Our daily lives are becoming increasingly digitalised. Read our perspective on the opportunities and challenges this profound shift presents to businesses and some of the companies well placed to benefit.

No trend has been more radically entrenched and accelerated by the pandemic and its lockdowns than the digitalisation of everything. In the paradigm-shifting tug of war between the atom and the bit, the physical and the virtual, the last two years will be seen as defining battle fronts.

We can witness this digital onslaught everywhere. The smartphone has long been the essential conduit of modern life, but the sheer time real-estate allocated to it has become mind-blowing. In 2021, with people confined to their homes for all but the most essential of tasks, the average person globally spent 4 hours and 48 minutes per day on their mobile phones, 1/3 of their waking life. This is up 30% on 2019 levels – on aggregate that means around 10bn extra hours a day of smartphone time across the planet in 2021 vs 2019, with every hour kicking out reems and reems of data, all of which serve to create ever more fleshed out, nuanced digital facsimiles of the person clutching the phone, which in turn can be fed back into making that mobile experience more tailored, more enticing.

And it is fascinating to note that in the splurge of mobile time, emerging markets are not simply on a par with developed markets, but have leap-frogged them, with Brazilians, Indonesians and Indians spending more hours per day than their American and European peers on their mobile phones, as the chart shows. This emerging market leadership is visible across a huge range of digital areas, particularly where the mobile phone is the interface – China has more smartphones than Western Europe and North America combined.

Retail on the go

The mobile phone has become the essential platform for gaming, for communicating, for entertaining, for learning, and for purchasing. There were almost 6bn finance apps downloaded in 2021 on smartphones (in India, mobile finance apps downloaded surpassed 1bn last year), up 74% on 2018 levels, as people manage their money in radically new ways. 233 smartphone apps or games worldwide in 2021 generated more than $100mn in sales, up 75% on 2018 levels (13 of them generated more than $1bn in sales). Time spent in shopping apps reached an amazing 100bn hours globally in 2021, up 100% on 2018’s level, and again, Indonesia and Brazil were the fastest growers, with these mobile native countries embracing innovative forms of retail. Nearly three quarters of all online retail is now transacted through mobile.

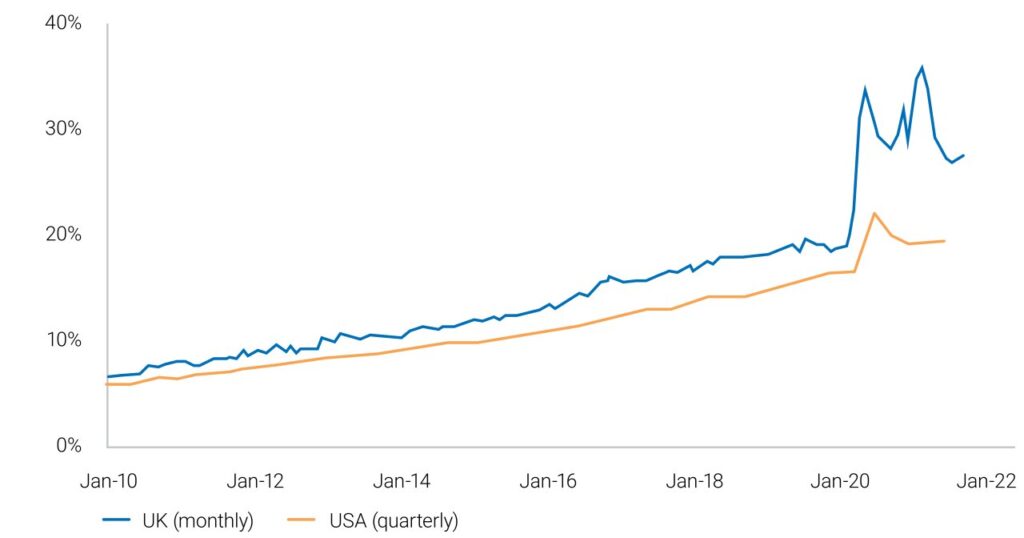

As the pandemic funnelled people, whether they liked it or not, onto digital platforms, patterns of behaviour and payment systems were laid out that won’t be fully reversed even when the last lockdown law is consigned to the bin. E-commerce is an excellent example: it was accelerated by years in 2020, and didn’t revert back to normal even when lockdowns lifted – you can see in the chart ‘retail unbundles’ e-commerce as a % of retail, after taking 7 years in the U.K. to get from 10-20%, has jumped to 30% in 18 months. If you exclude groceries, 40% of UK retail is now online. This is creating buying channels and behaviours that won’t revert.

Ecommerce as a share of addressable retail

But when we invest, we should remember we are still very early in the journey from bricks & mortar to digital retail – global consumer spending is around $50trn annually, and e-commerce still only represents $3-4trn of this. We will never live in a world where everything is purchased online, but the equilibrium point will certainly be further along the road to digitalisation ten years from now than it is today, as other forms of offline retail walk the painful road that newspapers, bookstores and other early casualties of e-commerce trod. Companies like Shopify, a leader of the anti-Amazon alliance, will be vital in tooling up retailers with the marketing, payments and logistical solutions to compete in the e-commerce era without surrounding their individualism.

Autos getting smarter

Away from the mobile phone, a vast array of other daily objects and experiences are seeing their digital density increase. We have become familiar conceptually with an Internet of Things, but recent years have seen this idea become more concrete. Take the auto industry, which is increasingly adding autonomous capabilities to its vehicles, and talking about a future where fully autonomous cars slice through cities, speaking to one another in real time, optimising routes, making decisions, reducing crashes to near nil (and freeing up more digital time for passengers no longer engaged with the wheel). This will require massive investment in chip technology, and indeed the autonomous chip-market is expected to nearly triple by 2030.

Finally, all of the electronic and digital and online interactions referenced above churn out epochal volumes of data, and all of this data has enormous value in the right hands. The figure is somewhat out of date now, but Forbes calculated that 90% of the data in the world had been created in the last two years. That volume is still exploding. What commodities were to the 20th century, data may be for the 21st, but instead of sitting in the hands of a few geographically fortunate countries, it sits in the hands of a select group of technologically savvy corporations. It can be used to understand and target consumers, but also to power algorithms and artificial intelligence. Microsoft has previously spoken about the quality of an AI algorithm doubling with every 10x volume of data flushed through it. The conclusion is simple: algorithms become stronger the more data they eat, and so data rich companies will develop an intelligence gap versus their more impoverished peers than will help form enormous digital moats.

Dialling into digitalisation

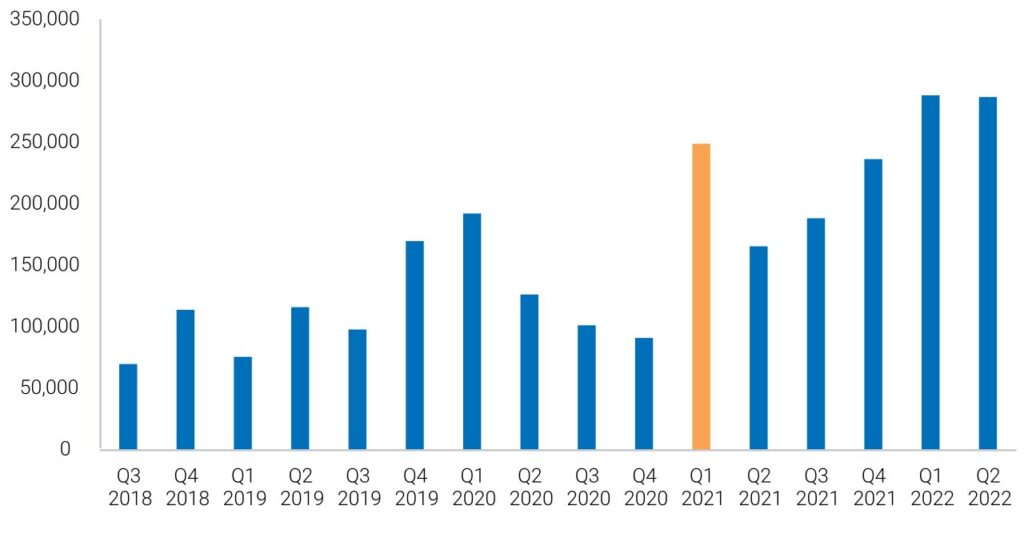

With such profound changes occurring, it is essential that we allocate capital to companies both driving and benefiting from these trends towards greater digitalisation. One broad way to play this theme is through TSMC, the world’s leading semi-conductor foundry. Chips are the building blocks of so much of the world’s computing and technological backbone, and TSMC has more than a 50% world market share in the made to order chip market. But the company is not just the volume leader. It is the go-to partner for the world’s most sophisticated tech companies, being the sole supplier for Apple’s 5-nanometer processors, used in various Apple products including the iPhone 12, MacBook Air and MacBook Pro, and also making the A15 Bionic chips found inside Apple’s newest gadgets, like the iPhone 13 and iPad mini. TSMC also partners with Qualcomm, AMD and Nvidia. At the bleeding edge of chip technology, TSMC dominates: it is estimated it is responsible for a staggering 92% of the world’s high-end chip production. And TSMC is continuing to focus on ever more sophisticated chips. It is to bring out its 3nm process node this year, and is channelling vast capex into meeting the ever more ravenous demand for chips in every industry from smartphones to data centres to connected vehicles. The chart shows TSMC’s capex, with the highlighted bar marking the first quarter of 2021, as TSMC kicked its capex up a gear in response to the pandemic induced spike in demand.

Capital expenditures by quarter for TSMC

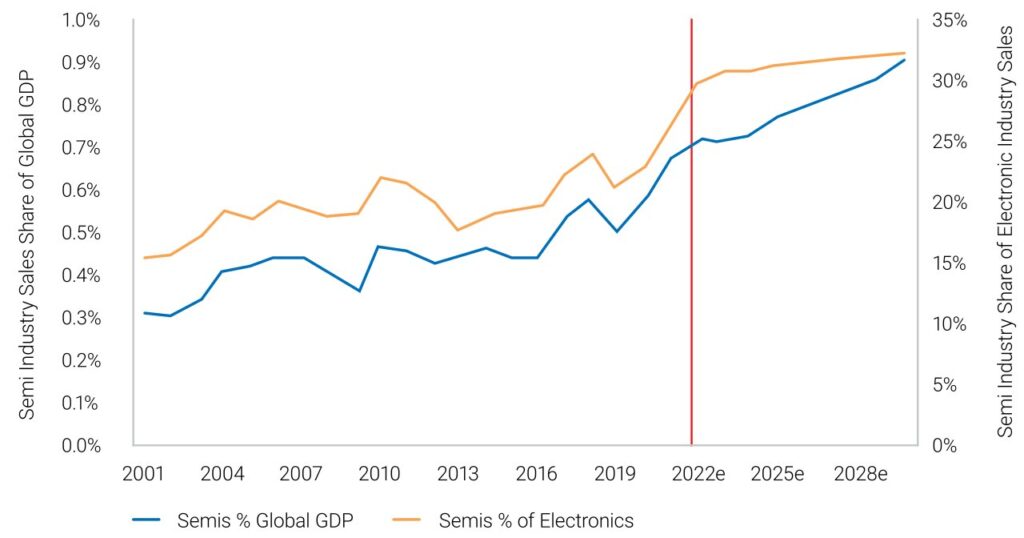

The chart below is a simple but effective way of visualising the ever more central role of the semi-conductor in the world, with the chip industry’s share of global GDP almost doubling over the last decade. That share of GDP is expected to increase significantly over the next 10 years as well. We want to capitalise on this, and TSMC is an excellent way of doing so.

Semis Share: Global GDP & Electronics

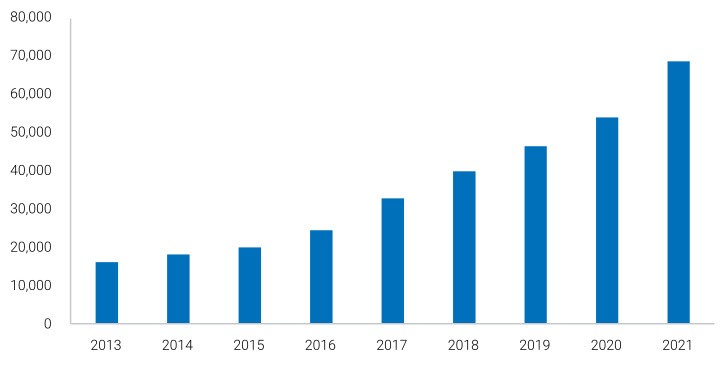

Apple is TSMC’s largest single customer, and we believe it is another outstanding way of capitalising on the increase digitalisation of the world. There are more iPhones and iPads in use today than all the PCs combined, and Apple has been adding a staggering three million active devices into the world every week for over a decade. A huge amount of the most affluent smartphone users globally use iPhones – Apple provides both the hardware and the operating system for perhaps the most important physical device of our century. An excellent barometer of mobile activity is Apple’s service revenue, which is like a tax on mobile phone commerce– Apple’s service revenue has been accelerating off a bigger base in 2021, jumping 27% YoY, the fastest rate in years, as the pandemic structurally accelerated it. Apple made comfortably more Services revenue in 2021 than it did in 2014, 2015 and 2016 combined. Perhaps just as importantly, Apple is currently at the forefront of exploring new ways of protecting consumer data in the digital era, making it harder for consumers to be tracked across platforms without their permissions. This may start to form the blueprint of what privacy looks like into the internet era.

Apple services revenue $bn

Finally, not every company will have proprietary technical nous, but it is increasingly important for all companies to be technologically enabled. We are invested in Accenture, a consultancy which helps its clients upskill themselves across a range of areas, including digitally. Accenture helps its clients to manage big data, which they define as ‘data sets created by digital technology systems… that are so voluminous that they can’t by processed by traditional IT’. Accenture helps these clients transition into the cloud, allowing them to use cloud solutions in a cost effective manner, generating insight that they otherwise wouldn’t have the IT infrastructure to drive. Accenture is investing billions to develop capabilities it can use to help clients migrate to the cloud; it estimates that most business are still only ~20% in the cloud, providing a huge opportunity for them to help shepherd these businesses across to a more data savvy future.

The digitalisation of everything is well underway, but with a certain social media company somewhat hubristically rebranding itself as Meta in 2021, there are signs everywhere that we are probably still early on in the journey across to a more digitally immersive, data rich future, and as investors, we are determined to be on the right side of that journey.