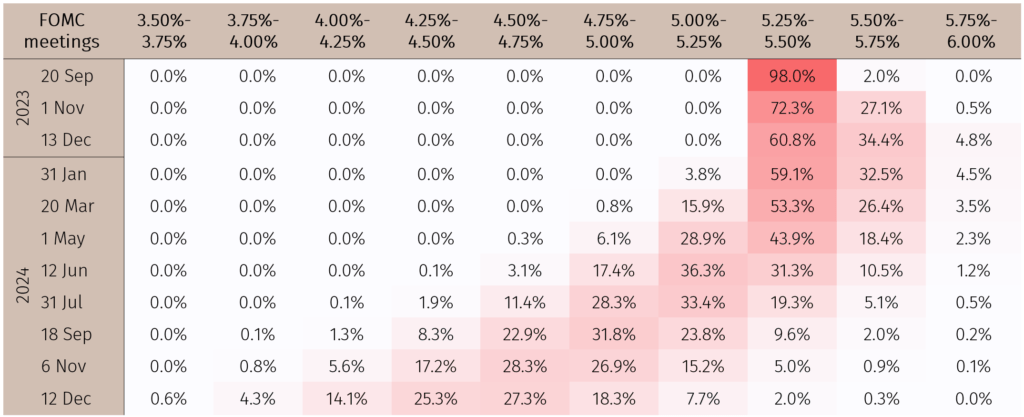

The Federal Reserve is widely expected to keep interest rates steady at its meeting on 20 September despite the rise in headline Consumer Price Index (CPI) inflation in August. Indeed, current market pricing suggests no change in interest rates with a probability of 98%. In this Macro Flash Note, Chief Economist Stefan Gerlach comments on the meeting.

There is much agreement that the Federal Open Market Committee (FOMC) will leave interest rates unchanged at its meeting this week. The main reason is that inflation has been declining in recent months.

1. Probabilities of Fed interest rate decisions as implied by market pricing

Source: : CME. Data as of 16 September 2023.

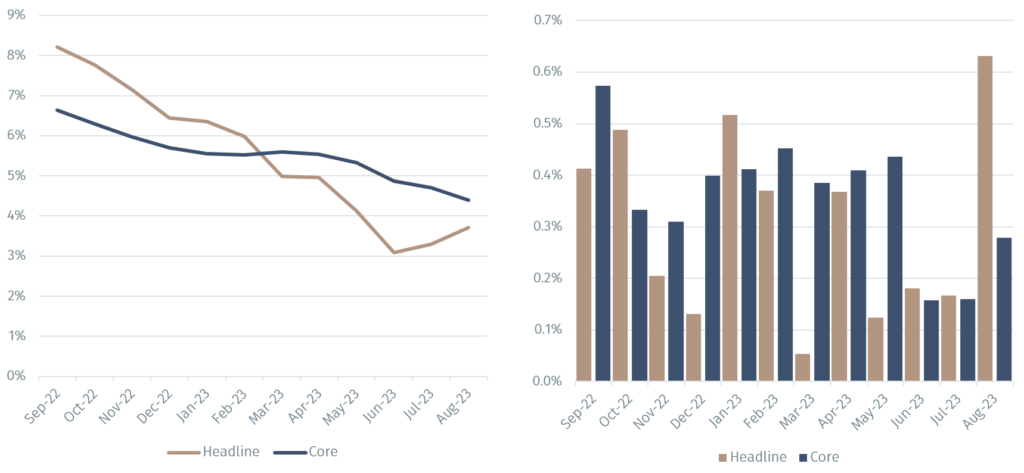

Of course, the CPI data for August released last week were a little discouraging, with annual headline inflation rising to 3.7% from 3.2% in July. However, that increase was principally due to a sharp rise in gasoline prices of 10.8% Month-over-month (MoM) which caused headline CPI inflation to increase to 0.6% MoM after 0.2% in July. Moreover, the increase in the headline data was largely expected by markets.

However, core inflation fell to 4.3% Year-over-year (YoY) in August from 4.7% in July. Month-on-month, core inflation was 0.3% in August, up from 0.2% in July.

2. CPI Inflation, y/y (left) – CPI Inflation, m/m (right)

Since core inflation plays a much greater role than headline inflation in the Fed’s thinking about the economy, FOMC members are likely to disregard the rebound in the latter. They understand data are erratic and occasional sharp changes in monthly inflation rates are common. They therefore attach greater emphasis to inflation rates over a few months.

With annualised headline inflation running at 3.9% over the last three months and core inflation at 2.4%, the massive increase in interest rates engineered by the Fed over the last 18 months has clearly slowed inflation.

It therefore makes sense to hold interest rates steady and wait to see whether inflation will continue to slow on its own or if further interest rate increases will be necessary. Unless the September and October CPI releases signal an obvious inflation problem, the FOMC is likely to wait until December to make that call. Interestingly, while the market is currently pricing in a 61% probability that the Fed will leave interest rates unchanged in December, it attaches a 34% probability that rates will be set 25 bps higher than today, and a 5% probability that they then will be set 50 bps higher.

With interest rates expected to be kept on hold this week, the focus of the meeting will be in what the Fed communicates regarding its outlook for the US economy. Given recent developments, it is possible that it will lower the expected projections for inflation but raise the projections for economic activity.

The dot plots1 will be revealing. On average members will likely view themselves as having finished raising interest rates, although some members may signal that they think a further increase this year will be appropriate. Interest rate cuts are likely to be projected for next year.

For the FOMC to decide to cut interest rates, it will most likely require continued gradual reductions in core inflation and a further rebalancing of the US labour market, entailing some increase in unemployment and participation rates, and a further slowing in the growth rate of labour costs. Keeping a close eye on core inflation and US labour market data therefore remains key to understanding the Fed in the months ahead.