The Long Time Series, back to the 1970s

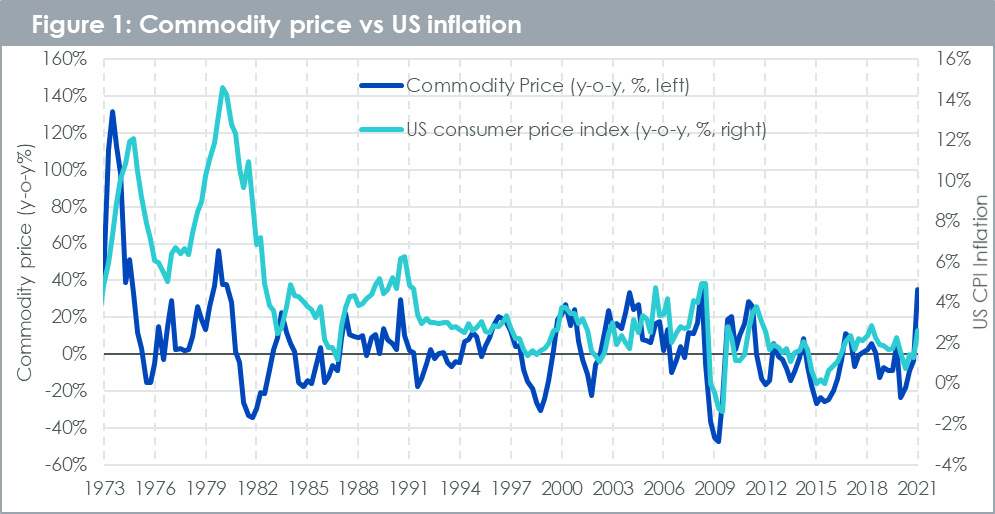

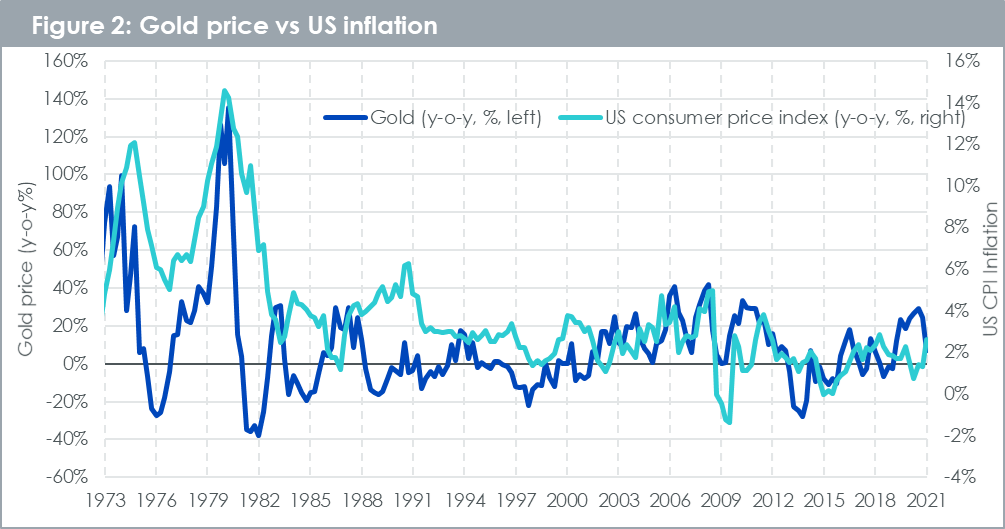

Commodities have historically been an excellent hedge for inflation. Figure 1 below shows that commodities have typically risen in times of higher inflation. Figure 2 shows also that gold has historically been a strong hedge for inflation. The relationship may not have been as tight for gold as it has been for the broad basket across most of the time series, but in the 1970s, when inflation became particularly elevated, gold did an exceptional job in hedging against increasing price pressure.

Source: WisdomTree, Bloomberg. Commodity price is based Bloomberg Commodity Total Return (BCOMTR Index); US CPI inflation. March 1973 to March 2021. Using Quartey frequency of data.

Historical performance is not an indication of future performance and any investments may go down in value.

Source: WisdomTree, Bloomberg. Data as of 31/03/2021. Gold price is based Bloomberg spot prices; US CPI inflation. March 1973 to March 2021. Using Quartey frequency of the data.

Historical performance is not an indication of future performance and any investments may go down in value.

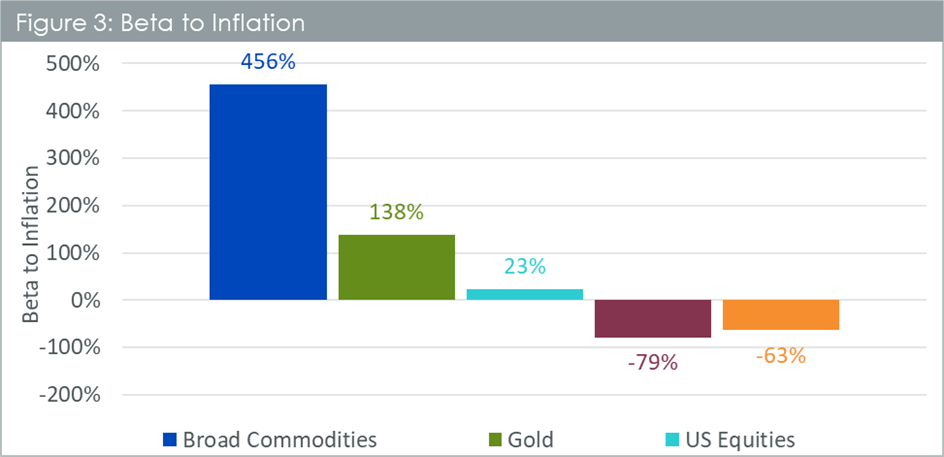

The Link between Inflation & Returns: Beta (1988 to 2021)

Looking at the numbers, commodities have a higher beta to inflation than any other asset class, including gold (Figure 3). Gold, never-the-less has a very strong inflation-beta, which is many multiples higher than equities. As we will see later, this indicates that while broad commodities follow inflation upward but also downward, gold tends to follow only on the upside, which translates into an overall smaller beta. Several asset classes respond to ‘expected inflation’, where expectations are often formed by monetary conditions and judgements over the strength of demand in the economy. These expectations are often demand focused. However, Inflation can also be generated by supply-side shocks. For example, the cyber-attack on the Colonial Pipeline last month increased the price of gasoline fuel for consumers[1]. Or, there is the example of the ongoing drought in Brazil that is pushing up the price of food items[2]. Most asset classes tend to react a lot less to this type of inflation, but commodity prices have a direct link to many supply-side shocks, which may make it a superior hedge to realised inflation. Those examples of supply-side shocks often tend to squeeze margins of companies and so are not positive for equities or corporate bonds.

While figure 3 shows the betas for the full time series, more than 30 years, we recognise that these statistics would not sit at constant levels. During the period from 2010 to 2020, these figures were 6.2 for broad commodities, 1.1 for gold, 2.0 for US Equities, -1.2 for US government bonds and -0.6 for US corporate bonds. Gold’s notably lower beta in the 2010s, once again speaks to the fact that gold does better in high inflation environments and the 2010-2020 period was notable for the absence of strong inflation. Investors have to consider whether they believe the 2020’s are more like a continuation of the 2010’s or something more similar to a prior historical paradigm.

Source: WisdomTree, Bloomberg. From 31st December 1988 to 31st May 2021. Calculations are based on monthly returns in USD. US Equities stands for S&P 500 gross TR Index. US Government Bonds stand for Bloomberg Barclays US Treasury TR Index. US Corporate Bonds stands for Bloomberg Barclays US Corporate TR Index. Broad commodities stands for Bloomberg Commodity TR Index.

Historical performance is not an indication of future performance and any investments may go down in value.

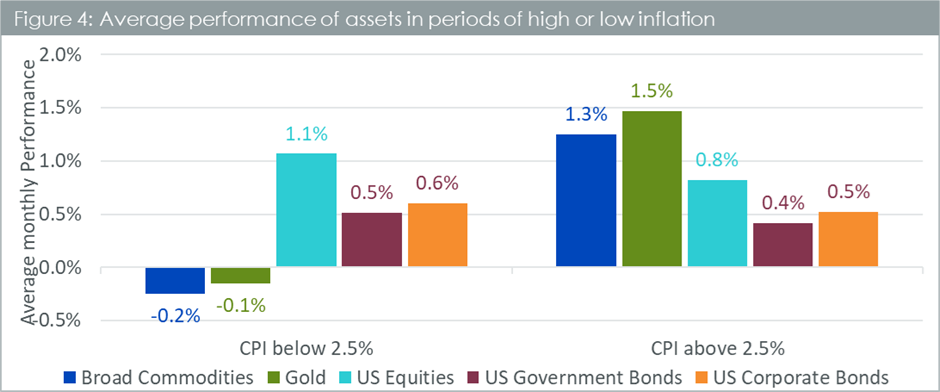

Gold has an Asymmetric Character

But this only tells part of the picture. Gold behaves in a very asymmetric fashion. It tends to perform really well when the economy is performing badly (for example in the aftermath of an economic shock) and it also performs very strongly in periods of economic strength when inflation is elevated. Gold doesn’t do as well when the economy is middling along (typically periods of time when inflation is just moderate). Figure 4, shows that gold is the best performing asset class in times of elevated (above 2.5%) levels of inflation and has outpaced commodities during such times.

Source: WisdomTree, Bloomberg. From 31st December 1988 to 31st May 2021. Calculations are based on monthly returns in USD. US Equities stands for S&P 500 gross TR Index. US Government Bonds stand for Bloomberg Barclays US Treasury TR Index. US Corporate Bonds stands for Bloomberg Barclays US Corporate TR Index. Broad commodities stands for Bloomberg Commodity TR Index.

Historical performance is not an indication of future performance and any investments may go down in value.

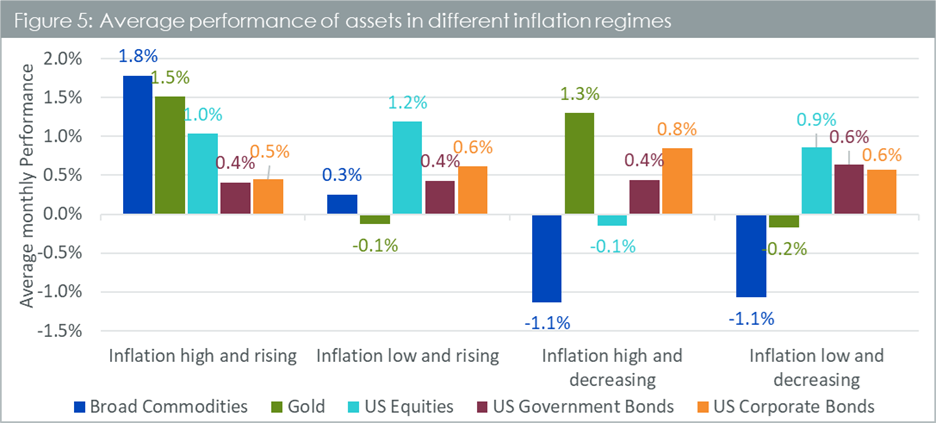

Levels of Inflation vs. Expected Future Path of Inflation

High inflation scenarios are gold price positive, regardless of whether the rate of inflation is rising or falling (figure 5). Commodities on the other hand tend to benefit from rising inflation. When inflation has passed its peak, it tends not to be as commodity price supportive.

Source: WisdomTree, Bloomberg. From 31st December 1988 to 31st May 2021. Calculations are based on monthly returns in USD. US Equities stands for S&P 500 gross TR Index. US Government Bonds stand for Bloomberg Barclays US Treasury TR Index. US Corporate Bonds stands for Bloomberg Barclays US Corporate TR Index. Broad commodities stands for Bloomberg Commodity TR Index.

Historical performance is not an indication of future performance and any investments may go down in value.

While we believe that inflation will ease a little in the short-term after the enormous base-effect from ultra-low energy prices last year pass, we believe that inflation is far from transitory. Looking at the detail behind the CPI[3] readings, inflation seems to be broad-based. The scale of monetary growth, combined with the pent-up demand for many goods and services will be a recipe for continued price inflation even after the extraordinary base effects pass. Inflation may very well rise again after the base effects are behind us. Broad commodities and gold are likely to be essential assets to protect your portfolio against inflation.

Conclusion: What are you Hedging for?

Each investor’s portfolio will have its own character and its own particular risk tolerance. Those who are worried about the dawning of a new era with risks to fiat currency rising would likely benefit more from holding more gold or even bitcoin and moving away from fiat monetary systems. However, those who are seeing shortages of key products central to economic growth—those that may benefit from the pull of economic demand—may benefit from a broader basket of commodities that each respond from their own unique supply/demand considerations.