Muzinich Weekly Market Comment: Green light for Bank of Japan?

In our latest round-up of developments in financial markets and economies, we consider the implications of an end to Japan’s negative interest-rate regime.

For the past year or so, market watchers have kept a close eye on events in the Land of the Rising Sun. While much of their focus has been on the surge in Japan’s stock market ― which has returned to levels seen during the country’s economic boom in the 1980s ― there has also been attention on when the Bank of Japan (BoJ) might end its negative interest rates policy (NIRP), in place since 2016.

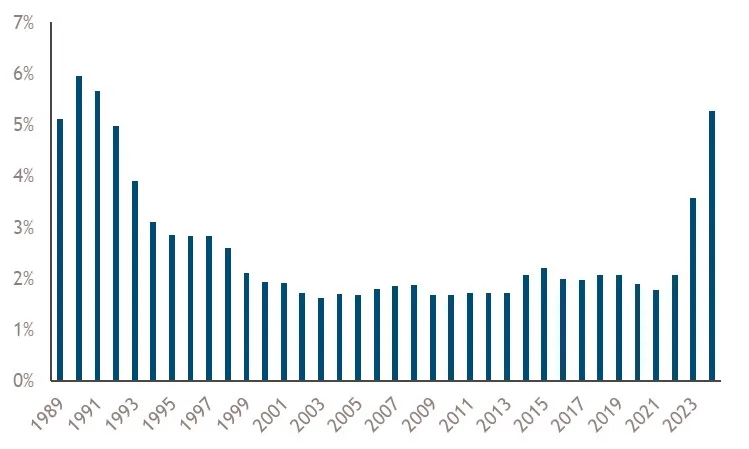

The BoJ has made it clear that to achieve its objective to keep inflation around 2% on a sustained basis, rising consumer prices need to feed through into wage demands. So, the announcement on March 15 that Rengo, the trade union group representing around 7 million workers, had agreed a wage increase of 5.38% with Japan’s biggest companies could be the green light for the BoJ to end NIRP and increase policy rates for the first time since 2007.1 The wage hike, which compares to 3.8% last year, will be the largest annual rise since 1981. (See Chart of the Week: Wage rises give BOJ green light to end NIRP.)

An exit from NIRP could be announced as early as this week, at BoJ’s upcoming monetary policy meeting.

The implications of higher Japanese rates

When policy rates and bond yields rise, the main beneficiaries are lenders at the expense of borrowers. This should improve the profitability of banks, pension schemes and insurance companies. However, the windfall may not be universal as paper losses from their government bond holdings could force some financial institutions to set aside extra capital, as we saw in recent crises affecting US regional banks and UK pension schemes.

It is projected that the Japanese government’s debt-servicing costs will increase to ¥27 trillion (US$180 billion), approximately a quarter of its annual budget for the 2024 fiscal year.2 As most homeowners in Japan have floating-rate loans linked to short-term interest rates, higher mortgage payments could reduce consumer spending and cool the housing market. As for corporate borrowers, there will be increased pressure on those who rely on cheap funding or have low profitability, as rising borrowing costs and tighter liquidity can accelerate bankruptcies.

From an investment perspective, and as we have seen recently with Mexico, higher policy rates can attract capital, from international but also domestic investors. Japanese investors have an estimated US$4 trillion of overseas investments, including US$1.1 trillion of US Treasuries3 and about 10% of both the Australian and Dutch government debt markets.4 Given the significance of the Japanese bid for international assets in recent years, an increase in interest rates could trigger a repatriation of capital and force global yields higher.

Higher policy rates could also strengthen the yen. This seems a strong possibility if Japanese rates rise while the US Federal Reserve and European Central Bank start cutting theirs. A stronger yen should help importers, including big buyers of commodities and energy, but at the expense of exporters, such as automakers. Toyota Motors estimates its operating profits are boosted by ¥45 billion (US$300 million) for every ¥1 fall against the dollar. Finally, Japan’s booming tourism industry could slow down from a stronger yen, impacting the hospitality and retail sectors.

Also in the news last week

Government bond yields rose last week, with US debt underperforming. Oil prices reached new highs for 2024, with the WTI Crude index topping US$81 on March 15.

The US dollar appreciated against most currencies, the notable exception being the Mexican peso — the best-performing major currency this year — which appreciated to levels not seen since 2015. With policy rates at 11.25%, solid growth and political stability, Mexico continues to attract capital. US equity indices ended broadly flat for the week, while on the economic front, inflation data was the key variable for investors to pore over and drive market prices.

In the US, both headline and core consumer prices increased by 0.4% month-over-month in February. Energy was the major contributor to headline inflation, with gasoline prices increasing 3.8% after falling 3.3% the previous month.

For core prices, economists will be relieved core service inflation moderated to 0.5% in February versus 0.7% in January due to a slowdown in owners’ equivalent rent (OER), its moderation confirming January’s surprising jump was likely just noise. On a 12-month basis, core prices continued their disinflationary trend, with the 3.8% increase in February slightly down on the 3.9% reported in January. However, on a six-month basis, core prices picked up to 3.9% from 3.6%, a possible sign disinflation momentum is stalling.

At the company level, producer prices were higher than consensus, rising by the biggest amount in six months — 0.6% versus the 0.3% expected — partly due to high fuel and food costs. Several categories from the Producer Price Report are used to form the Fed’s preferred inflation measure, the personal consumption expenditure index (PCE). Prices paid for portfolio management, a key constituent of the PCE index, rose 0.2%, a sign of stability after increasing 5.9% in January.

In Asia, Chinese consumer prices in February unexpectedly rose 0.7% year-over-year (YoY) versus the consensus forecast of 0.3%, with the Lunar Near Year in January continuing to distort economic data. A more representative measure is to take an average of the first two months, which shows consumer prices remained unchanged YoY. In contrast to the US, Chinese producer prices continued their deflationary trend, falling 2.7% YoY.

Chart of the Week: Wage rises give BoJ green light to end NIRP

Annual Rengo average pay increases (%)

Source: Bloomberg, as of March 15, 2024. For illustrative purposes only. References to specific companies is for illustrative purposes only and does not reflect the holdings of any specific past or current portfolio or account.

1.Reuters, ‘Japan union group announces biggest wage hikes in 33 years’, March 15, 2024

2.Bloomberg, ‘Winners and losers from Ueda ditching negative rates in Japan’, March 13, 2024

3.US Treasury, ‘Major foreign holders of Treasury Securities, March 15, 2024

4.Bloomberg, ‘Winners and losers from Ueda ditching negative rates in Japan’, March 13, 2024

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed by Muzinich & Co. are as of 18 March 2024 and may change without notice. All data figures are from Bloomberg as of 18 March 2024, unless otherwise stated. 2024-03-18-13163