The ECB has cut the deposit facility rate by 0.25% to 3.50%, as expected. In this Macro Flash Note, Senior Economist GianLuigi Mandruzzato looks at what the central bank has signalled about the future path of interest rates.

As widely anticipated, the European Central Bank (ECB) cut the deposit facility rate (DFR) by 0.25% to 3.50%.1 During the press conference following the Governing Council meeting, President Lagarde said that the decision was unanimous and motivated by the progress made in returning inflation towards the 2% target. According to the new macroeconomic projections, which are essentially unchanged from three months ago, this should happen by the end of 2025.

Nevertheless, Lagarde hinted that the next interest rate cut will likely take place no sooner than December. The interval until the next Governing Council meeting is shorter than usual and therefore limited new information will be available to assess the inflation outlook.

In addition, the ECB expects inflation will fall significantly in September thanks to an energy-related base effect, but that same factor will cause inflation to rebound in the fourth quarter of 2024. This de-facto rules out the possibility that a soft inflation print in September will influence the outcome of the ECB meeting on 17 October.

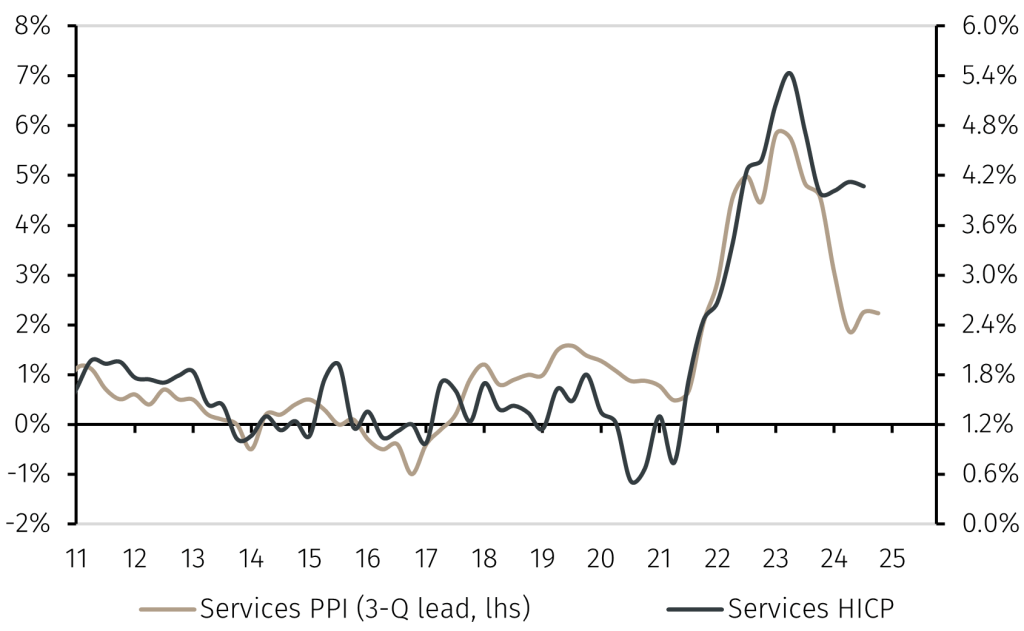

High service price inflation remains the main point of concern for the ECB, which it believes is linked to high labour costs and profit margins. In August, the services harmonised index of consumer prices (HICP) rose slightly more than 4% when measured both in annual and three-month annualised terms and has shown little progress since the end of 2023 (see Chart 1).

Chart 1. Services PPI and HICP (year-on-year)

Source: Eurostat, LSEG Data & Analytics, and EFGAM calculations. Data as of 13 September 2024.

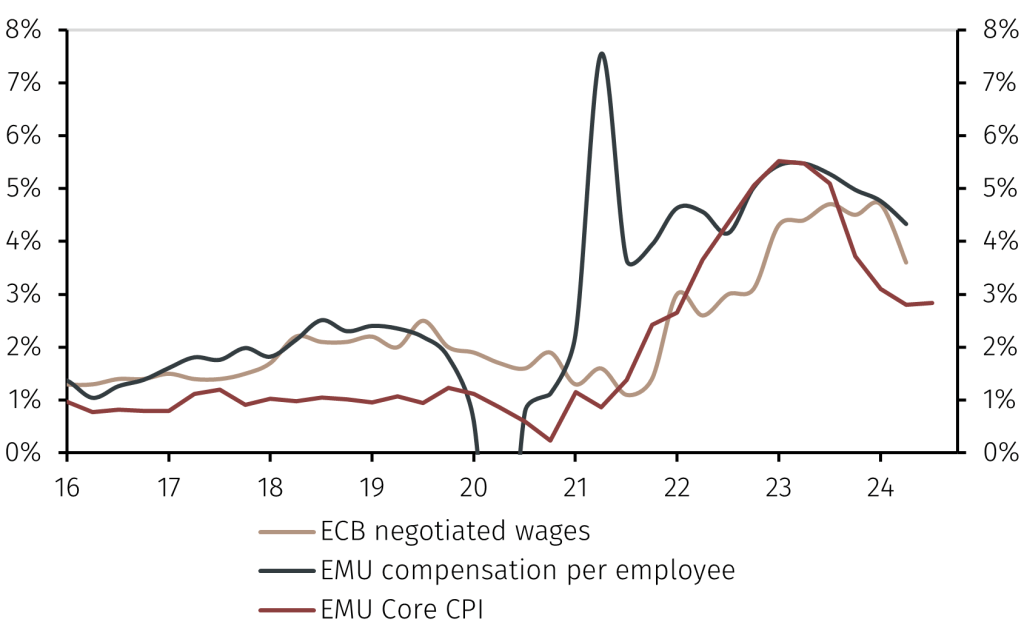

However, there are reasons for cautious optimism. In 2024Q2, the services producer price index (PPI), which historically leads the HICP by six to nine months, slowed to 1.8% from 3.0% year-on-year twelve months before (see Chart 1). Furthermore, a range of wage growth measures show they have moderated since the spring (see Chart 2).

Chart 2. Eurozone wages and core inflation (year-on-year)

Source: ECB, LSEG Data & Analytics, and EFGAM calculations. Data as of 13 September 2024.

In conclusion, the ECB did not surprise the markets and cut the deposit facility rate to 3.50%. However, Lagarde’s comments at the press conference appear to rule out a further rate cut before the December meeting and were marginally more hawkish than the market had expected. That notwithstanding, the weakness of the economy, particularly in Germany, and signs of declining price pressures in the services sector, including moderating wage growth, support an acceleration in the pace of rate cuts in 2025.

1 As announced in March, the interest rate corridor has been reduced to 0.4% by cutting the marginal lending rate and the marginal lending facility rate by 0.60% to 3.65% and 3.90% respectively. The measure aims at ensuring the effective implementation of the ECB monetary policy by reducing the volatility in money market rates.