Headline December UK consumer price inflation (CPI) came in at 4.0%Y after 3.9%Y last month, compared to consensus expectations of a fall to 3.8%Y.

Core CPI stayed at 5.1%Y (consensus: 4.9%Y) and CPI services (which the Bank of England’s Monetary Policy Committee (MPC) have been putting focus on) rose to 6.4%Y after 6.3%Y. Retail Price Inflation (RPI) surprised a tenth on the upside at 5.2%Y after 5.3%Y.

Just as for the November data, when the downside surprise in inflation wasn’t as good as it looks, today’s upside surprise for the December data isn’t as bad as it looks – at least in terms of what it implies for underlying inflation trends.

November’s CPI figures surprised on the downside, but were driven by a lot of things that were hard to pin on underlying domestic inflation pressure, with volatile components like computer games, live music events and air fares partly responsible.

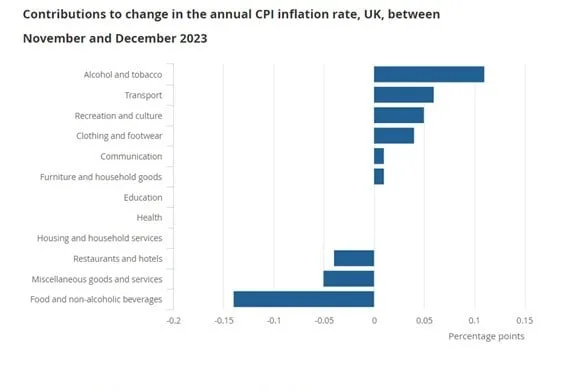

This time around, the biggest positive contributions to the increase in UK CPI in December (see chart 1) were alcohol and tobacco, transport, and the recreation and culture component. The alcohol and tobacco move was driven by higher tobacco duty after the government’s Autumn Statement. The move in the recreation/culture component looks to have been driven by a number of things but the Office for National Statistics again warns that short-term movements in some of the categories “should be interpreted with a degree of caution as the movements depend upon the composition of best seller charts.” As for transport, the move was mainly the result of air fares (a downside driver the previous month and often a volatile component).

Chart 1: Alcohol and tobacco leads the upward contributions to the change in annual CPI rate.

Source: Consumer price inflation from the Office for National Statistics.

Looking at bigger picture indicators of underlying domestic inflationary pressure, the fact that services inflation rose is clearly not great news. This indicator of inflation remains strong and likely too strong for the Bank of England to feel confident of sustainably hitting a 2% inflation target. But, looking at the services detail, there was quite a mix with different sub-categories seeing higher and lower inflation and no clear overall pattern.

December’s upside inflation surprise wasn’t as bad as it looks, but I still think that it will probably take a while – and quite a bit more evidence – for the MPC to feel convinced that inflation is going to sustainably return to 2% inflation. For now, I still have the first MPC rate cuts in my forecasts pencilled in for the second half of this year rather than the first half.

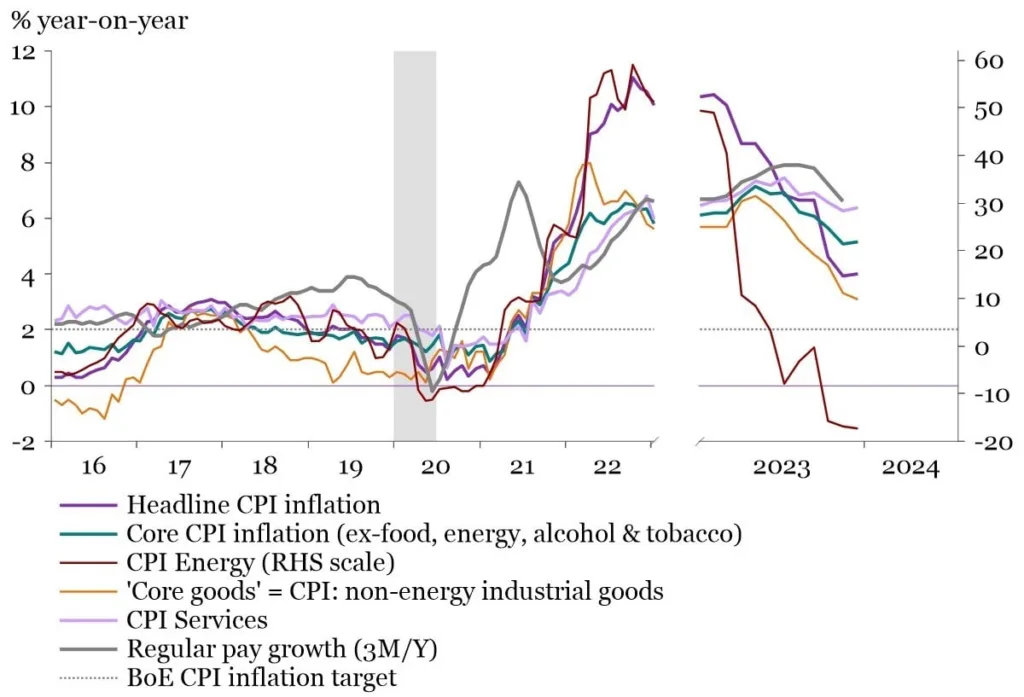

Chart 2: UK inflation: headline, core, core goods & services inflation

Source: LSEG Datastream as at 15/12/2023.

This is a financial promotion and is not investment advice. Past performance is not a guide to future performance. The value of investments and any income from them may go down as well as up and is not guaranteed. Investors may not get back the amount invested. Portfolio characteristics and holdings are subject to change without notice. The views expressed are those of the author at the date of publication unless otherwise indicated, which are subject to change, and is not investment advice.