Summary

Asia remains a high growth region led by two of its largest emerging economies, China and India. Both countries are expected to contribute about half of global growth in 20231 . Singly, either one of these dominant markets offers a range of investment opportunities but together their complementary strengths reveal a deeper and wider pool of stock choices.

China is already a major economic powerhouse, having grown at around 9% per year since it began to reform its economy in 1978. Recognising that its high growth model based on investments, low-cost manufacturing and exports has mostly reached its limits, the government is accelerating the pivot towards domestic consumption and innovation to sustain long-term economic development.

On the other hand, India is still a rising economic power. As its development model focused on domestic demand and services, India’s growth has been more moderate than China. Nevertheless, it is now the fastest-growing economy in the world and has reached a stage where it is too big to ignore. To add, it is the world’s most populous country with one of the largest percentages of working age population.

On a standalone basis, these Asian giants already offer plenty of diverse investment opportunities. However, given that both are at a different stage of economic growth and development, their investment universes differ. As such investors who would like to get exposure to the biggest emerging economies in Asia can gain more from the combined and complementary strengths of China and India.

Expanding opportunity set

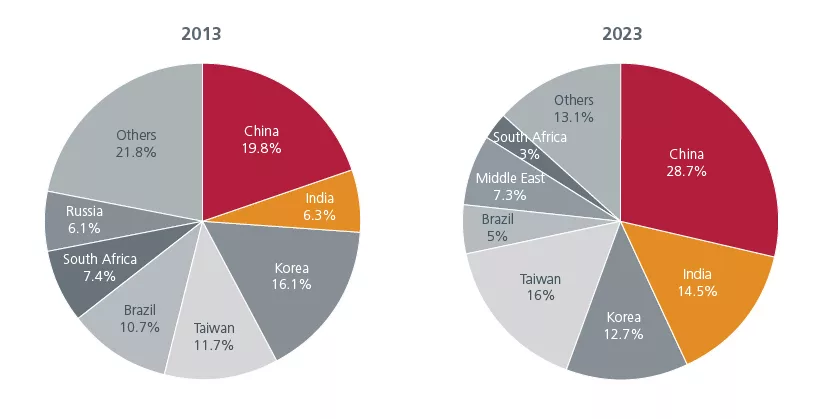

Within the MSCI Emerging Markets (EM) index, the weights of China and India have grown to 28.7% and 14.5% respectively as of May 2023. Ten years ago, their combined weight was only 26%. Fig 1. Likewise, within the MSCI Asia ex Japan index, they make up almost half the index weight. The rising dominance of China and India in the indices is a result of their rapid economic progress. We expect their combined weight in regional indices to continue its uptrend in the medium term driven by further A-share inclusion (China) and more initial public offerings (IPOs) in both markets.

Fig 1: Growing importance of China and India

A supportive regulatory environment is also underpinning Chinese and Indian capital markets. Over the years, India’s capital markets regulator, Sebi, has undertaken several enhancements; their latest proposal to reduce timelines for IPOs to three days from the six days at present when implemented will benefit issuers and investors. Likewise, earlier in the year, China relaxed the rules for IPO listings which will speed up listings and corporate fundraising.

Distinct sector strengths

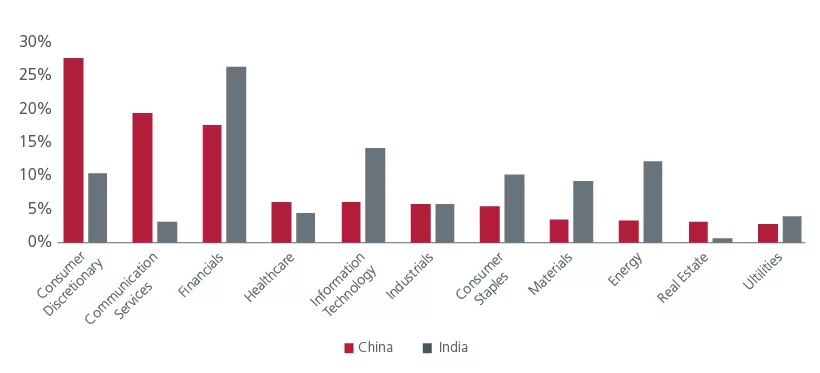

Another reason to invest in both markets is the opportunity to pick out the best ideas across a diversified range of sectors. The consumer discretionary sector has the highest weight in the MSCI China index while the financial sector is the largest in the MSCI India index. Fig 2. China’s consumer discretionary market is among the largest in the world and highly diversified into retail, e-commerce, travel, and luxury segments. On the other hand, India is the topmost offshoring destination for global information technology (IT) companies; the IT sector is expected to contribute to 10% of GDP by 2025. 2

Fig 2: Sector weights vary across both markets

Even within the same sector, the companies are distinct which allows active investors to maximise the stock picking diversity and focus on the best ideas. China’s banking sector is dominated by policy-driven state-owned enterprises while it is the private banks in India that are gaining market share from their state-owned counterparts.

The property sector is yet another example of this contrast; China faces an extended downcycle while India appears to be at the initial stage of a multi-year upcycle. Within healthcare, China’s big pharma companies are experiencing persistent price cuts domestically while India’s generic pharma manufacturers are fast diversifying from the challenging US generic market into new verticals such as innovative drugs.

Capitalising on differences

Having been the world’s factory for the past few decades, China is now transitioning to higher-quality growth and moving up the manufacturing value chain with a focus on innovation and higher-end equipment and industrial goods. Meanwhile India which has been well-known for being the world’s back office, is now establishing an additional pillar of growth in manufacturing by accelerating its infrastructure build-out and upskilling talents. This coincides with several multi-nationals’ “China plus-one” strategy. Data from US-based Reshoring Institute3 indicates that India is amongst the lowest-cost manufacturing hubs along with Mexico and Vietnam.

Likewise, the consumer sector is another clear example of the differences that can be exploited. Although India has pipped China to become the world’s most populous nation, the country’s consumer class (defined as those spending more than USD12 a day in 2017 PPP) is only half of China’s. However, China’s consumers are older and mostly live in cities. In contrast, India is on track to become the world’s biggest youth consumer market by 2030; yet the consumer class is both urban and rural.4 Consumption patterns which are usually dictated by affordability and lifestyle preferences will differ in both markets.

By investing in both markets, one will gain exposure to a wider spectrum of companies; their complementary nature implies investors get the best of both worlds.

The investment rationale

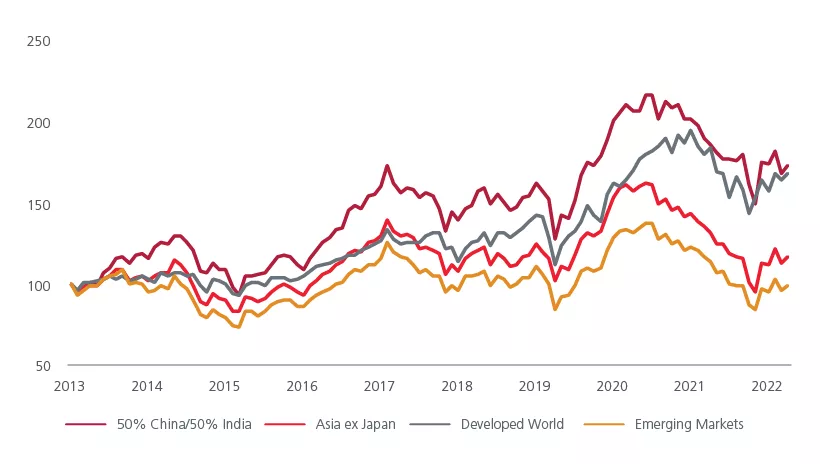

One could argue that investing in only China and India offers narrow diversification benefits. As both markets already form a big part of the MSCI EM and MSCI Asia ex Japan indices, investing in a broader emerging market or Asia strategy not only offers meaningful exposure to these markets but also diversification benefits from other countries. True, but whether such regional diversification dilutes one’s return is worth considering. Interestingly, empirical data reveals that a combined 50-50 China-India portfolio has outperformed the regional indices over the past eight years.

Fig 3: A combined China + India strategy has outperformed

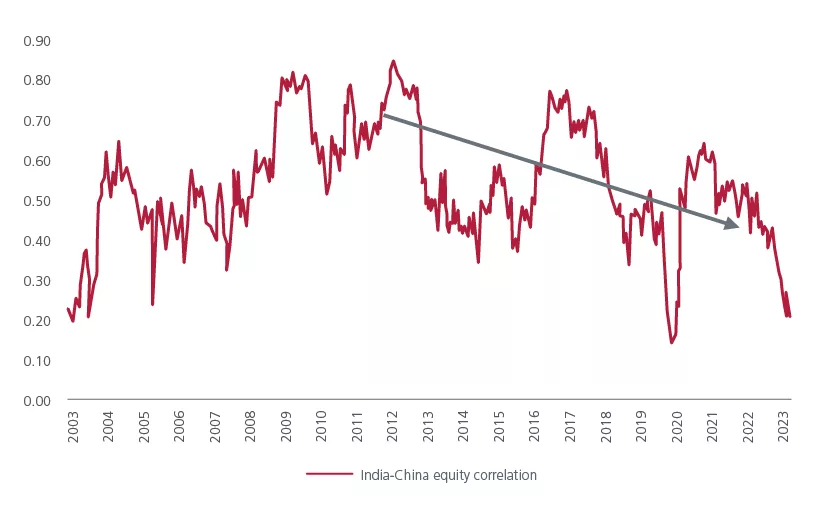

It is also encouraging to note the decreasing correlation between the two countries across multiple fronts –market performance, macro, and foreign flows. Fig 4. Differing valuations is an additional aspect; China is still cheap at one standard deviation below its 20-year average on a price-to-book basis while India is trading just above its average.5 The contrasting valuations offer active investors a dynamic pool of stocks to capitalise on mispriced opportunities in each market.

Fig 4 Decreasing correlation of the equity markets’ performance

All in, a combined China-India approach has its unique counter-cyclical benefits, providing a positive backdrop for bottom-up stock-pickers through market cycles.

Footnotes:

Sources:

1 IMF report, May 2023

2 https://www.ibef.org/industry/information-technology-india

3 https://thefederal.com/business/india-among-lowest-cost-manufacturing-hubs-beating-china-report/

4 https://www.brookings.edu/blog/future-development/2023/04/14/china-and-india-the-future-of-the-global-consumer-market/

5 Refinitiv Datastream, MSCI, 31 May 2023

Disclaimer:

This document is produced by Eastspring Investments (Singapore) Limited and issued in:

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K).

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

United Kingdom (for professional clients only) by Eastspring Investments (Luxembourg) S.A. – UK Branch, 10 Lower Thames Street, London EC3R 6AF.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).