If the song Barbie Girl had been written in 2022, it might go “life is hectic, not fantastic”. 2022 was another rollercoaster of a year, so just like the star of this summer’s blockbuster movie, retirees are weighing up what really matters in life and seeking some peace of mind as the latest research on LGIM DC members’ retirement behaviour suggests.

Retirement trends tend to move slowly, but 2022 heralded a noticeable change in the popularity of annuities.

Looking at LGIM’s DC retirement data1, annuities had fallen out of favour with the arrival of pensions freedom in 2015, but take-up rose last year from 3% to 7% among members with large pots.2

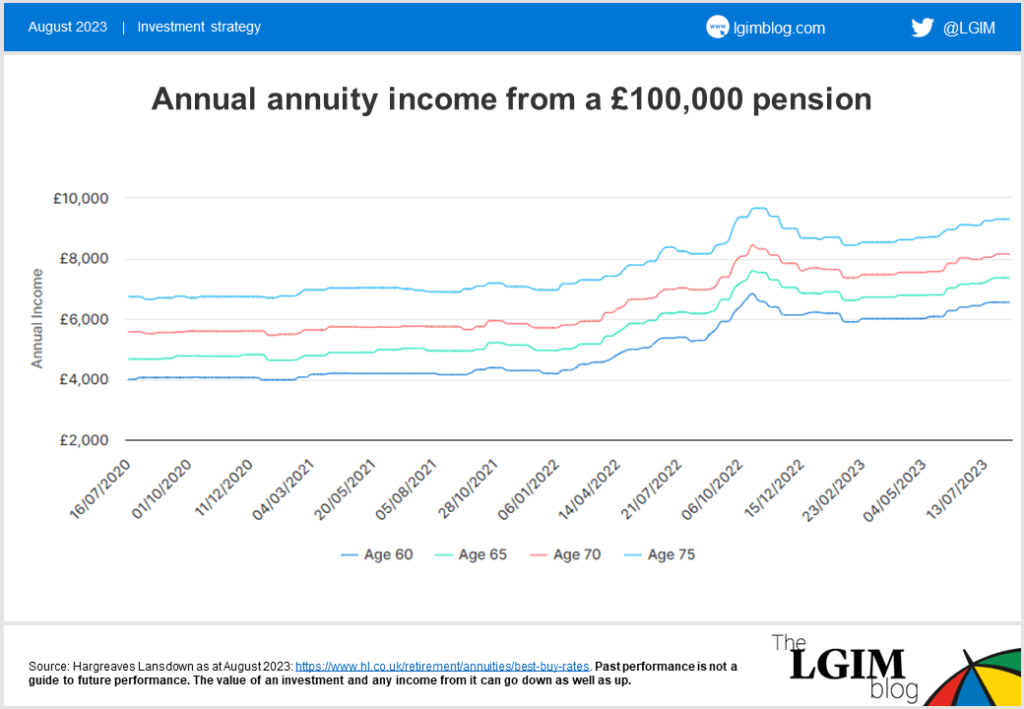

Annuity rates had been flat for years until 2022, when rates increased by as much as 37% from the start of the year to October.3 Rates took a bit of a breather earlier in 2023, but are nearly back at the peak level seen in October 2022.

Demand for annuities is likely to stick around in the face of an uncertain future (higher inflation may also push up demand for inflation-linked annuities; a fairly niche corner of the market), as retirees get much more bang for their buck at current rates, and if they delay retirement as observed over the last few years.

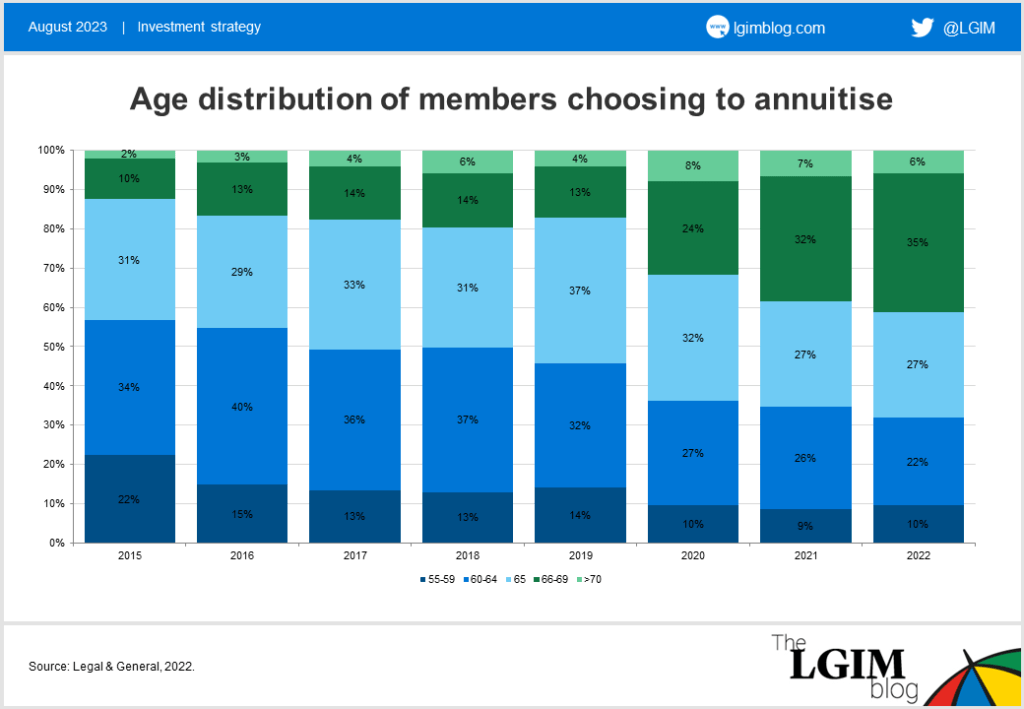

While members choosing to cash out or access drawdown (which accounts for 98% of retirees) are doing so sooner rather than later, the age distribution of members annuitising has shifted from early to late 60s over the last eight years. Some 56% of members annuitising in 2015 were under age 65, compared with 32% in 2022.

Compared with pot sizes in 2021, the average pot cashed out in 2022 was unchanged at £8,000, the average drawdown pot fell from £80,000 to £63,000, while the average annuity pot increased by 11% to £52,000. The divergence of pot movements reminds us that the path to and through retirement should not be one size fits all – different investment strategies and levels of risk aversion will set up incoming retirees at a wide range of starting points.

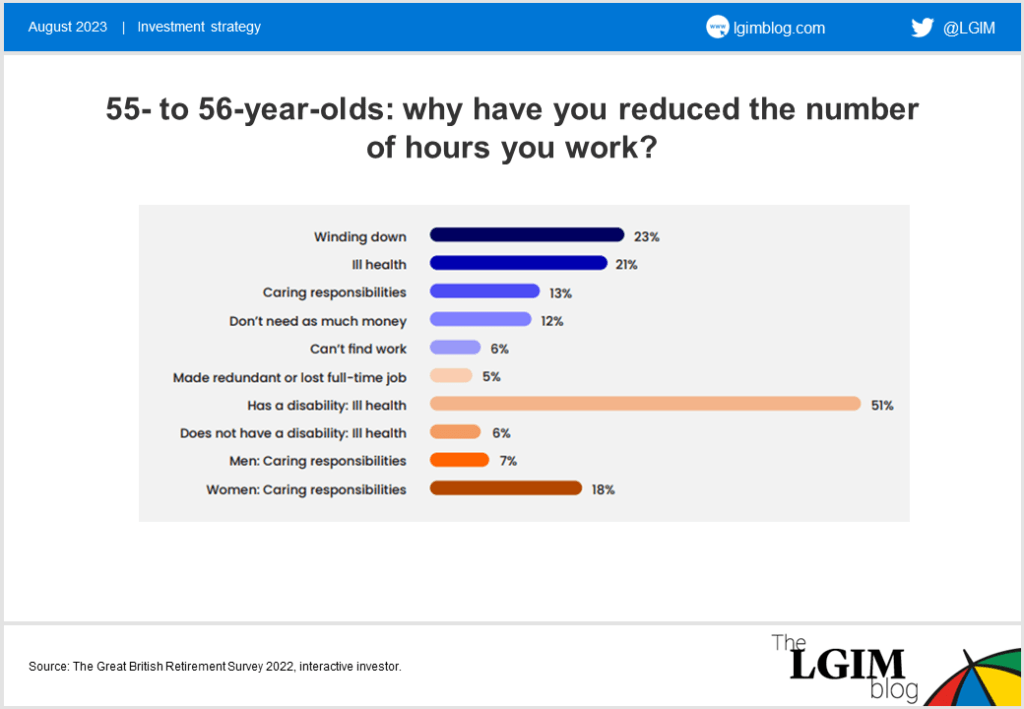

Another trend that has emerged since the pandemic is the exodus of those aged 55+ from the full-time workforce: the Great British Retirement Survey found that only one in three of those aged 55 and over are still in full-time work.4 The initial assumption (or hope!) had been that people had built up some savings during the pandemic and could comfortably retire.

However, more recent findings suggest that not everyone is throwing in the ‘9 to 5’ to sit on a beach and sip pina coladas – 12% surveyed said they didn’t need as much money, while 21% had reduced their hours due to ill health.

Many who were working part time or were self employed moved into retirement for several reasons including being furloughed, redundancy, mental health or a change in lifestyle, and some had benefited from building up savings during COVID-19.5

One consequence of retiring early is that retirees are usually at the point in their career when they are at their peak income potential. Dropping out of the workforce and ceasing pension contributions at this point can make a significant difference to the size of pot they get to live on in retirement.

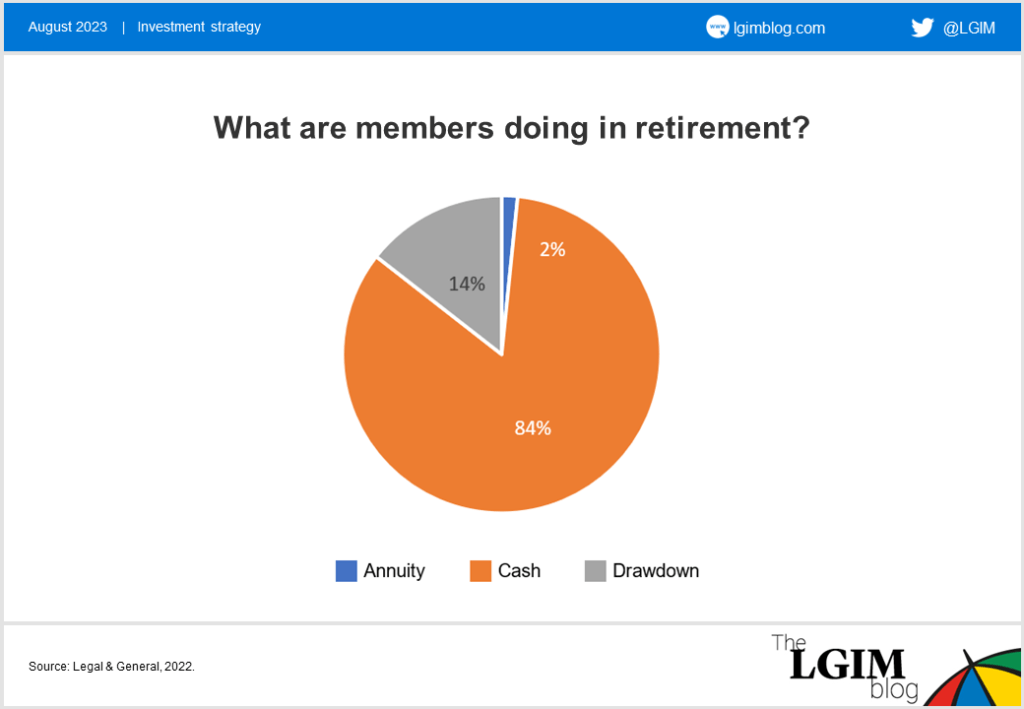

It has long been accepted that the reason most retirees are cashing out today is because they have small pots and other sources of income, such as a defined benefit pension. Of nearly 59,000 Legal & General members who retired in 2022, 84% of them cashed out. Broader research seems to suggest that health status could be another driver that schemes managers and pension providers should keep an eye on.

Another consequence of retiring early is the challenge posed to the UK’s economic recovery. The government tried to address this in the 2023 UK Spring Budget to encourage people to work longer or return to work.

Looking across the pond could give some indication of how this may play out – the US saw an excessive rate of early retirement during COVID-19 but there is evidence that the share of retirees returning to the labour market is creeping back towards pre-pandemic levels.6

While still too early to tell how successful some of these measures are, returning to part-time work could be the solution to balancing return to work and the individual’s health and/or carer considerations, which could accelerate the popularity of drawdown over the next few years.

Health or wealth?

The latest retirement trends suggest several possible perspectives to ponder. In the movie, Barbie uncharacteristically and abruptly blurts out mid dance party, “Do you guys ever think about dying?”

It might seem like a morbid question, but an unconscious choice everyone makes during their working life is between health and wealth. Most think about retirement assuming that they’ll be in comfortable health and worry about poor wealth, but in reality they may enter retirement in poor health and comfortable (enough) wealth.

Is spending half your days in retirement sleeping and watching TV worth the daily grind for several decades?7

“Imagination, life is your creation” – Barbie Girl.

1. 2022 data from Legal & General Investment Management (LGIM) DC business, as at March 2023. Figures relate to circa 59,000 Workplace members who retired in 2022.

2. Large pots defined as more than £150,000.

3. https://www.hl.co.uk/retirement/annuities/best-buy-rates (annuity rates for a 70-year-old).

4. The Great British Retirement Survey 2022, interactive investor: https://media-prod.ii.co.uk/s3fs-public/pdfs/GBRS_2022%20FINAL.pdf?VersionId=kqBcPXCu3WJ8EuDayUraHS_qE73pk0yF.

5. Chapter 3: Economic inactivity – who has left the workforce? Parliamentary publication on economic activity: https://publications.parliament.uk/pa/ld5803/ldselect/ldeconaf/115/11506.htm#_idTextAnchor039

6. ECB Economic Bulletin, Issue 6/2022: https://www.ecb.europa.eu/pub/economic-bulletin/focus/2022/html/ecb.ebbox202206_02~67d6677c0e.en.html.

7. How Do You Stack Up When It Comes to Retirement? Kiplinger Personal Finance: https://www.kiplinger.com/retirement/when-it-comes-to-retirement-how-do-you-stack-up.