An update on the UK inflation market over the last three months.

Introduction

Inflation has continued its strong upward march since our last update, fuelled on by the Russian invasion of Ukraine and China’s renewed Covid-related restrictions. Amidst this backdrop, a cost-of-living crisis is gradually unfolding in the UK and expectations of a growth slowdown becoming more likely. Naturally, an increasing focus is being placed on the Bank of England’s (BoE) reaction function to the inflation/growth trade-off. Looking ahead there are still plenty of strong inflationary pressures in the pipeline, but our view is that the medium to longer-term inflation outlook may be more balanced, to the extent of a possible inflation undershoot if growth slows because of permanently higher prices and rate hikes.

We also provide our projections for inflation-linked issuance for fiscal year 2022/23 to reflect the remit update at the end of April and discuss our outlook for inflation-linked assets.

The inflation/growth trade-off

Whilst the BoE’s primary mandate is to “set monetary policy to achieve the Government’s target of keeping inflation at 2%”, it also has a secondary remit to “support the Government’s other economic aims for growth and employment”. As we emerged from the Covid pandemic, economic recovery has been robust thanks to significant government intervention and the dominance of newer, less-threatening virus variants that weighed less on activity than expected. This had a hand in sustaining headline inflation at record highs and lifting the growth outlook for the UK.

Today we are in a slightly different place as the BoE warned of recession at the May Monetary Policy Committee (MPC) meeting if the market implied path of rate hikes were realised. Though inflation remains stubbornly high, signs of a growth slowdown have started to show in the form of declining consumer sentiment and retail sales numbers, thus shifting the market’s focus toward the BoE’s possible reaction function to the inflation/growth trade-off.

Elevated geopolitical tensions

In the medium-term, however, these exogenous shocks could become deflationary. The inevitable squeeze on consumer incomes could lead to demand destruction particularly on discretionary spending. It is not a given that consumers will entirely smooth their consumption patterns by reducing their accumulated savings, not least because aggregate savings are unevenly distributed across income deciles. The MPC recognises these risks and has clarified that it remains sensitive to domestic growth developments, particularly if material squeezes in real disposable incomes are likely to drag on output in the near term and domestically generated inflation in the medium term. For now, in the face of these sharp price increases, the BoE’s preferred policy stance is to tighten monetary policy and front load this, at the expense of lower growth.

Rising domestic price pressures

Supply and demand dynamics lean toward stronger pay awards in the coming months and an increase in employee bargaining power. This is because labour supply remains below its pre-pandemic level, whilst the “quits” rate1 is now at the highest level for nearly a decade. Hence, it is a real worry for the BoE if wage settlements begin to incorporate higher inflation into new bargaining agreements.

It is worth noting that although wage growth has been picking up, real wages have declined significantly, suggesting corporates are successfully passing on wage costs through higher prices and therefore, we can expect services price inflation to pick up going forward. As an aside, higher wages are not necessarily bad, particularly if they are associated with higher labour productivity. A sizeable gain in labour productivity should offset some of the headwinds from higher wages and support corporate margins through 2022.

Over the coming months we will see the peak of the inflation spike, but beyond this inflection point, inflation will likely come down mechanistically due to base effects, particularly as energy price rises will fall out of the annual inflation rate from April 2023. With the effects of tighter monetary policy, diminishing fiscal support and the cost-of-living squeeze also to play out, the probability of a wage-price spiral is low in our view but is one to watch.

The BoE’s policy dilemma

The BoE is in a difficult situation where it has a price stability mandate and hence cannot purely focus on growth. In the event of a large inflationary shock, monetary policy will usually need to tighten faster, creating spare capacity and a larger negative output gap to keep (medium-term) inflation at bay. There are still plenty of strong inflationary pressures in the pipeline, but further ahead our view is that the inflation outlook may be more balanced, with the added possibility of an inflation undershoot over the longer term if the economy slows consequent of price rises and rate hikes.

Inflation expectations have risen so far beyond target that the option value of waiting is too great now. Consequently, central bankers are under pressure to take action, with a preference for being aggressive now – raising rates into restrictive territory – then reversing course later if needed. By doing so, the BoE can appear credible with its inflation mandate and in turn, keep inflation expectations anchored to target.

The outlook for inflation-linked assets

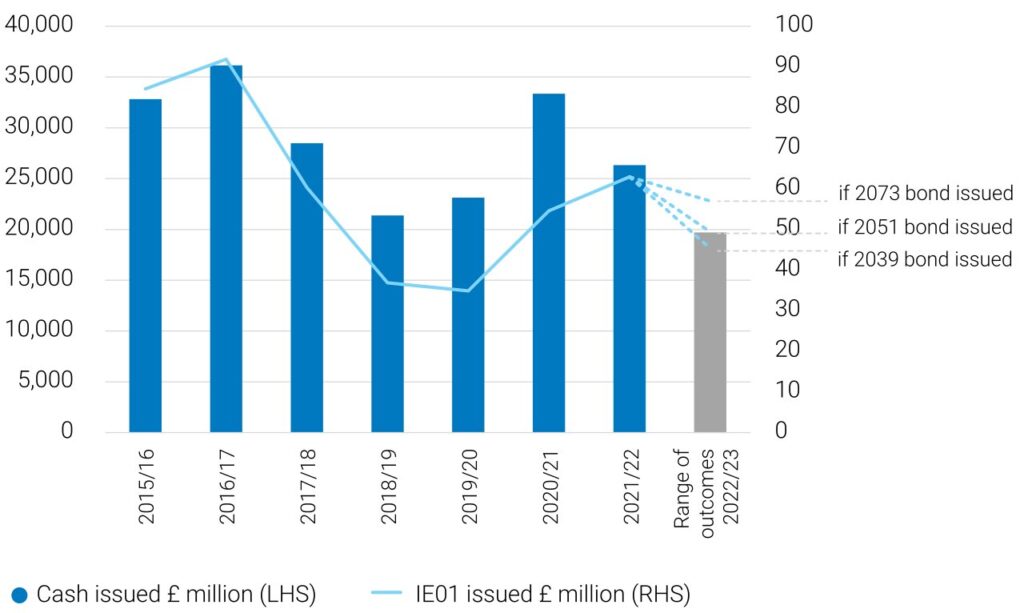

Following the announcement of the refreshed remit for fiscal year 2022/23 at the end of April, we provide our inflation-linked issuance projections for the period. The new remit saw index-linked gilts fall to an all-time low in terms of “cash issued” but exceeded expectations in “inflation risk” terms. This was kicked off with the re-opening of the 2073 inflation-linked gilt via syndication – the first key duration event of the year, adding c. £23m IE01 to the market.

We can expect one more inflation-linked issue via syndication this fiscal year. The range of possible issuance scenarios for three prospective gilts – maturing in 2039, 2051 and 2073 – are marked out in Figure 1. If the second syndication were to be another 2073, this would add significant inflation risk to the market (only c. 10% down from last fiscal year), despite the marked decrease in cash issued (c. 25% reduction from last fiscal year).

Figure 1: Inflation-linked issuance2

Source: BMO Global Asset Management, DMO

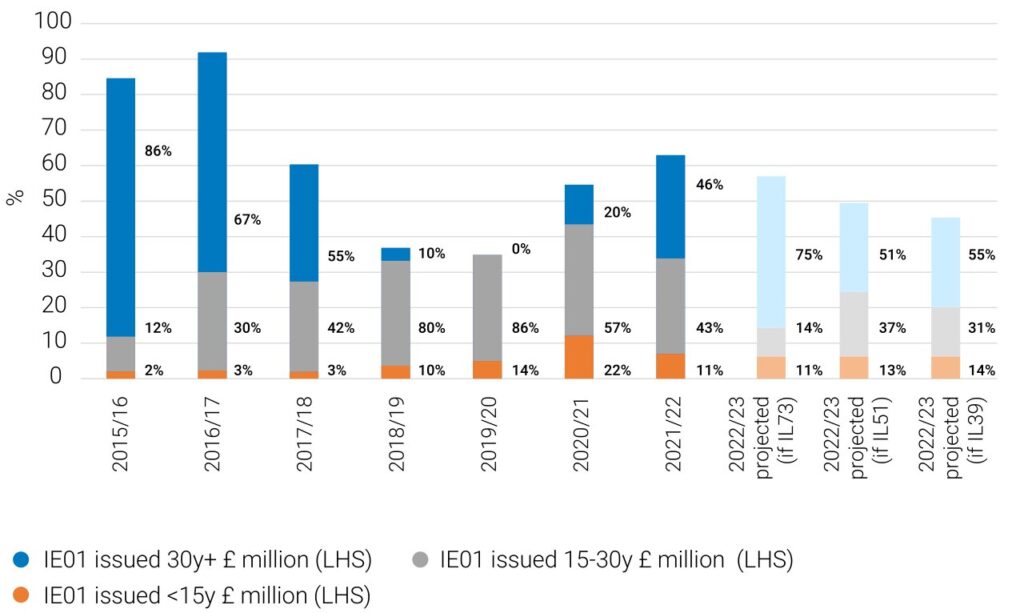

As we have previously highlighted, the DMO appears to prefer longer-dated inflation-linked issues. Figure 2 shows that regardless of which bond is selected as the second syndicated issue this fiscal year, there seems to be a reversion to longer-dated inflation-linked issues making up a larger proportion of total IE01 issued – a trend which characterised periods prior to fiscal year 2018/19.

Figure 2: Distribution of inflation exposure issued, by maturity buckets

Source: BMO Global Asset Management, DMO

Taking the 2073 syndication as an example – although there was strong demand, each day post syndication ultra-long inflation-linked gilts cheapened, cheapening by 0.4% between 27 April and 9 May where real yields peaked at a level not seen since March 2020’s “flight to safety”. The market repriced quickly then, due to the accommodative market conditions. In contrast, in the current rates rising environment, if inflation-linked supply were to be skewed longer, the ultra-long sector could underperform.

Never a dull moment in the inflation market

The trend of inflation-linked gilt selling over the past 6 to 8 months and their resulting weak valuations relative to swaps may also be explained by talk amongst pension scheme clients who voiced concerns that their RPI hedges were over-hedging their LPI-linked liabilities that now more resemble fixed liabilities.

Over the same period, volatility has plagued the inflation market but most notably for swaps, perhaps driven by a one-sided market where there have generally been more sellers than buyers of RPI. Compared to gilt inflation which is still driven by two-way flows in the market, swap liquidity has been persistently poor as banks have become more risk-averse (with some having taken on large positions that turned into painful trades amidst the heightened volatility). Consequently, transaction costs to trade RPI swaps have risen as banks try to reflect this volatility.

A brief update on CPI issuance

Turning to the CPI market, apart from a few quotes periodically being shown at 10-year and below in the interdealer market, there has not been too much activity of note. The fourth round of Contracts for Difference (CfD) auctions announced in December 2021 which we mentioned in our previous update were signed last month. This may prompt the follow-up hedging of some CPI exposure by contract winners, but it is unlikely this will come to market immediately, unless it is hedged in forward space. Issuance of this nature has tended to be swept up by larger insurers rather than pension schemes, whose interest in CPI-linked assets appear to have waned following the decision to align RPI to CPIH from 2030.

Final words

It is fair to say that there is general market consensus over near-term inflationary pressures persisting up until April 2023. The real question is – where will inflation land beyond that inflection point? Could we see inflation undershoot the BoE’s target over the medium to longer term as the impact of higher prices forces demand down; or might we be faced with higher inflation, albeit at a level lower than the spikes we have seen over 2022?

Our view is that inflation will come down mechanistically, not only as base effects fall out of inflation figures, but also due to the implications of tighter monetary policy, diminishing fiscal support and the cost-of-living squeeze, which will gradually kick in. Some have voiced concerns over the threat of stagflation – the combination of high inflation and stagnant growth – which might not be unfounded in the near term, as the MPC’s latest projection in May was for inflation to peak at over 10% by the fourth quarter of 2022. Considering this, again we have seen the market revise its terminal rate forecasts around 1% higher than in February, such that these are now exceed the BoE’s expectation of over 2.5% in 2023. Over the medium term, however, the MPC projects inflation to be back at target by mid-2024 as external and domestic pressures subside, which could signal that the BoE might take a more dovish stance at the next meetings to avoid sending the economy into recession.

- Cash raised based on assumption that auctions have average size ranging between £700 million to £1,400 million; and planned £8 billion to be raised over two syndications.

- Auctions beyond June 2022 have also been extrapolated based on the auctions already confirmed for April to June.

- For the two syndications, a 2073 was selected for April but the other scheduled for later in the year is still unconfirmed.