the region as a proxy for commodities are now discovering its richness in diverse sectors, underpinned by strong economic indicators. Indeed, SE Asian countries posted a GDP growth of 4.6% in 2024, compared with a 1.8% growth for advanced economies according to IMF data2.

Economically, the region continues to move from strength to strength. Many SE Asian countries have in the past decade followed orthodox fiscal policies, reducing deficits, and limiting currency depreciation, successfully addressing their vulnerabilities to produce a favourable investment environment.

From a bottom-up perspective, SE Asia offers fertile ground for stock picking. Many sectors remain underpenetrated, providing room for companies to grow faster than the broader economy. The standout companies in each sector also offer compounding growth, making for compelling long-term investment opportunities for diligent stock pickers like Carmignac.

In our view, SE Asia has emerged as a clear winner in the rebalancing of global trade and supply chains. Multinationals from Asia and beyond have been relying more on the region as a key production base for a range of sectors, in a shift that spiked with the Covid-19 pandemic and has accelerated amid ongoing geopolitical uncertainties. As a result, FDI inflows into the ASEAN region have significantly increased over recent years. Between 2021 and 2023, ASEAN averaged $220bn of foreign investment per year3, reaching a record $230bn in 2024.

With the US-China tensions on one side, Europe-China tensions on the other side, SE Asia is maintaining its appealing positioning for multinational companies looking to diversify their supply chains, relying on its key strengths. Indeed, the region has several competitive advantages that make the region compelling in the eyes of multinationals firms: Cheap and qualified workforce, decent and growing infrastructure, political stability, and access to key commodities.

This contrasts with some African countries that may lack key infrastructure networks and face political instability. Likewise, the political pendulum in Latin America has been swinging significantly and the region is lesser integrated in global supply chains compared to SE Asia.

While a cheap and abundant supply of labour has helped the emerging economies of the ASEAN region to attract low-cost and labour-intensive manufacturing, the focus is quickly shifting to higher value-added industries with many ASEAN countries expanding their manufacturing footprint in sectors like electronics, semiconductors, machinery, electric vehicles and batteries, and pharmaceuticals.

“SE Asia has several competitive advantages that make the region compelling in the eyes of multinationals firms: Cheap and qualified workforce, decent and growing infrastructure, political stability, and access to key commodities.”

From US and Asia’s tech giants to China’s unicorns, billions are pouring into the SE Asian economies. International companies such as Samsung and Apple are not only expanding production in Vietnam4, but are also building research and development (R&D) hubs in the country5. Malaysia has emerged as a major target for business growth in semiconductors, with global giants such as Intel and Infineon having committed to investing billions in the country5. In order to leverage this trend, the government plans to train and upskill more than 50 000 Malaysian engineers to position the country as a semiconductor R&D hub5.

In Thailand, which has already established strengths in packaged foods5 and the production of automobiles for major global brands, the pharmaceuticals industry is shifting from primarily producing generics to developing treatments of its own5. The Philippines is making an aggressive push for foreign investment, which could shore up its strengths in business process outsourcing and the manufacturing of electronics and technology components5. And Indonesia is on its way to parlaying its massive nickel reserves – which are key to global electric vehicle (EV) supply chains – to become a major producer of EVs and EV batteries in its own right.

Chinese flagship tech giants have been looking at the ASEAN market for expansion. SE Asia represents a strategic market in the race to global market dominance and the growing pressure is visible in the huge efforts companies such as Alibaba and Tencent are making in order to secure their shares in the market and ward off incoming threats from Amazon and Facebook in Asia.

The establishment of the $100 billion Asian Infrastructure Investment Bank (AIIB), the New Development Bank (former BRICS bank), and, particularly, “One Belt, One Road” (OBOR, now simply Belt and Road Initiative), have significantly increased the amount of capital in the region, as well as the cooperation between China and its neighbouring countries. Ports, highways, and railways are being built or expanded across the entire region. The gigantic network, once completed, is expected to extend from China to the Netherlands, through the Middle East, Singapore, Africa. Surely, the project has not been short of scepticism addressing operational delays, budget inflation, and environmental issues, but the size of the endeavour gives a fairly good idea of the direction which China and its neighbours are heading in.

Going forward, we believe that SE Asia is looking very well positioned to become the major beneficiary of the ongoing supply chain realignment, becoming the “plus one” alongside India when multinationals are considering their “China+1” manufacturing strategy but also becoming the “plus one” partner of China, thus benefiting on all fronts.

Indonesia: Sparkling gem of the ASEAN region

As SE Asia’s largest economy, Indonesia has navigated global challenges including trade wars and the pandemic with impressive resilience. Key factors – a young workforce, abundant natural resources, particularly as the largest producer of energy-transition-critical nickel – and fiscal discipline have transformed Indonesia into a robust growth story.

The country’s recent economic achievements are particularly compelling. Inflation has eased significantly since the global 2021-2022 shocks, falling to near-record lows (CPI Inflation standing at 0.8% as of end of January 20256), enabling Bank Indonesia to begin its easing cycle, which should support the Indonesian equity markets going forwards.

Reforms supporting digitisation and future-focused sectors including electric vehicle battery production have further cemented Indonesia’s role in the global economy, in line with emerging mega-trends. Meanwhile, on the political side, following the presidential election last year, there seems to be a smooth transition between the former president Jokowi and the General Prabowo Subianto, bringing some political stability to the country. With the new government’s pro-growth agenda, prospects look solid in Indonesia.

INVESTMENT CASE: SEA LIMITED

Sea Limited (Sea), headquartered in Singapore with a significant footprint in Indonesia, exemplifies SE Asia and Indonesia’s booming digital economy.

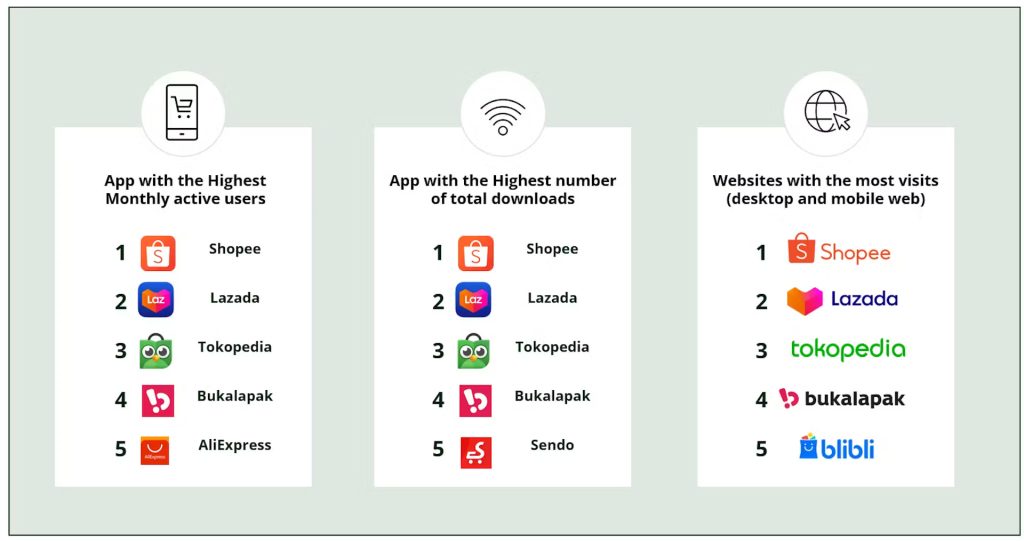

Sea started as a gaming company and managed to grow into SE Asia’s biggest eCommerce company, being number one in all SE Asia countries, ahead of Alibaba backed Lazada or Indonesian player Tokopedia (now called GoTo).

Through its three key divisions – Garena (digital entertainment & gaming), Shopee (ecommerce) and SeaMoney (digital finance) – the company has tapped into SE Asia’s burgeoning tech-savvy middle class.

Sea also boasts an incredibly robust management team, with a visionary founder and CEO, running the company since its creation.

Shopee’s, (Sea’s eCommerce platform) rapid growth has made it SE Asia’s largest eCommerce platform. Garena, meanwhile, is one of the leading online gaming platforms, sustaining revenue through a steady increase in user engagement. For investors, Sea offers a high-growth opportunity driven by a young consumer base and a rising demand for digital services in an underpenetrated and fast growing market such as Indonesia.

TOP 5 ECOMMERCE PLATFORMS IN SOUTHEAST ASIA IN 2023

Vietnam: A growing global footprint

Vietnam has also ascended as one of SE Asia’s most dynamic economies, becoming the manufacturing hub of the world, taking over from China. Leveraging its position as an alternative trading partner – challenging both China’s manufacturing dominance and India’s IT services exports – Vietnam has made significant strides. After experiencing a challenging period during the pandemic and subsequent export decline, Vietnam has rebounded strongly with record trade surpluses, further securing its reputation as an emerging export powerhouse. In fact, (after the correction of the past years, Vietnamese equities markets now have attractive valuations) these experiences may mean the valuations of some of the country’s most promising companies are particularly attractive.

Domestically, Vietnam’s economy is stabilising, with a resurgence in spending, credit growth and infrastructure development that collectively support its industrial ambitions. Mid-2024, Vietnam recorded the largest external surpluses in its history, at about 7% of GDP. And despite its $400 billion economy and population of 100 million8, Vietnam is absent from global indices, presenting a rare opportunity for active investors looking for growth.

In July 2024, the unexpected death of General Secretary Trong, led to the appointment of President and politburo member To Lam, taking on the acting role of the general secretary. While this new acting general secretary appears to be accumulating almost as much powers as his Chinese counterpart, the implied stability that it brings, combined with his pragmatism and pro-economic growth agenda point to an environment which is very conducive for companies to prosper.

INVESTMENT CASE : FPT CORPORATION

FPT Corporation (FPT) is a leader in Vietnam’s IT services industry, providing and deploying technology & telecommunications solutions to clients across Vietnam and the globe.

FPT has a presence in 30 countries and serves hundreds of companies across different sectors, and partnering with leading technology firms including GE, Airbus, Siemens, Microsoft, Amazon, and SAP.

FPT’s operations are divided into three segments: Technology (outsourced IT services, digital transformation consulting, AI, and Cloud solutions), Telecommunications (Broadband and Internet services in Vietnam) and Education (running training institutes across Vietnam to impart technology training to young people).

What makes FPT particularly unique is its exportation of IT services to Japan – a market that is exceptionally difficult to crack, and an exposure that’s scarce in the global market. With capabilities in digital transformation services, including cloud, artificial intelligence (AI) and big data, FPT is strategically positioned in a high-growth segment of the global IT market and a beneficiary of the AI revolution. It has cost advantage compared to its competitors in North America, Japan, and other developed markets, while FPT’s internal education programs continue to bolster Vietnam’s IT talent pool. By growing in its home market and expanding into key international ones, FPT is building a comprehensive service platform poised for long-term, compounding growth.

As an IT services exporter, FPT is not at risk from the US tariffs that concern so far only goods – services exports are not targeted – and its main export market is Japan and not the US.

Opportunities in high-growth sectors

When selecting stocks, Carmignac’s EM team looks for companies that offer compounding growth in underpenetrated sectors – two factors where Sea and FPT shine.

We are looking for companies with solid cash flow generation, self-financed growth, and success-hungry management teams, whittling our investment universe of 4000 securities to between 10 to 15 high-conviction selections across Asian large, mid, and small caps.

Carmignac’s strategy is to identify these opportunities early, including by keeping close relationships with private companies in anticipation of their going public to be able to invest during their IPOs.

Whether investing in large-cap companies via our flagship global EM Equity strategy, Carmignac Portfolio Emergents Fund, or in all-cap Emerging Asia companies via Carmignac Portfolio Asia Discovery Fund, our goal remains the same: to uncover compounders capable of sustaining long-term growth, reinvesting the proceeds of their success, while achieving a positive outcome on society or the environment, financing sectors or businesses where there are strong needs.

“We are looking for companies with solid cash flow generation, self-financed growth, and success-hungry management teams.”

WHY NOW? A SUCCESS STORY THAT IS SET TO CONTINUE

The ASEAN region is well on track to becoming the fourth-largest economy in the world by 20309. The region benefits from a young, fast-growing population. While many advanced economies are grappling with ageing workforces, SE Asia’s youthful demographic is a competitive edge, forming a tech-savvy middle class that is eager to spend.

Moreover, with global easing cycle continuing and inflation under control in Asia, local central banks can cut rates without jeopardizing their currencies. This is particularly the case for Indonesia and Philippines that had aggressively increased rates with the Federal Reserve tightening and now are cutting rates.

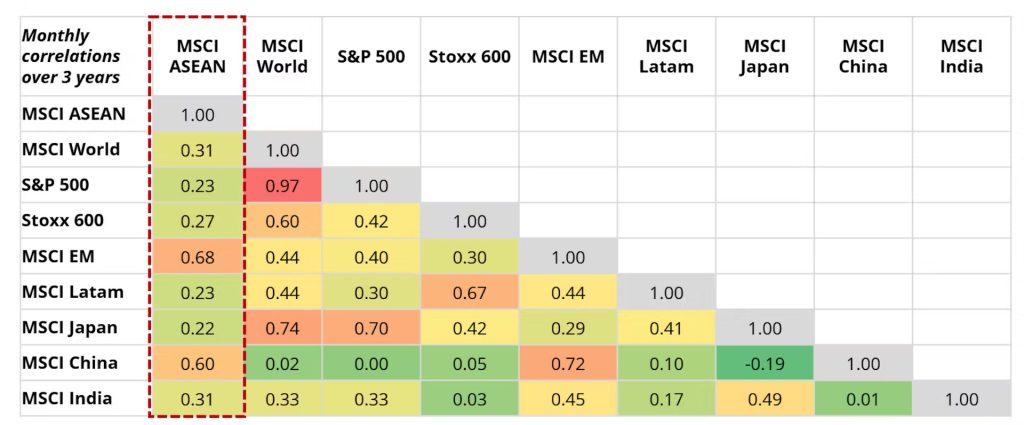

Investment wise, SE Asia markets play an important role in EM portfolios, acting as an effective diversification tool as the region shows low correlation with developed markets and also when compared with other Emerging regions, such as Latin America or India (see chart below).

They also provide a low beta exposure and compelling valuations in absolute and relative terms compared to Taiwan and other North Asian Tech companies.

Finally, in an environment marked by many concerns around the structural outlook for China, SE Asia emerges as an appealing alternative. Not only does it represent a China plus one alternative alongside India, but one with more compelling valuations given the stretched valuations in India following the solid performance of the past years.

MSCI ASEAN CORRELATIONS WITH DEVELOPED AND MAIN EM MARKETS OVER 3 YEARS (IN EUR)10

1 Sources: Bloomberg, MSCI, World Bank, 31/12/2024 2IMF:https://www.imf.org/external/datamapper/NGDP_RPCH@WEO/OEMDC/WEOWORLD/GUY/SUR/BRA/COL/ADVEC/AS5 3UNCTAD, ASEAN Investment reports 2024 4Multiples sources : https://www.scmp.com/tech/tech-trends/article/3206362/chinese-supplier-apple-samsung-screens-build-new-factories-vietnam

https://www.cnbc.com/2024/06/24/southeast-asia-is-the-top-choice-for-firms-diversifying-away-from-china.html

https://asia.nikkei.com/Business/Business-Spotlight/Malaysia-aims-for-chip-comeback-as-Intel-Infineon-and-more-pile-in

https://www.thestar.com.my/news/nation/2024/05/28/m039sia-to-become-global-semiconductor-rd-hub-attract-billions-in-investment-says-pm. https://thediplomat.com/2024/01/the-role-of-thailand-in-germanys-auto-manufacturing-future/

https://issuu.com/germanthaichamber/docs/update_q2-2024_pharmaceutical_industry_and_trends/s/46389208

https://foreignpolicy.com/2024/05/08/indonesia-electric-vehicle-green-transition-china-tariffs

5Sources: IMF : https://www.imf.org/external/datamapper/NGDP_RPCH@WEO/OEMDC/WEOWORLD/GUY/SUR/BRA/COL/ADVEC/AS5 6Source : Bloomberg 31/01/2025 7Source: TMO Group Asia, SeekingAlpha Research, Company data, 31/12/2024. 8Source: World Bank, Haver 31/12/2024. 9Source: IMF World Economic Outlook forecasts published on Jan 2025. 10Source: Bloomberg, 31/01/2025.