Key Takeaways

- The aviation sector has shown an impressive recovery from COVID-19, with air travel numbers back at pre-pandemic levels and the industry returning to profitability.

- This has led to a resurgence in leasing activity and senior financing, while the prospect of rate cuts should further boost investment opportunities by lowering the cost of capital for borrowers.

- Despite the historical resilience of the asset class, senior secured aviation loans continue to offer significant premia over corporate bonds and publicly issued aviation bonds.

- There is growing attention on how the industry meets 2050 net-zero targets. While sustainable aviation fuel has been touted as a solution, cost and supply issues have limited its usage so far.

In our latest Q&A, Alok Wadhawan and Tom Light share their thoughts on a remarkable turnaround in the aviation sector and the implications for investors.

Given the speed of its recovery, it can be easy to forget how the aviation sector was affected during the COVID-19 pandemic. In 2020 and 2021, global air passenger volumes plummeted 65.8% and 58.4% against 2019 levels as lockdowns put a stop to all but essential travel.1 Unsurprisingly, this hit revenues and profits, with airlines reporting combined losses of over US$185 billion in the 2020-2022 period.2

But, in what is a remarkable proof point of the resilience of the sector in the face of an almost unprecedented market and social event — not to mention the economic volatility seen since the pandemic caused by high inflation and rising interest rates — air travel numbers were back at pre-pandemic levels in 2023. The industry also returned to profitability last year, recording net profits of US$23.3 billion.3

This turnaround has filtered through to the aviation finance market, which has seen a revival in both leasing activity and senior financing. At the same time, higher yields and credit spreads relative to historical levels suggest the recovery has some way to go.

To understand what this means for the aviation finance asset class, we put the questions to Alok Wadhawan (AW), global head of aviation finance at Muzinich, and Tom Light (TL), aviation portfolio manager, Muzinich.

After losses caused by the pandemic, the airline industry has returned to profitability on the back of increased travel and cargo volumes. Are you seeing evidence of that in terms of origination activity and how do you expect the situation to evolve?

AW: The bigger picture of airlines returning to profitability and the recovery in air travel is fundamentally good for the credit quality of the industry. But in terms of transaction activity, much depends on the volume of aircraft being produced or traded. On the former, there is not enough supply to meet demand currently. On the latter, trading activity between leasing companies is picking up so we are seeing more opportunities on that side.

“Trading activity between leasing companies is picking up so we are seeing more opportunities”

Alok Wadhawan

It is important to recognise the resilience of the asset class over the past five years. The sector was one of the first to be impacted when the pandemic hit in 2020 and one of the last ones to recover. But the values of underlying aircraft held up and are now increasing,4 the industry has returned to profitability and recovered quicker than anyone could have expected. Since the start of the pandemic, Muzinich has financed or leased over 100 aircraft through multiple channels – directly with airlines, lessors, banks and secondary deals. We have experienced zero defaults to date, which speaks to the resilience of the asset class. Additionally, senior aviation loans are generating what we believe to be attractive cash yields.

Past performance is not a reliable indicator of current or future results.

TL: You have to factor in the potential level of downside protection for investors in this asset class. In the senior secured aviation loans market, the collateral against those loans are physical aircraft. If you have the highest quality aircraft as security for your transaction, your downside protection is relatively strong, especially on the senior loan side where LTVs are much lower than they were before the pandemic. It’s a similar story on the leasing side: current entry points are very attractive in our view.

“If you have the highest quality aircraft as security for your transaction, your downside protection is relatively strong.”

Tom Light

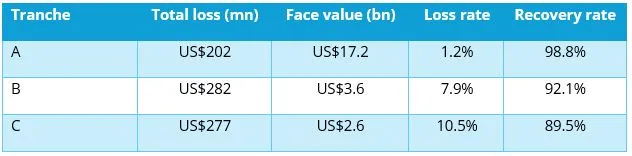

Historically, recovery rates for enhanced equipment trust certificates (EETCs), which are the most common form of publicly issued secured debt for airlines, have demonstrated the sector’s resilience. From 1994, the year the first EETC was issued, to November last year, recovery rates on this debt in the event of default are exceptionally high – 98.8% on single-A tranches, 92.1% on single-B tranches and even as high as 89.5% for C-rated paper.5 Compare that to the US corporate market, where historic recovery rates for senior secured bonds and senior unsecured bonds are 58.1% and 44.8%.6

This highlights how much structural support is embedded within aviation financings, from overcollateralization to the fact many deals are secured against aircraft.

Figure 1: Loss and recovery rates for EETCs in bankruptcy

Where do you currently see opportunities?

TL: For the last 12-18 months, we have mainly seen opportunities on the debt side. That is a function of higher interest rates. Typically, senior secured loans in the aviation sector are investment-grade assets, which in our view can potentially offer an attractive premium over corporate bonds and publicly issued aviation bonds. Based on the private transactions we have seen over the past year, the premium for senior aviation loans compared to similarly-rated corporate bonds and rated public aviation bonds can range from 200-400 basis points, depending on the quality of the borrower and quality of the collateral. In our view, this reflects the exit of some bank lenders from the sector and the illiquid nature of the asset class.

“Senior secured loans in the aviation sector offer an attractive premium over corporate bonds and publicly issued aviation bonds.”

Tom Light

While spreads blew out during the dislocation we saw during COVID-19, they remain wider than historical levels. In our view, that represents a mispricing given the recovery we are seeing in the sector.

Another trend that has increased the attractiveness of the asset class, in our view, concerns the fall in loan-to-values, which is largely due to the rise in interest rates. Pre-COVID, borrowers could access finance with LTVs of up to 80%, which was a function of the lower interest rate environment and greater risk appetite from lenders. Today, when base rates are above 4%, borrowers are not overextending themselves by taking out as much debt. There’s more equity on the transactions and we’re seeing LTVs in the mid-60s, which is a material change and positive from a lending perspective.7

AW: Given the quality of collateral, and the secured, investment-grade nature of the product, we believe those yields will look attractive to many institutional investors, including insurance companies who like the long-dated nature of the asset class to meet their liabilities.

In terms of the broader issue of opportunities for private lenders, this was a sector previously dominated by banks. What we have seen recently in Europe is a number of banks who were major players in the senior lending area either withdraw from the market or confirm they are looking at a potential exit.8

That space is being filled by large alternative managers, insurance companies and independent players like Muzinich. Insurers are particularly prominent: they like the rated element of the asset class from a capital perspective and the potential yields compared to equivalent asset classes in the capital markets. On the debt side, we are working with multiple insurance companies in Europe and the US.

While there is broad consensus the next move on interest rates will be for cuts, there is also an expectation they will remain higher for longer. What impact is that having in terms of origination and deal structuring?

TL: On the leasing side, the fact rates have stabilised is a positive. That allows lessors and airlines to make plans around capex, investment and sales. This has filtered through to the financing market, with more aircraft investment opportunities over the past six months or so. And, when central banks do cut rates, activity should logically pick up as buyers of aircraft will have a lower cost of capital.

At the same time, nobody expects interest rates to plummet back to zero. Airlines who need to meet upcoming bond maturities might not want to refinance at a much higher cost than they are used to and could look for other ways to generate liquidity. If that includes selling aircraft, this could be a source of opportunity for us, either to purchase the assets directly or to provide financing for potential buyers.

There is growing attention on how the industry can meet 2050 net-zero targets. Is that starting to feed through into the aviation finance market?

AW: Aviation produces around 2.5% of carbon emissions globally,9 so it is a relatively small, but not insignificant, part of a big problem.

Sustainable aviation fuel (SAF)10 can be part of the solution for the industry to get to net zero. But we have to caveat that for two reasons: firstly, SAF is currently a lot more expensive than jet fuel and is projected to remain so over the coming decades. Recent research from Bain and Company suggested SAF will still be two to four times more expensive than jet fuel in 2050.11 It’s possible that is too pessimistic a view – the technology is still nascent and various incentives could be introduced to close that gap – but it must become more cost-effective.

The second factor is supply – while demand is growing, SAF only accounts for around 0.2% of fuel used by aircraft and around 3% of renewable energy overall.12 There needs to be a major shift in the policy environment for that to change and for it to become a key enabler of the transition to net zero for the industry.

“There needs to be a major shift in the policy environment for sustainable aviation fuel to become a key enabler of the transition to net zero.”

Alok Wadhawan

There is also talk about electric engines, but that could be decades away in the commercial aviation sector. In Europe, we saw the first electric aircraft fully certified by the European Union Aviation Safety Agency in June 2020, but that is a two-seater used for pilot training and it is the only aircraft that has been certified so far.13 Airbus has a target to bring the world’s first commercial aircraft fueled by hydrogen by 2035, but the designs it is working on are for less than 200 passengers.14

So, going back to the question, yes, sustainability issues are important to us and our clients, particularly in Europe. But this area is in its infancy and not a major driver of the financing landscape yet.

References

1.International Air Transport Association, ‘Passenger Demand Recovery Continued in 2021 but Omicron Having Impact’, as of January 25, 2022

2.International Air Transport Association, ‘Airlines cut losses in 2022,’ as of December 6, 2022

3.International Air Transport Association, ‘Airlines set to earn 2.7% net profit margin on record revenues in 2024,’ December 6, 2023

4.International Bureau of Aviation, ‘Aircraft Engine Values & Lease Rates’, as of May 2, 2024

5.Kroll Bond Rating Agency, ‘EETC Resilience: Updated Historical Recoveries Through Pandemic and Beyond’, as of November 29, 2023. Most recent available data.

6.S&P Global, ‘U.S. Recovery Study: Loan Recoveries Persist Below Their Trend’, as of December 15, 2023. Most recent available data.

7.KPMG, ‘Aviation Leaders Report 2024,’ as of January 25, 2024

8.Standard Chartered, ‘Standard Chartered announces completion of sale of its global aviation finance leasing business to AviLease’, as of November 2, 2023

9.Our World in Data, ‘What share of global CO₂ emissions come from aviation?’, as of April 8, 2024

10.Sustainable aviation fuel is made from non-petroleum feedstock, including household waste and woody biomass.

11.Bain & Company, ‘A Realistic Path to Net-Zero Emissions for Commercial Aviation’, as of June 5, 2023

12.International Air Travel Association, ‘SAF Volumes Growing but Still Missing Opportunities’, as of December 6, 2023

13.European Union Aviation Safety Agency, as of June 10, 2020