It might seem a harsh economic environment for lenders. But not for those providing direct loans – less competition from the banking sector, the ability to select from companies with strong balance sheets and high yields make this an ideal entry point.

Rising interest rates, higher inflation and lacklustre economic growth may not sound like ideal investment conditions. But for private debt – lending directly to businesses – the climate is more favourable than it first appears.

An analysis of investment returns covering business cycles of the past 20 years supports our thesis. Direct lending strategies launched during difficult economic times – known as “in-cycle” vintages – have delivered above-average returns (see Fig. 1).

There are several reasons why that has been the case.

First, when central banks raise interest rates and the economy slows, investors find they can make loans on more favourable terms.

Second, as credit conditions tighten, companies respond by strengthening their balance sheets – which ultimately reduces risks for lenders.

Third, loans made during periods of economic uncertainty tend to have enhanced lender protections attached.

Stronger terms, defensive sectors

All of these factors apply today.

To begin with, the rates on offer for investors have indeed risen. Yields on European loans are now coming in north of 12 per cent, compared to 7 per cent this time last year.

That is primarily because private loans tend to be variable rate, with the cash coupon typically resetting every 30 to 90 days – a valuable feature at a time when European base rates are likely to stay higher for longer.

Secondly, companies that are seeking direct loans are – by and large – more financially disciplined than has historically been the case.

Today, there are many companies operating in Europe with relatively conservative balance sheets, or debt-to-EBITDA (earnings before interest, tax and amortisation) multiples of around 2-3 times. That is a marked improvement on what direct lenders have been used to.

Before the start of the current interest rate hike cycle, it wasn’t unusual to see private debt funds lending to firms with debt-to-EBITDA ratios as high as 7 times.

This suggests the upcoming wave of refinancing activity across Europe should offer new lenders the opportunity to recapitalise fundamentally sound companies with conservative balance sheets at a more attractive, lender-friendly yield level. With some EUR27 billion of European loans coming due in the next three years, this should give 2023 and 2024 vintages in private credit an additional tailwind.1 This ultimately makes direct lending a much more tenable proposition than it may have been 24 or even 12 months ago.

Fig. 1 – In-cycle advantage

Direct lending “in-cycle” returns vs long-term average

Finally, the terms on which loans are made are also becoming more favourable. In contrast to previous years, companies no longer have the easy option of borrowing via covenant-lite loans from banks.2

That is because commercial banks in Europe have been scaling back on loan-making. Credit standards are being tightened at the fastest pace since the sovereign debt crisis of 2011 according to European Central Bank data and some 15 per cent of corporate loan applications were rejected in the first quarter of this year – a record.

Which means many businesses have no choice but to accept much tighter terms demanded by private debt funds.

These include stricter rules covering acceptable levels of financial indebtedness and spending, as well as tighter covenants. They are all designed to enhance protections for creditors but also ultimately support companies in building strong and sustainable business models.

With lender protection strengthening, the credit quality of borrowers improving and loan pricing becoming more favourable, we believe the opportunities afforded by direct lending are more attractive than they have been for many years.

Partly for these reasons, the Pictet AM Strategy Unit has highlighted private debt as one of the most promising investment opportunities over the next five years, forecasting average returns in high single digits in Europe – comfortably above what is on offer from high yield credit both in absolute terms and on a risk adjusted basis (please click here to access our Secular Outlook).

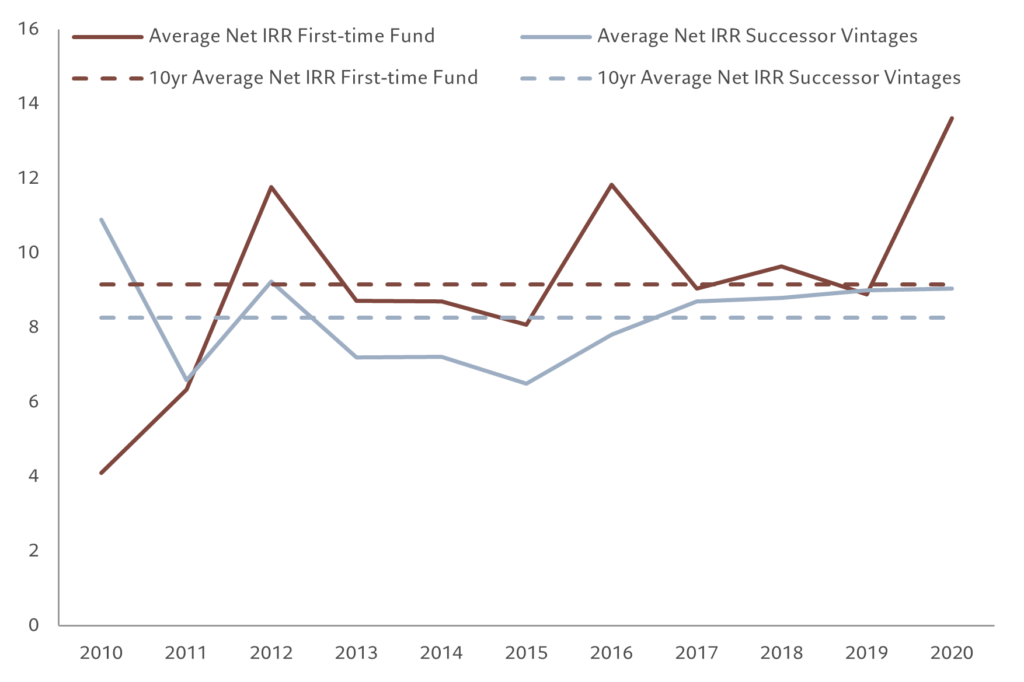

No “baggage” – a boost for first-time funds

For investors that allocate capital to first vintage private debt strategies, the rewards are potentially even greater.

First vintages typically concentrate lending activities in new niches that offer more opportunities. (At Pictet, we see such a niche among sponsor-less small- and mid-sized European companies, which are often overlooked by traditional private debt funds in favour of bigger private equity-backed deals.)

Moreover, by starting with a clean slate after a two-year period that has seen sharp increases in interest rates, first vintages do not have to deal with debtors struggling with higher borrowing costs. That is in contrast with older large direct lending portfolios, which will inevitably contain stressed assets given the pace at which central banks have tightened monetary policy.

Dealing with such problems is time-consuming for loan portfolio managers, as they have less time to dedicate to origination and selection – both of which are crucial to long-term investment success.

Fig. 2 – First vintage boost

Net internal rate of return (IRR) for developed market senior secured direct lending funds, %

[1] Pitchbook data based on Morningstar European Leveraged Loan Index as of 31.03.2023.

[2] Loans without maintenance covenants.