Adam Darling says a global recession looks probable and may bring opportunities in high yield bonds for active investors.

Risk markets bounced early in the year as investors bought into the view that central banks will somehow manage to perfectly land the plane and avoid undue turbulence in the economy.

This view holds that the US Federal Reserve (Fed) will pivot from hawkish to dovish, avoiding recession, and that we can return to bull market investing – and forget about the difficulties of 2022.

That is very firmly not our view. The cumulative tightening from the Fed, Bank of England and European Central Bank and the extent of interest rate rises, the amount of debt in the system that has to be refinanced and the stress that the global consumer is under already make recession highly probable. As the monetary largesse of the last decade fades into history, we anticipate rising corporate distress and dispersion in the corporate bond market.

Avoid distressed companies

We recognise this will be a difficult environment for many companies. However, it’s also a great market for active high yield bond investors. Investor fear and market volatility brings increased risk premiums, and as active managers with a well-resourced and experienced credit team, we will be looking to harvest that attractive premium while staying away from the distressed companies which will find market conditions increasingly challenging.

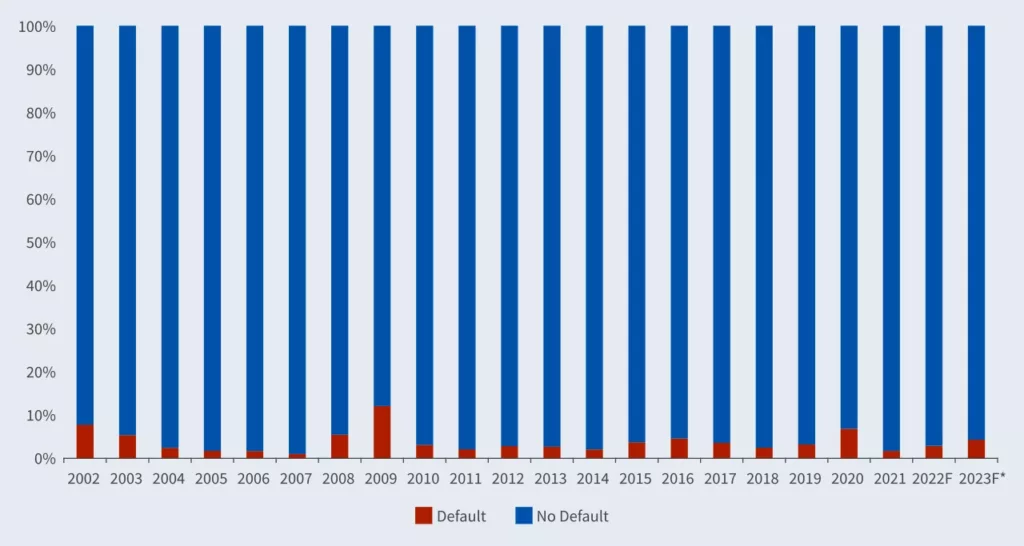

There is sometimes a perception that high yield bonds are “risky” – statistically they are riskier and therefore pay higher yields than investment grade credit. But our view is that a lot of the risk coming from high yield bonds can be mitigated if the asset class is approached in a sensible way. Default rates typically average less than 4% a year through the economic cycle, increasing in recessions and declining in recoveries. That means an active manager can choose from a large pool of investable companies. You are managing risk through the business cycle and the valuation cycle. In my view, the excellent total return and Sharpe ratio (a measure of risk-adjusted return) characteristics of the asset class over time highlight that as an investor, you are more than adequately compensated for managing the risks.

No surprises

Typically, unless there is a fraud or “black swan’’ event, defaults are rarely a surprise. You can see the businesses that are over levered and over extended and living on very cheap money. These are the companies that go bust.

Our investment process involves being active, pragmatic and risk aware. Active means moving the portfolio to take advantage of where you think the market is going. Pragmatic means reviewing market conditions, sentiment and valuations to assess when you should be aggressive or defensive through the cycle. You shouldn’t be dogmatic about how you invest. Then it is very important to be risk aware. In bonds, it’s about mitigating the downside risks. If you avoid the bonds that run in to difficulties, then you can make very good risk-adjusted returns.

High yield default rate: lower than feared?

Even in default, credit selection matters: bond recoveries can range from 0 – 100%

Historical defaults as proportion of global high yield market and Moody’s ’22 and ’23 forecasts

Generating income

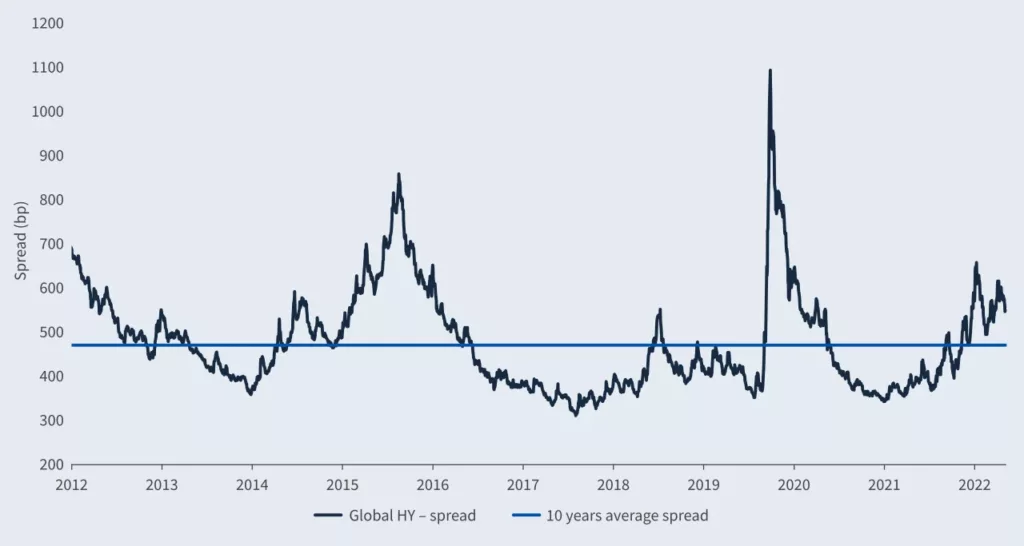

Last year was a horrible year for fixed income because of the combination of interest rates rising and credit spreads widening. However, the bear market has repriced high yield bonds from being very expensive to better value. Yields are very high relative to history so investors are being compensated for future volatility, with the benchmark yield to maturity around 8% at the time of writing. The combination of credit spreads and interest rates means the bond yields are now generating good income, in our opinion.

With broad market yields looking attractive, the key task for us this year will be avoiding those companies which will run into difficulties in a tougher economic environment. We currently have a preference to be overweight higher quality issuers after a very significant risk rally into the new year which has left some lower quality sectors of the market looking expensive. We retain a preference for Europe over the US – Europe was very cheap last year because of fears around the Russia-Ukraine war and the energy crisis. We did a lot of work around individual companies and found several compelling investment opportunities. Although European bonds have since rallied very strongly, we still find that in many cases they offer more attractive risk/return relative than the US (where credit spreads – in our view – are broadly too expensive going into a potential recession).

Global High Yield Market

Valuations in perspective

Global High Yield Market: historical yield, last 10 years

Squeezed consumer

We think emerging market exposure is selectively interesting, in an environment where investor sentiment has become overly bearish, developed market central banks may be less hawkish and the dollar weakens. There may also be opportunities in new issuance. Companies coming to market in a more challenging environment have to give bond investors better treatment, including better covenants and attractive coupons.

We would avoid consumer discretionary companies because we see consumers as probably the weakest part of the economy after absorbing enormous cost of living increases affecting housing, energy and credit access. Likewise, some cyclical industries such as chemicals, after a robust post-Covid period, may struggle as global growth and manufacturing weakens.

We believe that the damage from higher interest rates is only beginning. We will start to see in 2023 the real-world impacts of monetary policy tightening. At some point we will get through the recession and get a recovery. Central banks will be easing and governments will be stimulating. We are not there yet. We need to be careful in this interim period where asset prices have a lot of hope baked in but where there is still a lot of bad news to come. For investors it will be important to be selective and take advantage of the better opportunities where you’re getting compensated properly. We are very bullish about the capacity of active high yield fund managers to generate alpha in this environment.

Investment risks

When investing in developing geographical areas and there is a greater risk of volatility due to political and economic change; fees and expenses tend to be higher than in western markets. These markets are typically less liquid, with trading and settlement systems that are generally less reliable than in developed markets, which may result in large price movements or losses to the investment.

While high yield bonds may offer a higher income, the interest paid on them and their capital value is at greater risk of not being repaid, particularly during periods of changing market conditions.