Our recent observations of corporate behaviour have seen us become cautious in our general outlook for markets. There are some pockets of the market where aggressive corporate investment is worryingly high but share valuations are still exorbitant. In these areas, we are seeing the most expensive valuations we have come across in the 30-year history of the data we use. However, we think this bodes well for the prospects for the short side of our process and have significantly raised our short exposure.

Corporate aggression, our proxy for company manager optimism, is one of the main market indicators we use. We see corporate optimism as a contrarian market indicator: when company managers become more aggressive in their expenditure, we are more wary about the outlook for equities. The reason we are cautious regarding aggressive corporate expenditure is that it often signals that executives in board rooms are increasingly making optimistic forecasts which they are prepared to back with significant investment. When in due course the over-optimism is revealed and growth disappoints, the situation is exacerbated by the misplaced investment that has occurred.

We’ve therefore designed our corporate aggression measure to highlight when managers are becoming particularly aggressive with their investment – it is a signal across the market that company managers are becoming too optimistic about the outlook for growth and that they are backing these bold forecasts with substantial investments in operating assets such as property, equipment and stock to capture the growth opportunity they foresee.

These aggressive investments carry substantial forecast risk. This can be particularly dangerous where borrowing has been used to finance capital expenditures. If these projects don’t yield the anticipated boost to operating cashflow and profits, or worse, leads to more cash haemorrhage, the impact on share price valuations can be brutal. The higher the share valuation is, the greater this danger.

Immediately prior to the Covid-19 crisis, we held a constructive view of equity markets: although markets had become more expensive after strong returns in late 2019, valuations didn’t look worrying and companies in Europe were not showing any signs of over-aggressive levels of investment.

As the pandemic took hold, the level of corporate aggression understandably dropped given the significant pressure on corporate earnings. This sign of more conservative corporate management provided a positive outlook for equity markets at the time.

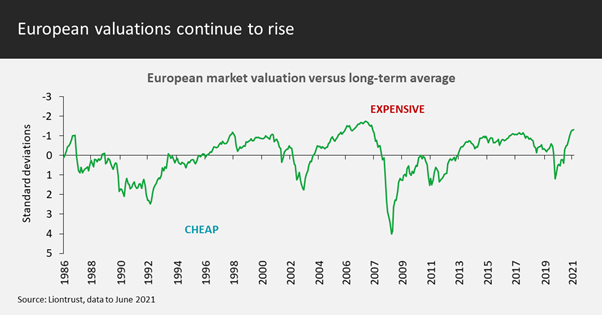

As markets subsequently rebounded strongly, they moved into expensive valuation territory. This alone isn’t usually enough to halt an uptrend – we know both empirically and anecdotally that market rallies can prove immune to valuation concerns for a surprisingly long time. However, when expensive valuations are combined with high corporate aggression, this is usually a sign that we are a lot closer to the end of a bull period.

This is the situation we face now. Valuations are expensive in Europe as the chart above shows. Meanwhile, our proprietary measure of corporate aggression now sits just over one standard deviation above average. At one standard deviation we sit up and take notice – closely monitoring the indicator. We know that previous market crises have occurred once the indicator begins to approach two standard deviations and usually the journey between one and two standard deviations on the indicator can be rapid. The situation today is therefore a concern – markets are very expensive relative to history and corporate aggression is climbing.

Due to climbing corporate aggression, we expect significant opportunities to unfold for the Liontrust GF European Strategic Equity Fund’s short book over the next 12 months. Specifically, there are pockets of the market where valuation dislocations are extreme, with some stocks scoring poorly against our cash flow criteria but still trading at exorbitant share price valuations.

These are mostly found among stocks we classify under our ‘secondary score’ system as possessing Recovering Value or Growth characteristic. We know that when stocks scoring poorly on our Recovering Value or Growth scores are also extremely expensive relative to their history, it has always been a leading indicator of very strong short side returns.

Today the situation relative to history is quite unprecedented. Stocks scoring poorly on our Recovering Value and Growth scores have never been as expensive as they are today for the entire 30 year history we have of this data. Currently the lion’s share of our short book is made up of stocks fitting this description.

We have also increased the size of our short position in the Fund to around 78%, from an average of closer to 50% over the prior 12 months. If corporate aggression continues to climb, we expect to see the net exposure of the Fund to decrease through a combination of an increase in the size of the short book and a reduction in the long book. If the indicator gets as high as two standard deviations, we expect the Fund will be close to market neutral.

Key Risks

Past performance is not a guide to future performance. Do remember that the value of an investment and the income generated from them can fall as well as rise and is not guaranteed, therefore, you may not get back the amount originally invested and potentially risk total loss of capital. Investment in Funds managed by the Cashflow Solution team involves foreign currencies and may be subject to fluctuations in value due to movements in exchange rates. The Liontrust European Growth Fund holds a concentrated portfolio of stocks, if the price of one of these stocks should move significantly, this may have a notable effect on the value of the respective portfolio. The Liontrust Global Income Fund’s expenses are charged to capital. This has the effect of increasing dividends while constraining capital appreciation.

Disclaimer

The information and opinions provided should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Always research your own investments and (if you are not a professional or a financial adviser) consult suitability with a regulated financial adviser before investing.