Global stock markets have extended their November gains after latest data showed welcome falls in inflation on both sides of the Atlantic

With price rises in the United States and UK slowing more rapidly than expected, the likelihood of central banks being forced to keep interest rates higher for longer has receded, providing a boost for share prices. Meanwhile, signs that growth in the world’s largest economies is proving relatively resilient in the face of high costs and tight monetary policy has raised investors’ hopes of a “soft landing” following the tumult of recent years.

United States

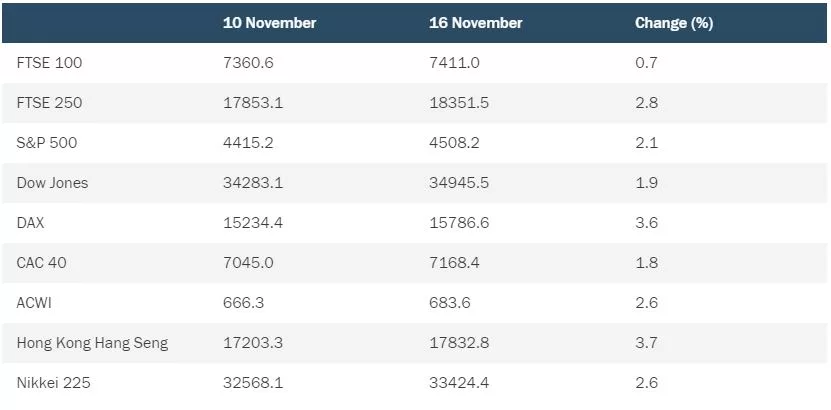

On Wall Street, the Dow Jones Industrial Average ended trading on Thursday 1.9% up for the week so far, with the S&P 500 advancing 2.1%. Shares in the US surged on Tuesday after official figures showed the annual rate of inflation had dipped to 3.2% in October – a steeper fall than analysts had forecasted. Markets are now expecting the Federal Reserve to cut interest rates as early as next May. Meanwhile, investors also reacted positively to the news that the House of Representatives had agreed a bill to avoid a government shutdown later this month, heading off another potential crisis.

UK

In the UK, the FTSE 100 closed on Thursday 0.7% up for the week so far. Inflation dropped sharply to 4.6% in October thanks mainly to a dramatic fall in the price of energy when compared with the same month in 2022. However, there were further signs that the UK economy is struggling to cope with high costs and elevated interest rates. Average house prices are reportedly falling at their fastest rate in five years, while insolvencies in England and Wales were up 18% in October on a year-on-year basis. Research suggests private-sector confidence had fallen to its lowest level this year.

Europe

In Frankfurt, the DAX index ended Thursday’s session up 3.6% for the week, while France’s CAC 40 gained 1.8%. Investors in Europe welcomed the news that the cost of gas was falling due to declining oil prices and the restoration of production at a major facility in the Middle East. Eurozone GDP was reported to have edged 0.1% lower in the third quarter, while the European Commission revised its growth forecast for the bloc lower. However, the prospect of interest rate cuts saw business sentiment improve in Germany.

Asia

In Asia, the Hang Seng index in Hong Kong gained 3.7% thanks partly to data showing a rise in industrial production in China and a larger-than-expected rise in retail sales last month. The summit between Chinese leader, Xi Jinping, and US president, Joe Biden, raised hopes of an improvement in relations between the two countries, a development that could have positive implications for trade. Japan’s Nikkei 225 index of leading shares advanced 2.6%, meanwhile, following positive news from China and the US. In addition, data showing the Japanese economy had contracted faster than expected in between July and September raised hopes of further stimulus measures from the Tokyo government.

Note: all market data contained within the article is sourced from Bloomberg unless stated otherwise, data as at 16 November 2023.