Despite living in a period of elevated inflation for the past 18 months, gold has failed to reach the highs of summer 2020. In fact, gold has largely been falling since March 2022, when it briefly rose above $2000/oz1. A strong US Dollar and a bond sell-off have put gold under pressure. The US Dollar basket (DXY) reached a 20-year high in July 2022, and we have not witnessed such a sharp appreciation in the US Dollar since 2015. The Euro briefly fell below parity to the US Dollar in July 20222 – a spectacle not witnessed since the early days of the currency3 when the US came under pressure from a ballooning deficit.

Gold holding up well, all things considered

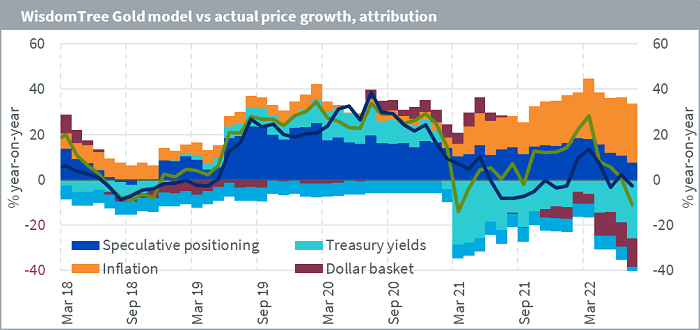

Factoring in these pressures, gold has not fared that badly. In fact, our internal forecast model4, indicates that gold should have fallen in the order of 10.8% y-o-y in July 2022, whereas we only saw a 2.7% y-o-y fall in the month. Despite subdued investor sentiment toward the metal of late, recession fears are likely to put gold increasingly into focus. Gold has historically been a strong performer in economic downturns. As hawkish central banks clip the wings of global economic growth, we expect interest in gold to be driven higher.

Source: Bloomberg, WisdomTree data available as July 2022. Speculative positioning as reported by Commodity Futures Trading Commission, Treasury yields are based on US 10-year government bonds, US Dollar basket is based on fixed weights against major trading partners, inflation is based on the US consumer price index, actual gold prices from Bloomberg. The fitted gold price is the price the model would have forecast. The constant does not have economic meaning, but is used in econometric modelling to capture other terms. It can be thought of as how much gold prices would change if all other variables are set to zero (although that would be unrealistic).

Historical performance is not an indication of future performance and any investments may go down in value. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

US Dollar pressure could ease

As we enter August 2022, we have witnessed US Dollar negative pressure on gold ease. Market consensus expects the US Dollar to depreciate going forward. The Dollar basket, currently at 106.2 is expected to depreciate to 101.8 by end Q2 20235. While most central banks have disposed of forward guidance tools and their policy course will be very data dependent, markets expect the Federal Reserve and European Central Bank to deliver most on their policy tightening in a front-loaded manner. Therefore, interest rate differentials may (at least initially) narrow, lessening the upward pressure on the US Dollar.

WisdomTree model points to gold price increases

Dollar depreciation is usually gold price positive, but for non-US Dollar denominated investors, the gains on gold can be lost when translating back to home currency. If we put consensus economic expectations6 into our gold model (and hold investor sentiment toward gold steady around current levels), gold could rise to $1825/oz by end Q2 2023, a gain of 6.9% relative to end Q2 2022. 2.5% of this gain comes from the Dollar depreciation that the market expects.

An example of why an unhedged position fails to benefit from US Dollar depreciation

Taking a numerical example, starting from an ounce of gold at US$1700/oz (i.e. €1734/oz with a EURUSD exchange rate at 1.02), if the US Dollar depreciates against the Euro by 5%, everything else being equal, the expectation is that the intrinsic value of gold would not have changed and therefore the price in Euro would remain €1734 per ounce. However, because of the currency move, the price in US$ is now 5% higher, i.e. $1785/oz. In such a scenario, the Euro investor unhedged would not benefit at all, the price of gold in Euro is unchanged after all. However, the hedged investor would benefit from the 5% increase in Dollar terms.

Currency hedging

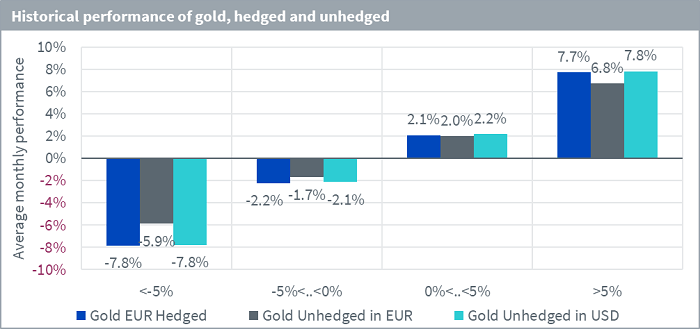

Currency hedging is one way of protecting a gold investment for non-US denominated investors. As an illustration, when we have seen gold price gains (in USD) greater than 5% m-o-m (which on average since December 2003 has given rise to gold performance of 7.8%), gold unhedged for Euro based investor has only returned 6.8%. Thus, an entire percentage point has been eroded by the currency translation. However, a currency hedged position would have on average performed 7.7% i.e. only 0.1% less than the US Dollar performance for a US Dollar denominated investor. Even in months when gold price gains were not as strong as 5%, for example between 0 and 5%, currency hedging has protected more of the gains.

Source: WisdomTree, Bloomberg, data from December 2003 to July 2022. Performance buckets based on gold in US Dollar on monthly basis.

Historical performance is not an indication of future performance and any investments may go down in value.

Conclusion

Gold prices in US Dollar terms tend to rise when the US Dollar depreciates (all else being equal). A non-US Dollar denominated investor holding their position unhedged would lose out on the proportion of gold gains that come from Dollar depreciation. A currency-hedged exposure would historically be the best way to attempt to preserve these gains.

Sources

1 Gold had reached US$2029/oz on 8 March 2022, dipped to US$1985/oz on 9 March 2022, touched US$2003 on 10 March 2022 before falling below the US$2000/oz thereafter (source: Bloomberg)

2 The Euro fell below 1 to the US Dollar on 14 July 2022 for a day (source: Bloomberg)

3 The Euro began trading on 1 January 1999 around 1.18 to the US Dollar and by 27 January 2000 it fell below 1. It remained below 1 until November 2002 (source: Bloomberg)

4 See Gold: how we value the precious metal for more details on the WisdomTree’s model

5 Using Bloomberg survey of economists from July 2022

6 Using Bloomberg survey of economists from July 2022, covering CPI inflation, 10 year Treasury Bond yields, and the US Dollar basket