At least headline Consumer Price Index (CPI) inflation actually fell this time… but again, the figures were an upside surprise.

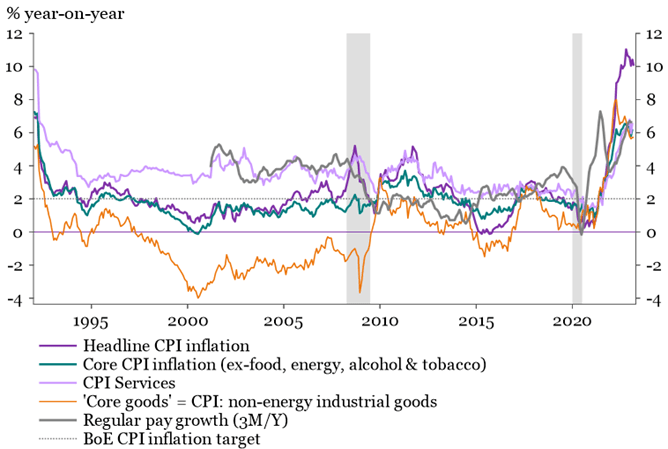

Headline CPI came in at 10.1% after 10.4% against consensus of 9.8% and core failed to fall at all, remaining at 6.2% (consensus: 6.0%).

Retail Price Index (RPI) inflation was stronger than expected too at 13.5% after 13.8% (consensus: 13.3%). After today’s inflation data and yesterday’s labour market data, it is hard to see the Bank of England (BoE) not hiking in May and I’d pencil in a higher probability of them hiking again after that – probably in August (all figures year-on-year).

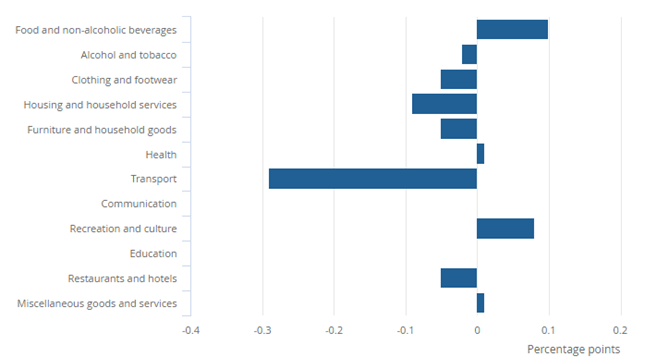

The biggest upward contributors to headline CPI inflation came from food and the recreation/culture components. The Office for National Statistics (ONS) estimates that food/non-alcoholic beverages inflation is now at its highest for 45 years. Worse, the upward pressure from recreation/culture didn’t seem to stem from the notoriously volatile computer games component – the ONS instead mention upward pressure from a ‘wide range’ of classes including “data processing equipment and cultural services”. The biggest downward drags came from diesel/petrol. However, more of the CPI components contributed negatively than positively to the move in year-on-year CPI this month, which was at least more encouraging than looking at core CPI in isolation (see first chart below).

As usual, these movements will reflect some temporary factors and some longer-term trends. The fall in energy price inflation from 49.0% to 40.5%, in particular, has a lot further to go in the UK, with powerful negative base effects likely to pull headline inflation down further this year. What I’d call ‘core goods’ inflation was disappointingly static though (non-energy industrial goods) at 5.7%, sticking around that level for the fourth consecutive month. I’d have expected lower commodity prices and improved supply chains to have had a bit more downward impact. It is also hard not to worry about how strong underlying/domestically driven inflation looks in the UK.

Domestically driven inflation still looks strong. Services inflation was static at 6.6%. More worrying, perhaps, is that when I scan down the list of services subsectors, not many showed decent falls in year-on-year inflation (though the heavily weighted catering services and package holiday components were notable exceptions). CPI figures by import show that the CPI contribution from the least import-intensive, or most ‘domestic’, bits of inflation remains relatively high. Pay growth was stronger than expected in yesterday’s labour market data.

Cost of living crisis: Inflation in essentials remains strong. In particular, energy and food price inflation remains high. Food inflation was painfully high at 19.6% in March after 18.3%. Energy inflation continued to drift lower but remains high.

BoE likely to hike again: In the February Monetary Policy Report, the staff forecast for this March headline inflation figure was 9.2%, so today’s data marked another significant overshoot to those forecasts. The Monetary Policy Committee have clearly indicated that if inflation pressures prove more persistent, then they would have to hike further…

Contributions to change in the annual CPI inflation rate, UK, between February and March 2023.

UK: Headline, Core, Core Goods & Services Inflation

This is a financial promotion and is not investment advice. Past performance is not a guide to future performance. The value of investments and any income from them may go down as well as up and is not guaranteed. Investors may not get back the amount invested. Portfolio characteristics and holdings are subject to change without notice. The views expressed are those of the author at the date of publication unless otherwise indicated, which are subject to change, and is not investment advice.