There’s an ongoing debate between Federal Reserve Governor Chris Waller and Larry Summers that, in my view, usefully frames the USD25 trillion question over whether inflation can be tamed with a ‘soft’ or ‘hard landing’ for the US economy.

It highlights the crucial role of the labour market and suggests investors should focus on the evolution of the vacancy rate (a reduction in job openings is good news for the ‘soft landing’ camp), reports of layoffs (consistent with the ‘hard landing’ scenario) and the evolution of wage growth (the litmus test of how tight the labour market is and underlying inflation pressures).

If, as Summers et al argue, the natural rate of unemployment (the rate of unemployment consistent with stable inflation) has risen, then upward wage pressure will persist, and core inflation will remain above target until there is a substantial rise in unemployment and recession.

But if Waller is right, wage pressure and inflation can be tamed by reducing labour demand through fewer job openings (vacancies), rather than a meaningful rise in unemployment, meaning the Fed can be successful in engineering a ‘soft landing’.

Ideally, labour supply would increase, allowing employment to rise while curtailing wage inflation. But the labour force participation rate appears unlikely to meaningfully increase, hence the focus on reducing labour demand.

In my view, the Waller analysis implies that the Fed can ‘pivot’ once the vacancy rate has fallen further and wage growth decelerates that would underpin a sustained fall in core inflation towards the Fed’s 2% target. But if Summers et al are right that the natural rate of unemployment has increased and aggregate demand is well above the supply capacity of the economy, the Fed will be forced to keep hiking rates until the unemployment rate reaches at least 5% and implies a higher terminal rate for the Fed funds than under the ‘soft landing’ scenario.

Let’s explore in more detail the debate between Waller and Summers.

At the heart of the ‘soft’ versus ‘hard landing’ debate for the US economy as the Fed tightens monetary policy is whether excess labour demand (the excess of vacancies over the unemployed) can be reduced without a meaningful rise in the unemployment rate. Historically, an increase in the 3-month moving average unemployment rate by 0.5% relative to its prior 12-month low signals recession – the Sahm Rule.

Bringing the labour market back into balance so it is not extremely tight, and tempering wage growth requires reducing labour demand. But a ‘soft landing’ requires most of the reduction in labour demand to come from fewer vacancies, rather than an increase in layoffs and unemployment.

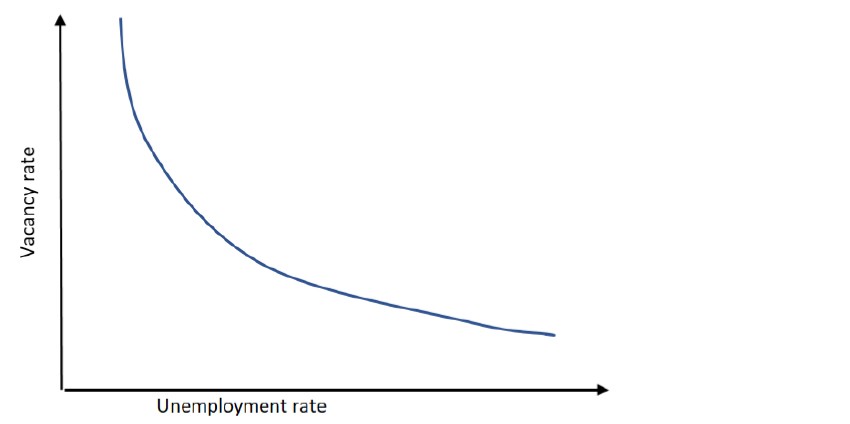

The relationship between the vacancy rate (job openings/labour force) and the unemployment rate can be expressed in terms of the ‘Beverage curve’.

Chart 1: Beverage curve

Moving from left to right along the Beverage curve, the vacancy rate declines and the unemployment rate rises. The position, and crucially steepness, of the underlying Beverage curve (relationship between vacancies and unemployment) that the labour market current sits is not directly observable as it depends on estimates of the efficiency of the labour market in matching unemployed to vacancies.

Fed Governor Christopher Waller claims that a reduction in labour demand and the vacancy rate can be achieved without a meaningful rise in unemployment because the slope of the actual Beverage curve is currently steep1.

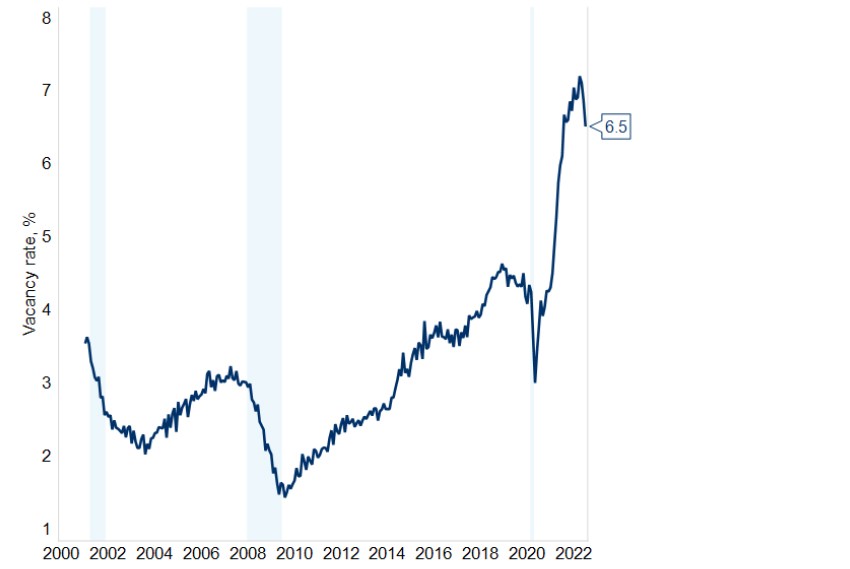

Waller argues that the current vacancy rate is exceptionally high (generating wage pressure but not more employment), which is consistent with very strong labour demand, and that the labour market is positioned on the steep segment of the Beverage curve. Reducing the vacancy rate from its current level to 4.6% – its pre-pandemic rate – would reduce wage growth and still be consistent with strong labour demand, a low rate of layoffs and only a modest increase in unemployment.

According to Waller’s estimates, reducing the vacancy rate (see chart 2) from around 7% to 4.6% (its pre-pandemic level) would only be associated with a one percentage point increase in the unemployment rate2.

Chart 2: Vacancy rate (job opening/labour force)

Larry Summers, Oliver Blanchard and Alex Domash have contested Waller’s analysis, concluding that the post-pandemic labour market is less efficient (less good at matching unemployed to vacancies) in part due to increased ‘reallocation’ post-pandemic (shifts in jobs by skill and place due to work-from-home etc)3.

Summers et al conclude that the ‘natural’ rate of unemployment (rate of unemployment consistent with stable inflation) has increased to around 5% from 4% pre-pandemic (the Fed’s estimate of the natural rate). This implies it will have to rise above 5% for inflation to be sustainably reduced from above target.

They also show that historically, a sizeable reduction in the vacancy rate is invariably associated with a meaningful rise in unemployment and argue that for this not to hold true in the current cycle, there would have to be meaningful improvement in labour market efficiency (the rate that unemployed workers are matched to vacancies) that would shift the Beverage curve lower.

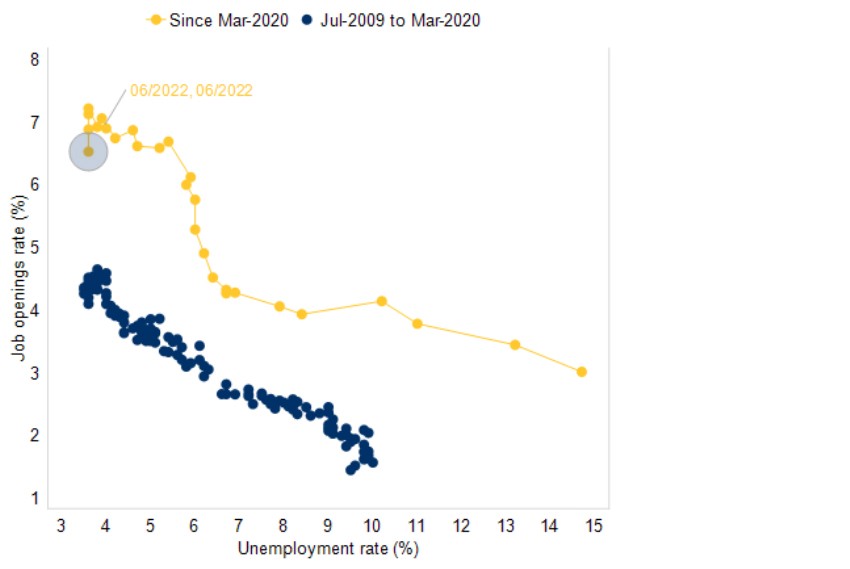

The debate between Waller and Summers can be partly summarised in chart 3, where the gold dots show the observed relationship between the vacancy and unemployment rates before and post-pandemic. It suggests that Summers is right that the labour market is less efficient than it was pre-pandemic (i.e. the ratio between vacancies and unemployed has increased) consistent with a higher natural rate of unemployment.

But it also fits with Waller’s argument that the pandemic and its aftermath are exceptional, the labour market is on the steep point of the Beverage curve and that the vacancy rate can fall meaningfully from its current exceptionally high level without a big increase in unemployment (and will show up by the gold line in chart 3 shifting down towards the blue dots).

Chart 3: Vacancy & unemployment rates pre and post-pandemic

The latest job openings data (JOLTS report) for June showed a larger-than-expected decline in vacancies while the unemployment rate remained unchanged over the month, consistent with the Fed/Waller case for a soft landing. But it’s just one data point, and the relationship between labour demand, vacancies, layoffs and unemployment is dynamic with time lags. The July Employment report showed an outsized gain in jobs but a further drop in labour supply while the unemployment rate fell to a post-pandemic low of 3.5% and wage growth accelerated. Both sides of the debate acknowledge that the US labour market is indeed ‘extremely tight’.

The debate between Waller and Summers frames the USD25 trillion question over whether inflation can be tamed with a ‘soft’ or ‘hard’ landing in the US economy. It highlights the crucial role of the labour market and suggests investors should focus on the evolution of the vacancy rate (the 2 August JOLTS report showing a reduction in job openings is good news for the ‘soft landing’ camp), the pace of layoffs and the path of wage growth.

If Summers et al are right, wage growth should remain elevated and even accelerate (hence tracking the various wage measures is important, including of course average hourly earnings reported along with nonfarm payrolls). But if Waller is right, vacancies will continue to decline as Fed policy tightening reduces labour demand and wage growth will moderate with only a modest pick-up in the rate of unemployment – the hoped for ‘soft landing’ scenario.

It is difficult to map this debate into alternative paths for Fed funds, not least because the sensitivity of the economy to changes in interest rates is uncertain. For instance, higher levels of debt may mean that even modest increases in interest rates by historical standards may be sufficient to reduce aggregate demand.

With this qualification in mind, in my view, the soft landing scenario implies the Fed can pivot once the vacancy rate has fallen significantly and wage growth is decelerating, even with inflation above target. For Summers et al, the economy is operating well above potential and to sustainably reduce domestic wage and price inflation the Fed will be forced to keep hiking rates until the unemployment rate reached at least 5% (currently 3.5%), implying a higher terminal rate than under the ‘soft landing’.

1 Responding to High Inflation, with Some Thoughts on a Soft Landing

2 What does the Beveridge curve tell us about the likelihood of a soft landing?

3 Bad News for the Fed from the Beveridge Space, PIIE, July 2020