European high yield bonds might be junk in name, but we believe there are hidden treasures in this much-maligned sector.

The definition of junk appears to be twofold:

- Any old or discarded material – as in metal, paper or rags.

- Anything that is regarded as worthless, meaningless or contemptible i.e., trash.

The European high yield bond index, which started in 1997 with just eight securities across six countries and a had total face value below €1 billion, now comprises 729 securities across 37 countries, representing €415 billion of borrowing.

For more than 25 years, investors, company managers, bankers and lawyers have become familiar with the nature of high yield borrowing. A generation has grown up understanding capital structures, multiples and appropriate leverage for different situations.

The result is the ICE BAML European High Yield Index, which has improved in credit quality, reduced its default rate, yet still wears the tag ‘junk bonds’.

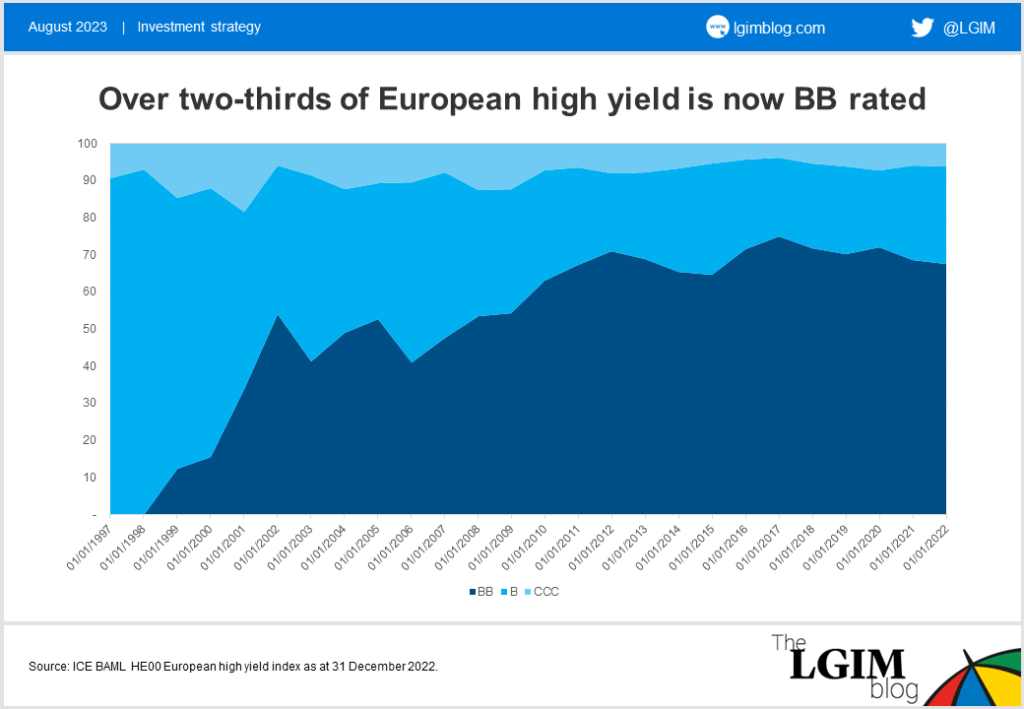

Lower-quality issuers leaving public markets

As can be seen from the chart, the highest-rated cohort of the market, BB bonds, has grown in representation from zero in 1998 to over two-thirds currently. This is a higher share than in the US and emerging market high yield markets, and we expect this improving trend in European credit quality to continue. By contrast, the lowest-rated CCC cohort has lately shrunk to just 6%, as lower-quality issuers leave the public markets and instead seek refuge in the loan and private credit markets.

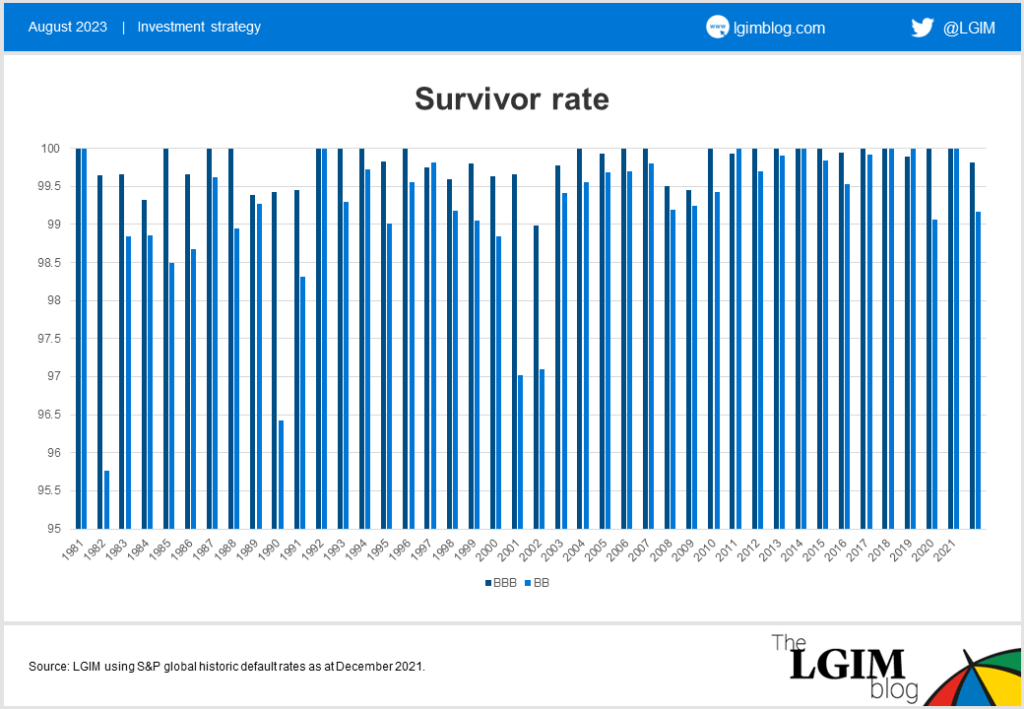

When we look at this majority share, BB bonds, we see established companies with financial metrics often not dissimilar to investment grade companies. And when we look at trailing survival rates, history suggests BB bonds have more in common with investment grade BBB bonds than with lower-quality B or CCC bonds.

Using historic global default rates for representation, on average 99.8% of BBB bonds survive, followed closely behind with 99.2% of BB rated bonds, as the chart below shows:

Using behavioural bias in our investment thinking

Behavioural bias features heavily in our investment thinking. Whenever we see assets that are described negatively but which, we believe, have underlying positive characteristics, we become interested.

Our research shows that throughout history, the yield investors have been paid to own BB bonds has exceeded, by a multiple of 4-5x, the losses suffered from defaults. In short, a strategy of blindly buying and holding BB bonds to maturity has always, theoretically, delivered a positive total return.

While past performance is no guide to the future, we believe this highlights the potential of any asset labelled negatively. Or to quote a well-known proverb: one man’s trash is another man’s treasure.