Key Takeaways

Profit margins are healthy, though earnings growth has slowed markedly in the U.S.

Inflation remains a top concern for many businesses as once-voracious consumers begin to tighten their belts and change their spending habits.

Estimates for future profits are still rising in Europe but declining elsewhere amid concerns about slowing global growth.

Europe Again Outpaced the U.S.

Despite rising economic and geopolitical headwinds, corporate profits continued to grow in the opening months of 2022. Europe outpaced the U.S. for the third consecutive quarter, with earnings climbing 35% and more than 71% of companies beating analysts’ estimates. U.S. earnings growth slowed dramatically, falling to 9%, with 77% of companies outperforming expectations.1

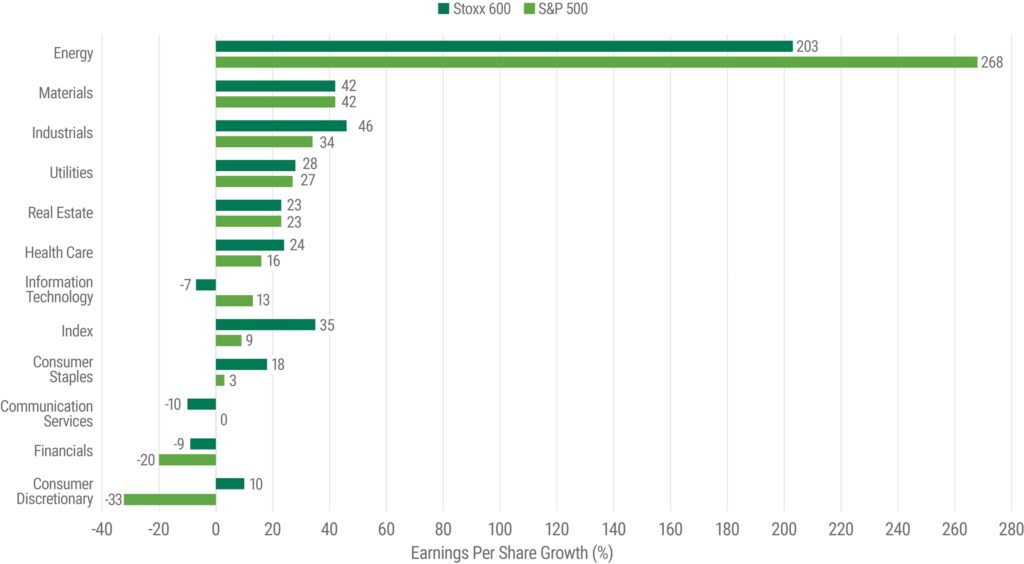

Overall earnings figures are somewhat misleading given the strong performance of the energy sector. As shown in Figure 1, the sector’s earnings growth was 268% in the U.S. and 203% in Europe, dramatically higher than all other areas. Excluding energy, earnings growth was only 3.1% in the U.S. and 12% in Europe.2

Industrials, materials and utility companies also delivered double-digit earnings growth in the U.S. and Europe. Meanwhile, communications services and financials were weak performers in both regions. The impact of inflation and souring consumer sentiment is reflected in sharply negative earnings growth in the U.S. consumer discretionary sector.

Though profit growth slowed, margins remained robust as businesses passed through higher costs to customers. U.S. profit margins came in above the five-year average at 12.3%. In Europe, the average profit margin was 9.6%.3

Figure 1 | Energy Profits Dwarf all Other Sectors

Inflation Tops the List of Worries

Macro concerns often emerge as significant talking points during management conference calls with analysts. For example, “supply chain” was frequently referenced at the height of the pandemic disruption (and it remains a key concern). As we noted last quarter, inflation has become a critical theme more recently. Management teams for S&P 500 Index companies mentioned inflation in 85% of calls this quarter compared to just 12% after the onset of the pandemic in 2020.

With inflation top of mind, cost-conscious businesses are seeking to make their operations more efficient. These efforts could benefit select information technology businesses, especially those that can help companies streamline their workflows and reduce their dependence on labor. Indeed, Microsoft’s CEO said that though corporate budgets are getting tighter, some companies are accelerating their IT spending to speed up digitization and automation projects.

Management Comment on Efficiency Spending:

“I have not seen this level of demand for automation technology to improve productivity. Because in an inflationary environment, the only deflationary force is software.”

Satya Nadella, CEO, Microsoft

Consumers Feeling the Inflation Pinch

Thanks to the strong jobs market and government support, consumers have been resilient up to this point. We’re now starting to see some cracks. Lower-income shoppers, in particular, are feeling the sting of higher food and fuel costs, which is reducing their spending on discretionary items.

The strain is apparent in disappointing results for Walmart and Target. In addition to reporting higher-than-expected supply chain costs, they saw a shift in customer spending from general merchandise toward groceries, which have lower profit margins.

The companies’ management teams also discussed using discounts to clear out inventory. Retailers had limited supplies of many products, such as TVs, bicycles and kitchen appliances, at the height of the pandemic. Now, they’re overstocked as customers tighten their belts and shift their spending habits.

Management Comment on Retail Spending Shifts:

“In our other three core merchandise categories, apparel, home and hardlines, we saw a rapid slowdown in the year-over-year sales trends beginning in March, when we began to see the impact of last year’s stimulus payments. While we anticipated a post-stimulus slowdown in these categories, and we expect the consumer to continue refocusing their spending away from goods and into services, we didn’t anticipate the magnitude of that shift.”

Brian Cornell, CEO, Target

Shift from Goods to Services Continues

The demand for leisure travel strengthened in 2021 and has continued to accelerate. This trend is reflected in results for hotels, restaurants and airlines, which posted some of the highest year-over-year growth outside of the energy sector.

Marriott reported that while business travel has lagged, demand has improved as more employees have returned to the office. The company also saw more bookings that blended travel and leisure.

Management Comment on Travel Demand:

“We’ve finally reached the inflection point as we transition from pandemic to endemic, and demand is stronger than I’ve ever seen in my career. And that’s even before business travel fully recovers, though it continues to accelerate at a rapid pace, and before international, especially Asia, fully recovers.”

J. Scott Kirby, CEO, United Airlines

The Stay-At-Home Bubble is Bursting

Many companies that were beneficiaries of stay-at-home mandates reported disappointing first-quarter results and saw their stocks trade lower.

Amazon.com is experiencing a double whammy. Demand is falling back to earth after massive pandemic gains, while the company’s costs rise sharply. The management team reported that the cost to ship an overseas container is more than double pre-pandemic rates. Further, the cost of fuel is approximately one and a half times higher than a year ago.

Netflix, another stay-at-home beneficiary, confirmed investors’ worst fears about rising costs and the increasingly crowded streaming market. The company reported disappointing results due to growing competition and the impact of massive spending on content to attract and retain subscribers. The company also affirmed expectations that growth would slow as it reached higher levels of market penetration.

The pandemic increase in streaming demand helped mask some of these issues. However, with people getting off the couch and back out into the world, Netflix’s subscriber growth missed expectations, forcing management to lower its earnings forecast. To help support future revenue growth, the company announced an advertising-based model and said it would fight password sharing more aggressively.

Expect Earnings Growth to Slow in the Second Half of 2022

We expect earnings growth to slow in the coming months with inflation, monetary tightening and the war in Ukraine hanging over the global economy. Other headwinds include weak real wage growth and its pressure on consumer spending, the energy price shock in Europe and COVID-19 lockdowns in China.

Despite this gloomy backdrop, analysts have raised their second-quarter estimate for profit growth in Europe to 15.3%. Meanwhile, they have lowered their U.S. profit growth estimate to 4.4%. Forecasters expect energy and industrial companies to post the highest growth in developed markets. They are also calling for solid earnings growth for industrials and materials companies in the U.S. and consumer products companies in Europe.

Meanwhile, we think the flattening yield curve will compress net interest margins and pressure U.S. and non-U.S. financials, particularly banks. We also expect earnings pressure at U.S. utilities, communications and consumer-oriented companies.

Is All the Bad News Priced In?

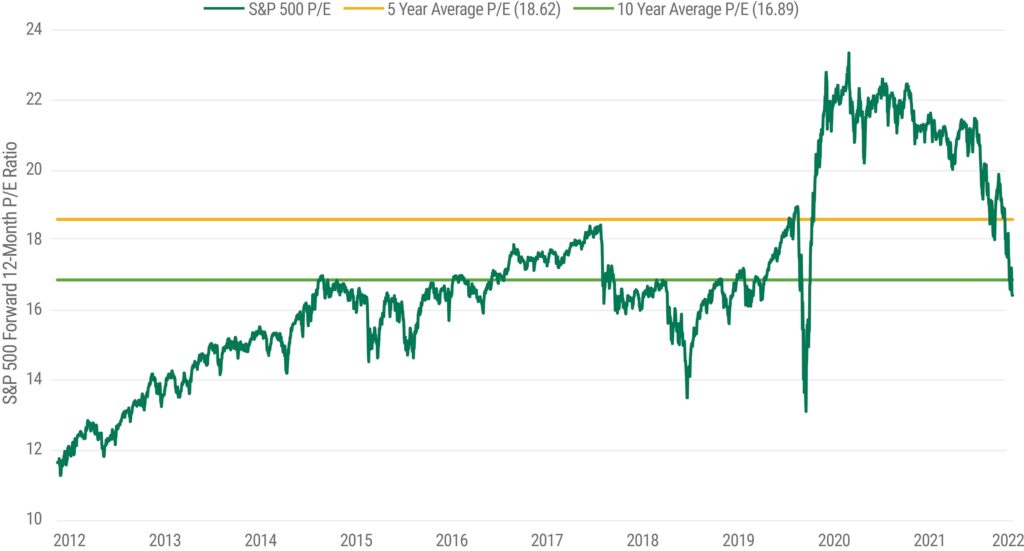

Strong earnings growth in recent years coupled with the market sell-off in 2022 have made valuations look more reasonable. As shown in Figure 2, the forward 12-month P/E ratio for the S&P 500 Index is below the 10-year average. It has touched levels not seen since 2019, if you exclude the brief COVID-19-induced bear market in 2020. Prices also appear attractive in Europe, with Stoxx 600 companies trading below long-term average valuations.4

Even in an uncertain environment, companies are maintaining healthy profit margins and continue to deliver earnings growth. So, we think the market is moving in anticipation of poor results in future quarters. We believe this market action could be similar to the sharp rise in stock prices and P/E ratios coming out of the COVID-19-induced downturn of 2020. At that time, investors bid up prices before there was evidence of earnings growth.

In the months ahead, we expect continued volatility as the market tries to calculate how the challenging macroeconomic backdrop will affect corporate profits. We believe this scenario highlights the importance of security selection.

Figure 2 | Valuations Have Dropped Below the 10-Year Average

1Source: FactSet.

2Source: FactSet.

3Source: FactSet.

4Bloomberg.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments’ portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

The information is not intended as a personalized recommendation or fiduciary advice and should not be relied upon for, investment, accounting, legal or tax advice.

No offer of any security is made hereby. This material is provided for informational purposes only and does not constitute a recommendation of any investment strategy or product described herein. This material is directed to professional/institutional clients only and should not be relied upon by retail investors or the public. The content of this document has not been reviewed by any regulatory authority.