On 3 August the Bank of England’s (BoE) Monetary Policy Committee (MPC) voted to hike interest rates by 25 basis points to 5.25%. With annual inflation at 7.9%, the central bank is expected to raise rates at least twice more to encourage inflation to return to the 2% target. In this Macro Flash Note, economists Joaquin Thul and Sam Jochim look at the outlook for UK inflation and the implications for the BoE’s next steps.

Following the August meeting, several members of the MPC noted that interest rates in the UK are restrictive for economic activity, but risks to inflation remain tilted to the upside. Sharp increases in energy, food, and other import prices over the last two years have affected domestic prices and wages. These effects are taking longer to unwind than initially anticipated. Hence, despite some recent improvement, annual inflation remains too high at 7.9%.

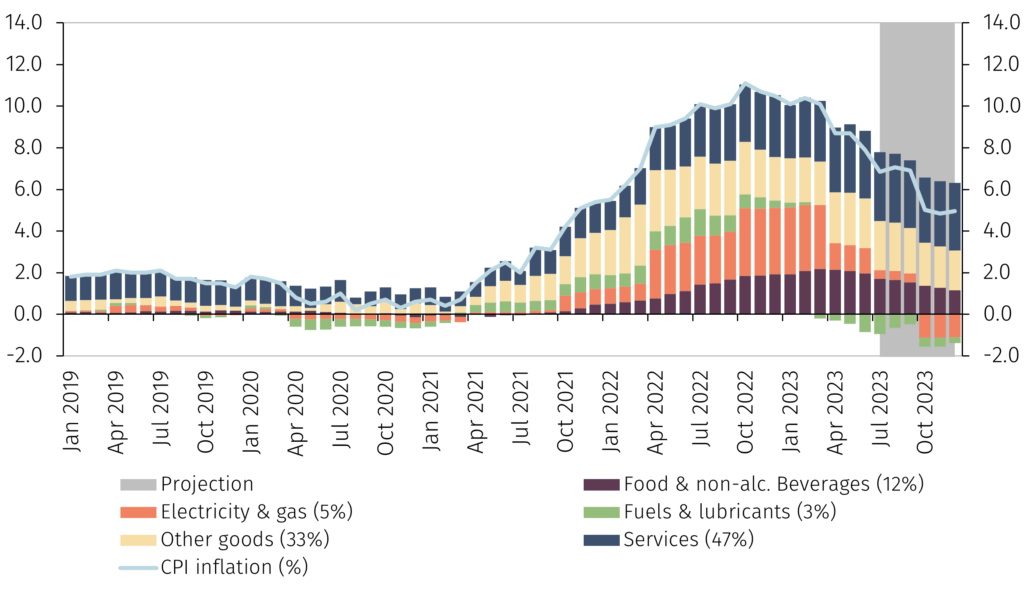

Chart 1. Contributions to UK CPI inflation (%) *

(*) Figures in parentheses are CPI basket weights in 2023.

Source: Bank of England and EFGAM. Data as of 3 August 2023.

Nevertheless, economic activity has been more resilient than previously expected. Underlying quarterly GDP growth was around 0.2% in the first half of 2023, with BoE officials expecting a similar rate of growth for the coming quarters. Relative to the previous forecasting round in May, the BoE revised up its projection for GDP growth in 2023 from 0.25% year-on-year (YoY) to 0.5% YoY. However, the BoE’s forecasts are conditioned on the market-implied path of interest rates which, given the persistence of inflation, has shifted up since May. With the higher rates path expected to weigh on demand in 2024 and 2025, GDP growth forecasts have been revised down for those years. The BoE now expects GDP growth to remain around 0.5% YoY in 2024 before slowing to 0.25% in 2025.

MPC members had previously acknowledged they were surprised by the increase in services prices of 7.4% YoY and private sector wage growth of 7.7% YoY in May, prompting a 50bps increase in interest rates at the June meeting. The decision to take a smaller step of 25bps in August was attributed to the improvement in inflation data during the month. After the meeting, MPC members explained that three indicators will be key to assess the future path of monetary policy:

- Services prices. These have been in an uptrend since mid-2021, driven by factors such as rising labour costs that have been slow to build up and are proving slower to unwind. The latest data on prices for services showed an increase of 7.2% YoY, representing a slight improvement from the 7.4% YoY increase in May. Nevertheless, the contribution of services is expected to remain elevated for the rest of 2023 (see Chart 1).

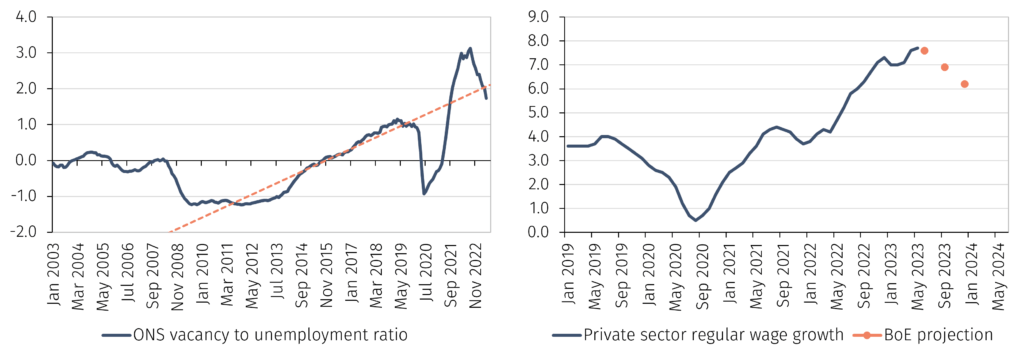

- Labour market. The strength of the labour market has driven improvements in household income following the Covid pandemic. However, some signs of loosening are emerging. The unemployment rate rose to 4.0% in the three months to May and the vacancies-to-unemployment ratio has declined, though it remains above its pre-pandemic level (see Chart 2.1).1

- Wage growth. Despite the tightness in the labour market, which has contributed to the rise in wage growth, some forward-looking indicators suggest that it will moderate in the second half of 2023. Indicators of private sector earnings growth, estimated by the BoE and the Office for National Statistics, show that wage growth is close to peaking and should decline to around 6% by year-end (see Chart 2.2).

Chart 2.1 Labour market / Chart 2.2 Wage growth

Source: Bank of England and EFGAM. Data as of 3 August 2023.

If, as we expect, the growth in services prices gradually declines, and labour market conditions continue to loosen, which contributes to wage growth moderating, then the MPC is likely to raise rates twice more by 25 basis points. This would bring UK interest rates to 5.75% by the end of 2023. However, if these indicators remain elevated and labour markets do not loosen, MPC members have not ruled out a further tightening of monetary policy.

To conclude, following August’s MPC meeting, the BoE stressed that the future path of interest rates will be data dependent. Further rate increases are likely to be required in the coming months and, at the same time, committee members noted that interest rates will need to remain restrictive for a sufficiently long time to return inflation to the 2% target. This is not expected to be achieved before Q2 2025. In the meantime, the transmission of monetary policy tightening to the economy through the housing market and the exchange rate will continue to put pressure on borrowers and moderate import prices through an appreciation of the pound. These effects are expected to contribute to inflation falling to around 5% by the end of 2023. Whilst this represents significant improvement, it is still a long way from the BoE’s target.