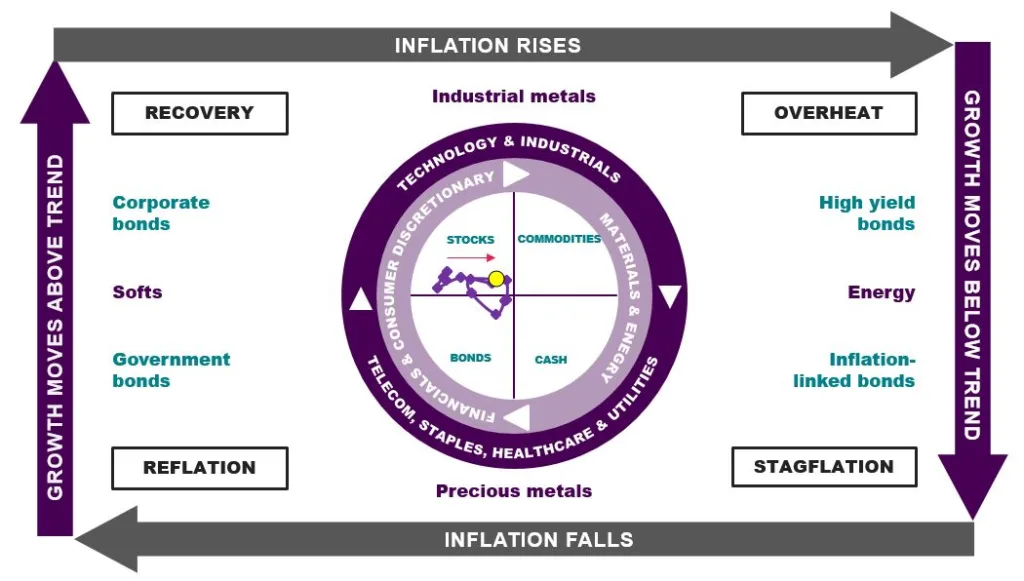

Our proprietary Investment Clock is just into its Recovery zone, indicating we are in the stage of the economic cycle when growth is improving (if slowly) and interest rates can begin to fall later this year as inflation weakens.

We wouldn’t be surprised to see a soft landing play out in the US but market expectations of several interest rate cuts have reduced significantly, to maybe one, given stickier inflation (owing to good growth). The US has been the best performing major economy while Europe and China have patchier growth pictures. Given this patchy but still somewhat improving global backdrop, we are positioned positively in our multi-asset funds and have benefitted from an overweight position in equities over the last 18 months.

Chart 1: The Investment Clock

In stock friendly Recovery but moving towards Overheat

Cross asset

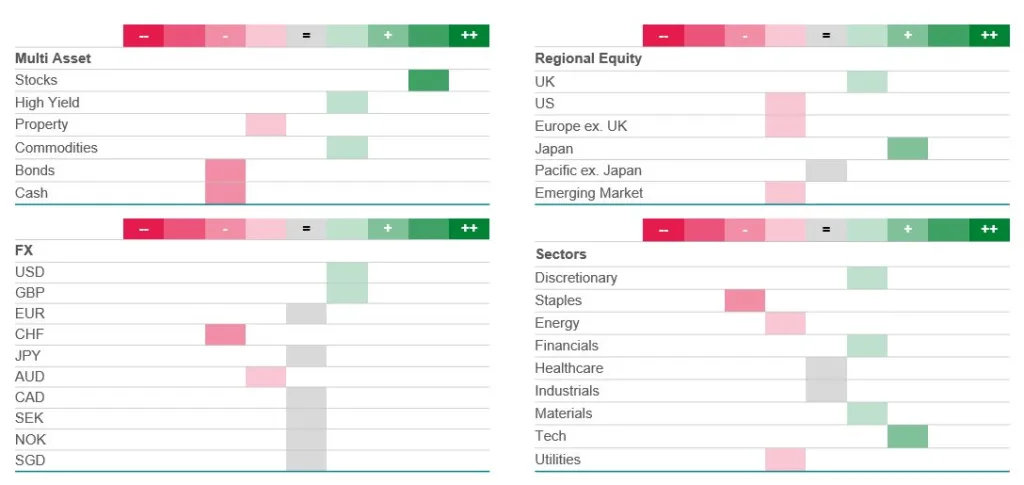

- Equities: overweight given a slowly improving macro environment and signs of earnings growth recovering.

- Commodities: overweight given some geopolitical risk and recovery potentially leading to stronger demand.

- Property: slightly underweight as the UK economy lacks strong positive momentum and interest rates are yet to fall.

- Government bonds: underweight as the market comes to terms with inflation being sticky (preventing interest rate cuts to date).

- Credit: constructive, but watchful for signs of stress.

Equity regions

- Overweight US equities given superior economic performance in America, compared to Europe and China, and the strength of tech-related earnings.

- Overweight Japanese equities which have done well on yen weakness.

- Underweight UK, Europe given the defensive nature of the sectors dominant in the UK market.

- Neutral on Asia Pacific and emerging markets given Chinese property debt issues and disappointing growth rates.

Currencies

- Underweight the US dollar as interest rates are likely to have peaked.

- Overweight sterling where rates are likely to stay higher for longer if (wage) inflation remains robust.

Sectors

- Overweight the interest rate sensitive consumer discretionary sector given rate cuts expected.

- Underweight energy and defensive utilities given we are not in a defensive period but growth is improving.

- Neutral to positive on technology given elevated valuations (but not underweight given growth potential).

Chart 2: Where we stand

Overweight global and Japan stocks, and growth sectors. Underweight bonds, cash, defensive sectors, and CHF.

Weightings may vary according to tactical asset allocation and the Fund may invest outside of indicated asset classes as the manager sees fit. The views expressed are the author’s own and do not constitute investment advice.

Source: Royal Londong Asset Management. Tactical positions as of 29 April 2024.

This is a financial promotion and is not investment advice. Past performance is not a guide to future performance. The value of investments and any income from them may go down as well as up and is not guaranteed. Investors may not get back the amount invested. Portfolio characteristics and holdings are subject to change without notice. The views expressed are those of the author at the date of publication unless otherwise indicated, which are subject to change, and is not investment advice.