Key Takeaways

- For investors in emerging markets, India is potentially one of the most exciting areas of opportunity, with a dynamic economy, growing labour force and strong balance sheet.

- With inflation looking manageable, the Reserve Bank of India is expected to maintain a stable policy environment, potentially lowering policy rates this year.

- For credit investors, we see the biggest opportunities in the corporate investment-grade market and high-yield segments.

- At a sector level, there are attractive opportunities in the services sector, renewables and infrastructure.

Portfolio managers Warren Hyland and Mel Siew discuss the key themes and topics in emerging markets and what investors should look out for in the month ahead.

The big story: Accessing the India growth phenomenon

Over the coming weeks, India, one of the world’s most populous country, takes to the polls in the world’s largest general election. Out of its population of 1.4 billion,1 close to one billion people will cast their vote2 in a process lasting six weeks. Current Prime Minister Narendra Modi, leader of the Bharatiya Janata Party, is expected to return to office for a third successive term.

By population and geographic area (1.3 million square miles), the numbers are huge. Equally sizeable is India’s 677million labour force,1 which is projected to reach 800 million by 2040.1 The country also has a fast-growing and dynamic economy with a strong balance sheet and independent and democratic institutions.

Against this backdrop, the International Monetary Fund recently upgraded its growth estimate for India to 6.8% from 6.5% for 2024, citing strong domestic demand.3 In our view, India’s growth momentum could make 7% achievable in the not-too-distant future.

While some developed markets continue to battle inflationary pressures, Indian inflation appears more manageable. Headline consumer prices eased to 4.9% year-on-year in March 4 and we project inflation is likely to fall to 4% (the Reserve Bank of India’s (RBI) medium-term target) later this year.

The current Goldilocks economic environment — not too hot, not too cold — should allow the central bank time to monitor incoming data without adjusting policy rates. We expect the RBI to begin policy normalisation in the fourth quarter, in line with the US, and we could well see policy rates lowered to 6% from the current 6.5% by year end.

As a result of this stellar set of numbers, India is on track to be the fastest-growing G20 nation in 2024 and the third-largest world economy behind the US and China before the end of the decade.4 However, given the sovereign does not directly issue US dollar-denominated debt, how can investors tap into this growth?

Accessing the domestic growth story

As India only issues local-currency debt, the pure sovereign market is off limits for US dollar investors. This generates strong investor demand for the Indian corporate investment-grade market – the natural home for investors looking for a similar risk profile to the sovereign – which they can access via quasi-sovereign cohorts such as Indian Rail or the State Bank of India.

For investors wishing to build exposure to the domestic growth phenomenon, we believe the focus should lean towards the high-yield (HY) universe. This segment has grown significantly, more than doubling in 5 years, from 10.8% in 2019 to 24.7% in 2023.5 Within that universe, the largest three sectors (44% renewables, 20% basic materials and 13% infrastructure) are mainly focused on the domestic economy.6

In our view, this should become a long-term underlying structural trend as India looks to close the development and infrastructure gap with China; the country is a key beneficiary of the “China+1” supply chain dynamic – whereby international companies look to broaden their exposure beyond China.

The China+1 theme is already in evidence; last year, US Treasury Secretary Janet Yellen visited India four times to encourage the shift in supply chains away from China.7 Technology giant Apple is also among those ramping up its Indian operations.8 Overall, the level of foreign direct investment has doubled since Modi took power in 2014, as Figure 1 shows.

Figure

1: Total foreign direct investment (FDI) inflows into India

Figure 1: Total foreign direct investment (FDI) inflows into India

Source: Department for Promotion of Industry and Internal Trade, as of December 31, 2023. Latest data available used. For illustrative purposes only.

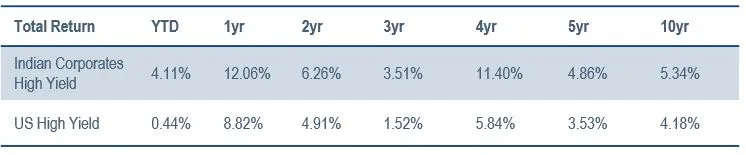

Figure 2: India HY versus US HY, total return by time period

Past performance is not a reliable indicator of current or future results.

Source: ICE Index Platform, as of 30th April. ICE BofA High Yield Emerging Markets Corporate Plus India Issuers Index (EINH), ICE BofA ML US Cash Pay High Yield Index (J0A0) For illustrative purposes only. Indices selected represent best proxy for asset classes. Index performance is for illustrative purposes only. You cannot invest directly in the index.

Figure

3: India HY has outperformed US HY

Figure 3: India HY has outperformed US HY

Past

performance is not a reliable indicator of current or future results.

Source: ICE Index Platform, as of April 30th, 2024. ICE BofA High Yield Emerging Markets Corporate Plus India Issuers Index (ENIH), ICE BofA US Cash Pay High Yield Index (J0A0). For illustrative purposes only. Indices selected represent best proxy for asset classes. Index performance is for illustrative purposes only. You cannot invest directly in the index.

Investment themes

There are several notable sectors within Indian credit where we see opportunities that tie in well with the country’s domestic growth story.

Services

India has one of the world’s largest emerging ‘service factories’ (services covering computers, insurance and financials, professional consulting, transport and travel). Service exports increased from US$53 billion in 2005 to US$338 billion in 2023, almost double the rate of world service export growth over the same period.9 This sector represented 9.7% of Indian GDP in 2023 9 and we believe this can continue in line with continued sector growth.

Renewables

India has been focusing on developing its renewables capabilities for some time, across green hydrogen, wind, hydro and solar power generation.

This initiative is underpinned by government policy to tender 50GW of renewables annually, working towards 1700-1800GW of renewable energy capacity by 2047. The government has also announced various incentives for green hydrogen with a target of 5 metric tonnes capacity by 2030.10 The majority of the country’s renewable energy was generated by hydro and wind power. However, given the country receives around 300 days of sunshine annually,11 concurrent with technological advances in the creation of solar panels, the country’s main renewable energy source now comes from the sun.

The sector has also been a key beneficiary of the broader FDI theme. According to the United Nations Conference on Trade and Development, India ranks in the top 5 recipients of FDI by number of greenfield renewable energy projects and international project finance deals (Figures 4 and 5).

Within this segment, we see compelling opportunities in onshore solar and wind power generators. These types of investments may appeal to those wishing for greater exposure to the Indian growth story and those looking to support the green energy transition.

Figure 4: Top five recipients of FDI by number of renewable energy projects

Source: United Nations Conference on the Trade and Development (UNCTAD), World Investment Report 2023, as of 31st December 2023. For illustrative purposes only.

Figure 5: International project finance deals

Source: United Nations Conference on the Trade and Development (UNCTAD), World Investment Report 2023, as of 31st December 2023. For illustrative purposes only.

The month in credit: Risk off

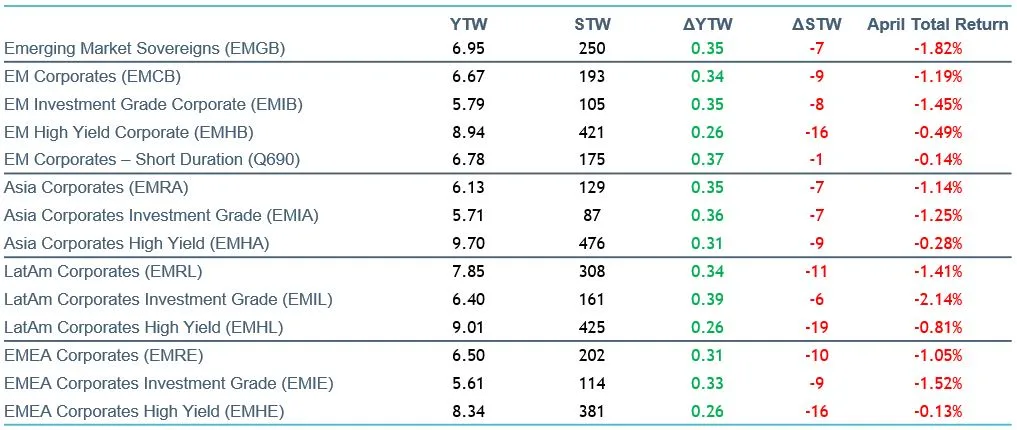

Following a strong first quarter, April was a weaker month for EM overall, as geopolitical tensions and rates volatility weighed on markets. Reflecting this backdrop, EM corporates outperformed sovereigns, HY outperformed IG (which tends to be more sensitive to rates volatility) and short-duration bonds outperformed their regular-duration counterparts. Drilling down further, B-rated bonds outperformed BBs within EM HY, while EMEA HY outperformed LatAm (see market data section for full sources).

Despite relatively strong performance within EM HY, defaults ticked up slightly to 0.7% year-to-date (slightly ahead of the US and Europe). However, for EM corporates overall, the YTD default rate is just 0.2%.12

One of April’s key drivers was sovereign ratings action. Fitch downgraded Panama to HY, highlighting the country’s fiscal and governance challenges that have been exacerbated by a recent mine closure and reliance on external financing. For China, Fitch revised its sovereign outlook to negative, citing concerns around public financing and the property sector. Peru, meanwhile, was downgraded by S&P to BBB-, noting political uncertainty and its negative effect on growth. Israel received the same treatment on the back of the recent escalation in geopolitical tensions. On a more positive note, S&P re-affirmed Hungary and Romania’s current BBB- ratings.

The growth picture in Asia surprised on the upside with Korea’s first-quarter GDP coming in at 3.4% year-on-year, up 2.2% from Q4 2023.13 Meanwhile, China reported GDP of 5.3% in the first quarter, up from 5.2% in the previous quarter.14 Industrial production led the positive surprise, driven by strong exports and manufacturing investment.

Past performance is not a reliable indicator of current or future results.

EM central banks continued their rate-cutting trajectory. In Peru, the central bank surprised the market with a 25 basis points (bps) cut down to 6%,15 while Argentina cut interest rates to 60% amid efforts to manage inflation and the fiscal adjustment.16

Colombia cut its basic rate by 50bps,17 and signalled a less dovish stance going forward, while Hungary lowered its base rate by 50bps to 7.75%,18 slowing its pace of easing in line with expectations. Indonesia was the exception, surprising the market with a 25bps hike to anchor FX stability and combat rising commodity prices. 19

The technical backdrop for the asset class remained robust, with US$31billion of new paper, which is down from the 5-year average of US$38 billion and leaves net supply for April at negative US$17.5 billion.20 At a regional level, the majority of the supply came from Asia while by sub-asset class the majority of supply came from IG rated issuers.21

On the lookout: What to watch out for in May

South Africa goes to the polls on May 29, and current polls suggest that African National Congress support is around 40%, which would see it fail to reach an outright majority for the first time since 1994. Former president Zuma’s MK (uMkhonto weSizwe) party support is around 8%.22

China’s five-day Labor Day holiday at the start of May is expected to show mobility and travel data at levels above corresponding periods in 2023 and pre-COVID 19. Survey data indicates the willingness to travel abroad is higher than last year and there is also an increase in expected travel budgets.

Regional outbound travel has been given a boost this year with mutual visa-free travel agreed to Singapore (30 days), Thailand (30 days), and Malaysia (15 days). In addition, travel to Hong Kong and Macau continues to be eased, with the recent announcement of a series of measures expediting visa processing and allowing longer stays.

On 15th May, Singapore’s second longest-serving prime minister, Lee Hsien Loong, is due to step down after almost 20 years in office. He will be succeeded by Deputy Prime Minister Lawrence Wong as power transitions to the ‘4G’ (4th Generation) leadership team.

Source: Muzinich & co as of April 2024. For illustrative purposes only.

Market Data – Credit

Market Data – Yield to Worst

Past performance is not a reliable indicator of current or future results

Source: ICE data platform. as of 30th April 2024. EMGB – ICE BofA Emerging Markets External Sovereign Index EMCB – ICE BofA Emerging Markets Corporate Plus Index, EMIB – ICE BofA High Grade Emerging Markets Corporate Plus Index, EMHB – ICE BofA High Yield Emerging Markets Corporate Plus Index, Q690 – ICE BofA Custom Emerging Markets Short Duration Index, EMRA – ICE BofA Asia Emerging Markets Corporate Plus Index, EMIA – ICE BofA High Grade Asia Emerging Markets Corporate Plus Index, EMHA – ICE BofA High Yield Asia Emerging Markets Corporate Plus Index , EMRL – ICE BofA Latin America Emerging Markets Corporate Plus Index, EMIL – The ICE BofA High Grade Latin America Emerging Markets Corporate Index, EMHL – ICE BofA High Yield Latin America Emerging Markets Corporate Plus, EMRE – ICE BofA EMEA Emerging Markets Corporate Plus Index, EMIE – ICE BofA High Grade EMEA Emerging Markets Corporate Plus Index, EMHE – ICE BofA High Yield EMEA Emerging Markets Corporate Plus Index,. Index performance is for illustrative purposes only. You cannot invest directly in the index. Indices selected provide best proxy for highlighting performance of emerging market corporate bonds. For illustrative purposes only

References

1.World Economic Forum, as of January 15, 2024

2.Commonwealth Parliamentary Association UK, ‘The Biggest Election in History Begins as India Goes to the Polls’ as of April 19, 2024

3.International Monetary Fund, Transcript of World Economic Outlook press briefing, as of April 16, 2024.

4.Reuters, India inflation likely cooled in March, albeit slightly, as of April 9, 2024.

5.ICE Index Platform, as of April 30th, 2024. ICE BofA Asian Dollar High Yield Index (ADHY)

6.ICE Index Platform, as of 30th April 2024. ICE BofA High Yield Emerging Markets Corporate Plus India Issuers Index (EINH).

7.US Dept of the Treasury: Remarks by Secretary of the Treasury Janet L. Yellen at US – Indian business council ideas summit, as of 13th June 2023.

8.CNBC “Why Apple is betting big on India”, as of 22nd April 2024.

9.Goldman Sachs, ‘India’s rise as the emerging services factor of the world’, as of April 17 2024.

10.Carbon credits.com – Indian government announces massive new green hydrogen project, as of February 23, 2024.

11.World Economic Forum, 30 November 2022

12.JP Morgan, EM Corporate Default Monitor, as of 15th April 2024.

13.Reuters, ‘South Korea Q1 GDP growth smashes estimates, but outlook’s uncertain. As of 25th April 2024.

14.CNBC ‘China’s economy grew 5.3% in the first quarter, beating expectations”, as of 15th April 2024.

15.Bloomberg UK “Peru Unexpectedly Cuts Interest Rate as Inflation Nears Target Band”, as of April 12, 2024.

16.Reuters, “Argentina cuts interest rate to 70% citing ‘pronounced’ inflation slowdown”, as of April 11, 2024.

17.Bloomber UK “Colombia Central Bank Lowers Key Rate Half a Percentage Point to 11.75%”m as of April 30, 2024.

18.Central Banking “Hungary cuts rates by 50 basis points”, as of April 24, 2024.

19.Reuters, “Indonesia’s central bank delivers surprise rate hike to anchor rupiah”, as of April 24, 2024.

20.JP Morgan, EM Corporate Default Monitor, as of 15th April 2024.

21.JP Morgan, EM Corporate Weekly Monitor, as of 6th May 2024.

22.Aljazeera “Can Jacob Zuma emerge as kingmaker in South Africa’s election?

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co are as of May 2024 and may change without notice.