At its meeting on 21 March, the Swiss National Bank (SNB) unexpectedly cut rates, starting its monetary policy easing cycle before the other main central banks. In this Macro Flash Note, Senior Economist GianLuigi Mandruzzato looks at the factors behind the SNB’s decision and the outlook for Swiss policy rates.

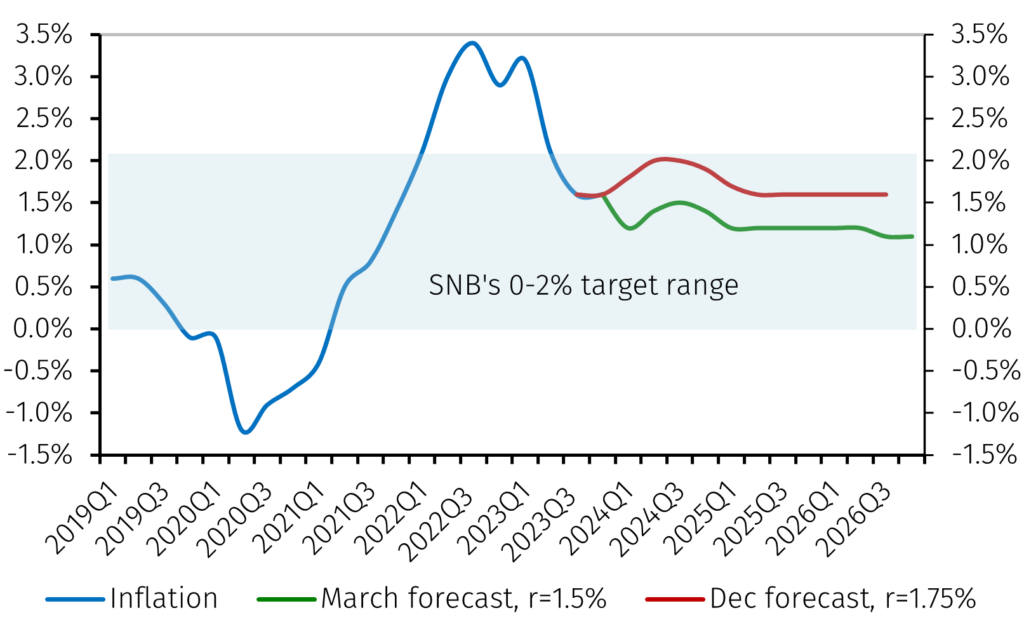

Surprising market expectations, on 21 March the SNB announced a reduction of its policy rate by 0.25 percentage points to 1.50% and signalled that further expansionary policy changes are possible in 2024. The SNB’s decision to cut interest rates was based on the improved outlook for inflation (see Chart 1). The SNB’s new conditional forecasts see inflation around half a percentage point below the December forecast. Swiss inflation is now expected to stabilise just above 1% in the medium term, close to the midpoint of the SNB’s 0-2% target range and not far from the level it reached in February.

Chart 1. SNB conditional inflation forecast (year-on-year)

Source: Swiss National Bank. Data as at 21 March 2024.

The other factor that encouraged the SNB to act earlier than other major central banks is the strength of the Swiss franc. According to the SNB, the rise of the franc in the final months of 2023 went beyond what was justified by the inflation differential between Switzerland and its trading partners. The resulting real appreciation of the exchange rate reduces import prices and, by making Swiss exports more expensive, has an adverse impact on the Swiss economy. The rate cut should therefore help support Swiss GDP growth, particularly benefiting export-oriented industries and the tourism sector.

The SNB said it remains willing to intervene in the currency market “as necessary,” that it will continue to closely monitor inflation and will adjust interest rates to keep inflation within the target range.1

Swiss GDP growth is expected to be weak in the coming quarters and is subject to significant downside risks, mainly due to the international economic cycle. Implicitly, this suggests that risks to inflation are predominantly to the downside and that the SNB therefore has a bias to reduce interest rates further over the next few quarters, perhaps as early as the June meeting.

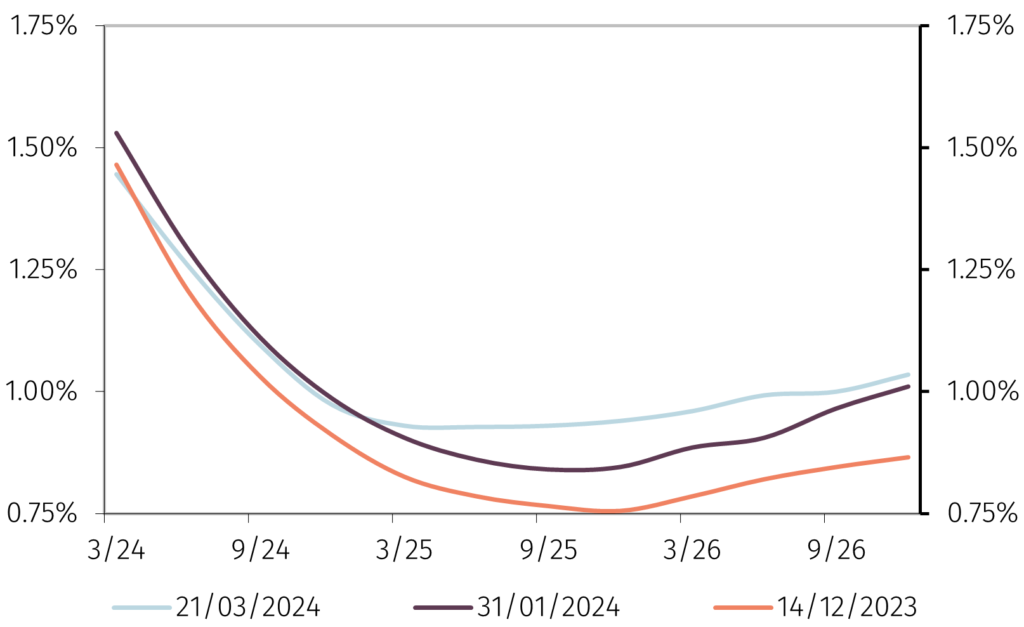

Chart 2b. Swiss 3-month interbank rate implied in futures contracts

Source: LSEG Data & Analytics, and EFGAM calculations. Data as at 21 March 2024.

Indeed, based on interest rate futures contracts, markets are anticipating that the Swiss policy rate will fall to 1% before the end of 2024 and then stabilise at around that level (see Chart 2). If that proves to be a reliable forecast and the other main central banks reduce interest rates as implied in futures contracts, the differential between Swiss and foreign short term interest rates will become less negative, thereby supporting the Swiss franc exchange rate.