Global stock markets suffered further losses this week, and September looks set to be one of the weakest performing months of 2023

Share prices continued to be held back by concerns about high interest rates and the outlook for global growth given China’s lacklustre post-pandemic recovery. In the past few weeks, these issues have been compounded by rising oil prices and, more recently, the prospect of a United States government shutdown.

At the close of trading on Thursday, lawmakers in Congress appeared some distance away from reaching an agreement that would allow US state spending to continue past the start of October. A shutdown is expected to harm America’s credit rating and could have a negative impact on financial markets.

United States

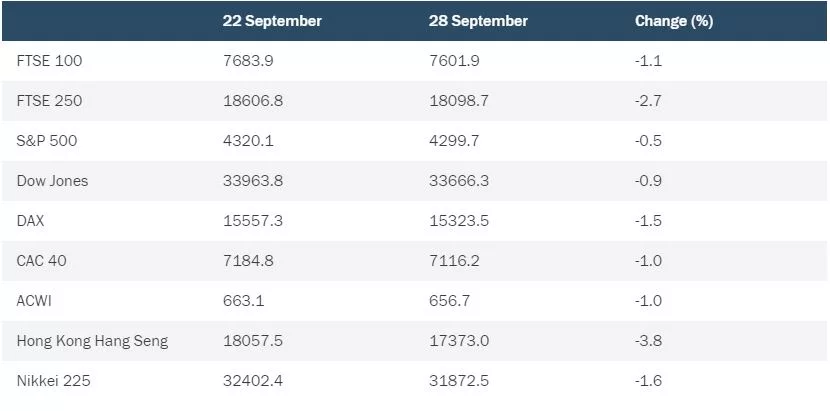

On Wall Street, the Dow Jones Industrial Average ended trading on Thursday 0.9% down for the week so far, with the S&P 500 falling 0.5%. Worries that the Federal Reserve could raise interest rates again before the end of the year sent bond yields higher at the start of the week. However, softer economic data – including a fall in new home sales and an increase in unemployment claims – helped to calm investors’ nerves on Wednesday and Thursday. An antitrust probe into one of the country’s biggest online retailers hit sentiment in the technology sector, and markets remained uncertain as to what ramifications a government shutdown was likely to have.

UK

In the UK, the FTSE 100 closed on Thursday 1.1% down for the week so far. Continuing fears for China’s growth outlook hit the price of mining stocks, with demand for precious metals and other commodities likely to be lower than previously expected in the months ahead. Analysts warned that the UK’s economic growth is set to underperform in 2023 and 2024, while data published on Monday showed a drop in retail sales for August following a similar fall in July. Energy companies were one bright spot this week, with oil prices remaining strong and the British government giving the green light to a North Sea gas extraction project.

Europe

In Frankfurt, the DAX index ended Thursday’s session down 1.5% for the week, while France’s CAC 40 lost 1%. European shares were hit by concerns about interest rates in the US and growth in China, while European Central Bank president, Christine Lagarde, warned of ongoing weakness in the eurozone economy. However, Thursday ended on a relatively positive note as latest data showed that the rate of inflation in Germany had receded to its lowest level since Russia’s invasion of Ukraine in February 2022.

Asia

In Asia, the Hang Seng index in Hong Kong slumped 3.8% as the turmoil in China’s real estate sector continued. Trading in the shares of one of the country’s biggest property companies was suspended late in the week after the firm – which is currently under investigation by Chinese authorities – was unable to reach an agreement on refinancing part of its debt. Industrial profits among Chinese firms fell in August, albeit more slowly than in previous months. Japan’s Nikkei 225 index of leading shares, meanwhile, fell 1.6% as investors reacted nervously to news that the Bank of Japan was unsure of when it would end its current negative interest rate policy.

Note: all market data contained within the article is sourced from Bloomberg unless stated otherwise, data as at 28 September 2023.