KEY POINTS

1. We believe there will be improvement in Japanese corporate growth, profitability and financial returns.

2. Cash abounds in Japan, while U.S. and European stock markets have been rocked by the banking crisis.

3. Re-opening China and lifting COVID-19 restrictions provide a helpful boost for Japan.

4. Dividends are rising, share buybacks have increased and cross-shareholdings are being unwound.

London – Broad economic uncertainty and recent volatility in the banking sector have led many U.S.-based investors to seek opportunities that may be less impacted by these issues. In times like this, we believe there is potential merit in looking at international equity markets, such as Japan, that have a relatively low correlation with the S&P 500.

We recently returned from Tokyo, our first visit since December 2019 before COVID-19 closed Japan to foreign visitors. The country is opening up again after three years of pandemic-related restrictions. The mood is optimistic as corporations and consumers embrace a return to normalcy.

Creature comforts remain as major systemic and cultural changes unfold

Thankfully, much was unchanged. If you want real Wagyu steak, visit Japan. If you want to spend more, try Kobe steak. The sushi remains sublime, and a walk around the Tokyo Imperial Palace is as soothing as ever.

On one such walk, we were reminded that much change is underway in Japan. Looking at the palace reminded us that in 2021, Princess Mako, the niece of Emperor Naruhito, renounced her royal status to wed her college sweetheart, a commoner, winning headlines and signaling prospective change in Japan’s strict culture of tradition.

A new Central Bank Governor is about to be sworn in during a time of global consternation over rising interest rates. Japan is shifting away from its long-held zero interest rate policy. Such change excites us, as we believe there may be opportunities for improvement in Japanese corporate growth, profitability and financial returns.

In our ongoing efforts to minimize behavioral biases in our investment process, we have developed many proprietary portfolio exercises that are designed to help our portfolio managers and analysts systematically recognize and overcome behavioral biases. This year, we have used our portfolio exercises to refocus the team on Japanese equity idea generation. As a result, we have become increasingly optimistic that there is potential opportunity for investing in Japan, and we have recently increased our allocation to Japanese equities.

The outlook for Japanese corporate earnings in 2023 is reasonably robust. This is helped by the normalization of the economy and GDP growth,1 which is expected to be superior to both the U.S. and Europe in 2023. With inflation and interest rates on an upward trajectory, we anticipate a pivotal moment for the Japanese economy to move out of the deflationary low growth environment that dominated over the last 30 years. The current round of spring wage bargaining, or Shuntō,2 is around 3.7%,3 the highest percentage in 30 years.

China's reopening and re-entry of Japanese Tourists offer boost for Japan

The re-opening of China and lifting of COVID-19 restrictions also provide a helpful boost for Japan. The countries are close trading partners, and the return of Chinese tourists to Japan is expected to be an important tailwind. Japan is the top destination for Chinese tourists this year, and it is widely expected that pent-up demand will be unleashed on luxury goods, cosmetics, and other consumer goods.

We favor stocks that will benefit from this trend, as China is a large component of profits for several of them. Our meetings with consumer companies highlighted that all of them are intent on increasing marketing spend to try and maximize the expected jump in consumer spending both domestically and in China. We are identifying companies that we expect will help facilitate this trend.

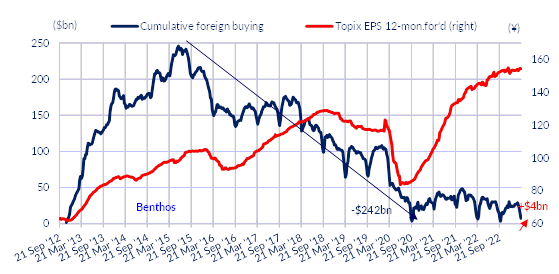

As we see in Europe, valuations are attractive in Japan, with the Tokyo Stock Price Index (TOPIX) 12-month forward PE multiple around 12.5 times, trading below the ten-year average around 14 to 15 times. Foreign investors have been reducing their allocations to the Japanese market in recent years. Just as we have seen in European equities over the last six months, it may be time for investors to return.

Despite resilient corporate earnings, foreign investors continue to shun Japan

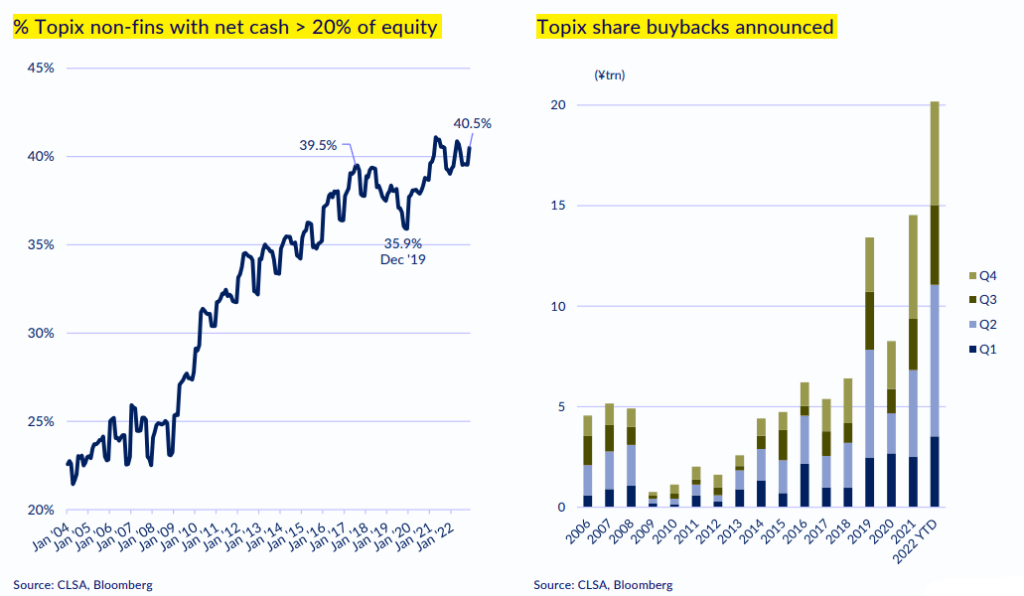

Excess cash abounds in corporate Japan

U.S. and European stock markets have been rattled by the most recent banking crisis that started with the collapse of Silicon Valley Bank a few weeks ago. At times like this, investors immediately start looking at the strength of companies’ balance sheets.

As illustrated in the left panel below, there has been a steady increase in the percentage of non-financial companies in the TOPIX with cash representing more than 20% of shareholder equity. Accordingly, we believe that many global investors will view the strength of Japanese corporate balance sheets as an obvious source of comfort in such an environment. Corporate Japan sits on an abundance of excess cash. For years, it led to balance sheet stagnation and declining returns on capital.

Buybacks at new highs — and potential for lots more

However, following the introduction of Japan’s Corporate Governance Code in 2015, we believe that excess cash is being put to better use. As shown in the right panel above, share buybacks have increased materially. Likewise, dividends are rising, and cross-shareholdings are being unwound. These dynamics present both safety and opportunity.

Over the longer term, we expect secular growth themes around de-carbonization, electrification, semiconductor capex and automation to provide interesting investment opportunities for corporate Japan. We own several Japanese companies that dominate niche growth markets on a global basis.

Bottom line: We often frame our team’s stock discussions around secular sales growth, profitability and return on capital. Both in the short and long term, we believe Japanese equities may improve on all of these. We certainly feel there are increasing opportunities to find companies that are amplifying business model sustainability. When we combine that with attractive valuations and a distinct lack of foreign ownership within Japanese equities, we believe the potential result is an increasingly appealing equity market for investors.

1 Global real GDP is forecasted to grow by 2.3% in 2023, down from 3.3% in 2022. Most weakness will be concentrated in Europe, Latin America and the U.S. Source: The Conference Board.

2 Shuntō is a Japanese term usually translated as “spring wage offensive,” which refers to the annual wage negotiations between enterprise unions and employers in Japan.

3 Japan Times, April 5, 2023

Risk Considerations: In general, equities securities’ values fluctuate in response to activities specific to a company. Investments in foreign markets entail special risks such as currency, political, economic, and market risks. The risks of investing in emerging market countries are greater than risks associated with investments in foreign developed markets.