The Solvency II capital charge has become an important aspect in portfolio construction and asset allocation for insurance companies, next to the traditional trade-off between risk and return. For most assets, the capital charge is fixed and known upfront. However, for equities a capital charge with a variable component – the symmetric adjustment – is used. We discuss the current mechanism and possible changes in the Solvency II review. We also make a projection for the remainder of 2022 and find that the symmetric adjustment remains in slightly positive territory for the rest of 2022 in case of positive equity returns. In a negative equity scenario the symmetric adjustment is expected to become negative at the end of this year, however.

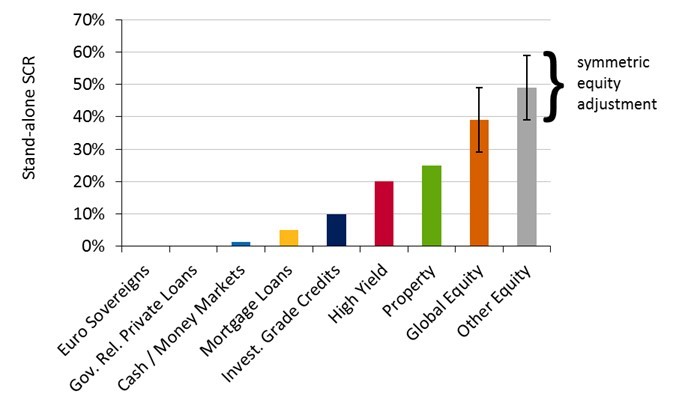

Solvency II is the regulatory framework for European insurance companies since January 1, 2016. The solvency capital requirement (SCR) is a crucial element under Solvency II. Because Solvency II is a risk-based framework, riskier assets are typically charged with a higher SCR than less risky assets. An example is given below for different asset classes.

We consider the stand-alone SCR here, so before diversification and tax effects. We also assume that interest rate and currency risk are hedged on the overall balance sheet. This figure shows that the SCR is zero for euro sovereign bonds (and euro government related bonds) and very low for cash or money market investments. The SCR increases for bonds with longer maturities or lower ratings.

For equities the SCR is not fixed but changes over time. The maximum deviation in SCR from the base value is +/-10%-points. In simple terms, this means that in a bull market the SCR for equities goes up, while the SCR goes down in a bear market. This mechanism – known as the symmetric equity adjustment – makes equities more capital expensive under Solvency II in an upward market and vice versa. The idea is to suppress pro-cyclical investment behavior of insurance companies in this way by making equities less attractive in bull markets and vice versa.

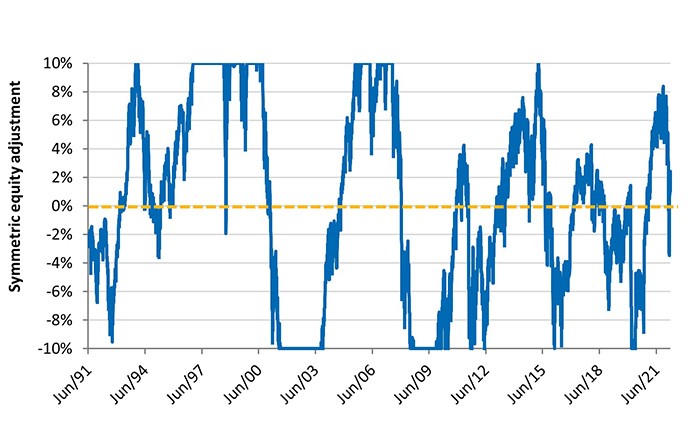

The following figure presents the official level of the symmetric adjustment as published by EIOPA.

Long-term evolution of the symmetric equity adjustment

This adjustment is very volatile, as is shown in the figure. It can go from one extreme point to another in only one year, as was the case in 2000-2001 and in 2007-2008. In order words, the amount of capital that an investor needs to set aside for equity investments can vary significantly from one year to the next. In relative terms, the capital charge for equity can vary by almost 70% for equity type I (50% for equity type II). In the full article we also show the effect of widening the corridor of +/-10% to +/-17%, which has been proposed in the current Solvency II review.

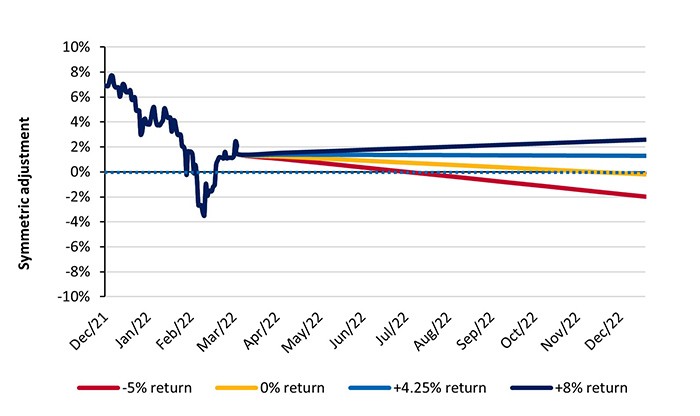

At the end of March 2022, the symmetric adjustment was equal to +1.4%. From this starting point, we have made a forecast of the symmetric adjustment for the remainder of 2022, see the figure below. The light blue line, with an annualized return of 4.25%, is based on the historical performance of the Euro Stoxx 50 index. Given the large uncertainties in the current equity markets we also show results for several other return assumptions, ranging between -5% and +8% per year.

Projection of the symmetric adjustment

We find that the symmetric adjustment remains in slightly positive territory for the rest of 2022 in case of positive equity returns. In a negative equity scenario the symmetric adjustment is, however, expected to become negative by the end of the year.

A summary of the findings:

- The capital charge for equities is currently slightly above its base value under Solvency II (+1.4%).

- The symmetric adjustment can, however, change rapidly, depending on the evolution of the underlying basket of equities.

- In our projection for the remainder of 2022 we see that the symmetric adjustment remains slightly positive, except when a negative equity scenario materializes in the rest of the year.

- The symmetric adjustment is also a discussion topic in the ongoing Solvency II review. The outcome of this review may be that the current corridor of +/-10% is widened to +/-17%. This would allow for larger swings of the symmetric adjustment, leading to a more volatile capital change for equities in extreme market situations.